Last Update 12 Jun 26

TIINDIA: Future P/E Premium And Borrowing Plans Will Support Upside Potential

Analysts have slightly reduced their price target on Tube Investments of India to ₹3,362, reflecting marginally lower assumptions for the discount rate, revenue growth and future P/E, while keeping their overall fair value view broadly unchanged.

Analyst Commentary

Recent commentary on Tube Investments of India centers on how much investors should pay for the stock rather than on a major shift in the underlying thesis. With the price target trimmed but the fair value view largely intact, analysts are focusing on the balance between execution risks and longer term growth potential.

Bullish Takeaways

- Bullish analysts highlight that only modest tweaks to discount rate, revenue growth and future P/E assumptions were needed. They see this as a relatively contained adjustment to the valuation framework rather than a wide reset.

- The broadly unchanged fair value view is interpreted as confidence that the company can still work toward its medium term growth ambitions, even if the implied upside from the prior target has narrowed.

- Supportive commentary often points to Tube Investments of India having room to justify a premium P/E over time if it continues to execute on its expansion and capital allocation plans efficiently.

- Some bullish analysts see the current consolidation in estimates as potentially reducing the risk of future downward revisions. They view this as helpful for sentiment around the stock.

Bearish Takeaways

- Bearish analysts focus on the lower revenue growth assumptions behind the updated target and read this as a signal that near to medium term growth expectations may have been too optimistic.

- The reduction in the implied future P/E raises questions for more cautious investors about how much multiple expansion Tube Investments of India can realistically support without clearer evidence of improving fundamentals.

- Some cautious views center on the sensitivity of the valuation to discount rate inputs, which can make the stock more exposed to changes in risk sentiment or funding costs.

- Bears also flag that even a small cut to the price target can weigh on momentum driven interest, especially for investors who were relying on a larger valuation buffer to justify new positions.

What's in the News

- A board meeting is scheduled for May 13, 2026 at 12:30 Indian Standard Time to consider and approve the audited standalone and consolidated financial results for the year ended March 31, 2026. (Source: Company filing)

- On the same agenda, the board will consider recommending a final dividend, if any, for the financial year ended March 31, 2026. (Source: Company filing)

- The board will also consider approving long term borrowings through the issue of non convertible debentures during FY 2026 27, in one or more tranches. (Source: Company filing)

- The meeting is expected to propose the upcoming Annual General Meeting. (Source: Company filing)

Valuation Changes

- Fair Value: The fair value estimate is maintained at ₹3,362.33, indicating no change in the central valuation outcome despite tweaks to inputs.

- Discount Rate: The discount rate has been reduced slightly from 14.38% to 14.35%, which is a very small adjustment to the risk assumption used in the model.

- Revenue Growth: The revenue growth input remains effectively unchanged, with only a tiny adjustment in the modelled decline, holding around a 19.69% drop.

- Net Profit Margin: The assumed net profit margin stays broadly flat at about 10.68%, with only a marginal numerical refinement.

- Future P/E: The future P/E multiple has been trimmed slightly from 78.56x to 78.50x, reflecting a very small reduction in the valuation multiple applied.

Key Takeaways

- Expansion into electric vehicles, automation, and value-added products is expected to drive margin improvement and support top-line growth amid rising industry demand.

- Diversification into exports, medical devices, and premium market segments should enhance revenue stability and leverage evolving trends in global mobility and manufacturing.

- Intensifying EV segment competition, export uncertainties, customer concentration, high capital spending, and raw material cost pressures threaten growth, profitability, and earnings stability.

Catalysts

About Tube Investments of India- Engages in the manufacture and sale of precision engineered and metal formed products to automotive, railway, construction, agriculture, etc.

- The company's strategic expansion into electric vehicles, including three-wheelers, e-trucks, and upcoming launches in new subsegments, aligns with the rising demand for green mobility solutions and government incentives (such as the PLI scheme). As volumes scale, benefits from cost reduction, local sourcing (indigenization), and upcoming battery pack manufacturing are likely to drive top-line growth and improve gross/operating margins over time.

