Catalysts

About HORNBACH Holding KGaA

HORNBACH Holding KGaA operates large format DIY and home improvement stores across Europe, complemented by an integrated e commerce offering and a specialist builders merchant business.

What are the underlying business or industry changes driving this perspective?

- The company continues to open large box DIY stores in Germany, Austria and Romania and is preparing to enter Serbia. The associated higher CapEx and inventory needs can keep free cash flow under pressure and weigh on future earnings growth unless new sites scale quickly.

- Customer footfall and like for like sales across Europe have been positive and market share in several countries has risen. However, subdued consumer sentiment and pockets of weaker purchasing power, such as in Romania, may limit the ability to translate higher volumes into stronger revenue growth.

- E commerce sales grew 8.1% and now account for 12.9% of group sales. Continued investment in IT infrastructure and omnichannel capabilities raises selling and administrative expenses, which can cap any improvement in net margins if cost savings from digitalisation take longer to materialise.

- Demand from professional customers and installation services is growing faster than group sales. A still soft construction sector and cautious investment cycles could constrain the contribution of this higher ticket segment to EBIT and delay any meaningful uplift in overall margins.

- The company reports a solid equity ratio of 47.1% and an improved net financial debt to EBITDA ratio of 2.5x. However, the plan to keep CapEx at elevated levels and invest €25 million to €40 million per new Serbian store could slow future improvements in leverage metrics and keep returns on invested capital and earnings growth closely tied to execution quality on these projects.

Assumptions

This narrative explores a more pessimistic perspective on HORNBACH Holding KGaA compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming HORNBACH Holding KGaA's revenue will remain fairly flat over the next 3 years.

- The bearish analysts assume that profit margins will increase from 2.1% today to 2.2% in 3 years time.