- Rapid urbanization and higher disposable incomes in India are fueling demand for automobiles and mobility products; Tube Investments is capitalizing on this with strong double-digit volume growth in its core Engineering and Mobility divisions, which should support continued revenue expansion and sustainable margin recovery as input cost pass-throughs stabilize.

- The company's increased focus on process automation, value-added product lines (e.g., fitness-focused bicycles, spare parts, premium precision tubes), and operating efficiencies positions it to enhance net margins even as raw material price volatility and competitive intensity persist.

- Growth in export-oriented product categories, supported by ongoing CE certifications and customer approvals at new manufacturing facilities, provides incremental revenue diversification; this offsets near-term protectionist risks and positions the company to capture increased share as global infrastructure and manufacturing investment cycles accelerate.

- Prudent deployment of capital-doubling down on emerging areas like medical devices, clean mobility, and advanced CDMO manufacturing-combined with targeted inorganic expansion, is expected to compound future earnings and market share, capitalizing on industry trends of premiumization, consolidation, and preference for technologically advanced and reliable suppliers.

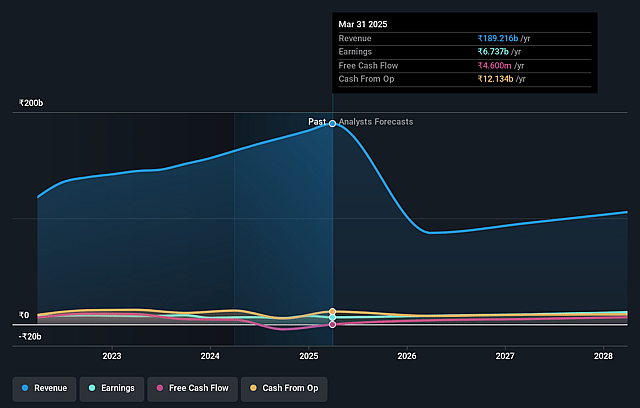

Tube Investments of India Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Tube Investments of India's revenue will decrease by 19.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.9% today to 10.7% in 3 years time.

- Analysts expect earnings to reach ₹12.3 billion (and earnings per share of ₹63.6) by about June 2029, up from ₹6.3 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹13.6 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 78.9x on those 2029 earnings, down from 90.7x today. This future PE is greater than the current PE for the IN Auto Components industry at 25.7x.

- Analysts expect the number of shares outstanding to decline by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.35%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition in the electric vehicle (EV) segment, particularly in 3-wheelers, is resulting in lower-than-expected volumes, limited pricing power, delayed achievement of operational breakeven, and potential margin pressure, which could impact net profitability and long-term earnings quality.

- Uncertainty around export growth due to rising global protectionism and tariffs (e.g., in the US), along with delays in new product development for international markets, increases the risk of missed revenue targets and can erode top-line growth from exports.

- Customer concentration, especially notable in the automotive segments, may lead to significant fluctuations in revenue and earnings if major clients reduce orders or switch to alternative suppliers, negatively affecting revenue stability.

- High ongoing capital expenditure requirements (e.g., ₹350 crores planned for this year), coupled with investments in new divisions like EVs, TI Medical, and CDMO, could constrain free cash flow, delay return on investment, and pressure bottom-line margins if targeted volume growth or profitability is not achieved.

- Delay in cost recovery and margin normalization due to lag in passing through raw material (steel) price changes to customers, combined with sectoral input cost volatility and slow take-up of process automation or indigenization strategies, can result in compressed or unpredictable net margins over multiple quarters.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹3362.33 for Tube Investments of India based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3870.0, and the most bearish reporting a price target of just ₹2780.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹115.1 billion, earnings will come to ₹12.3 billion, and it would be trading on a PE ratio of 78.9x, assuming you use a discount rate of 14.4%.

- Given the current share price of ₹2975.3, the analyst price target of ₹3362.33 is 11.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Tube Investments of India?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.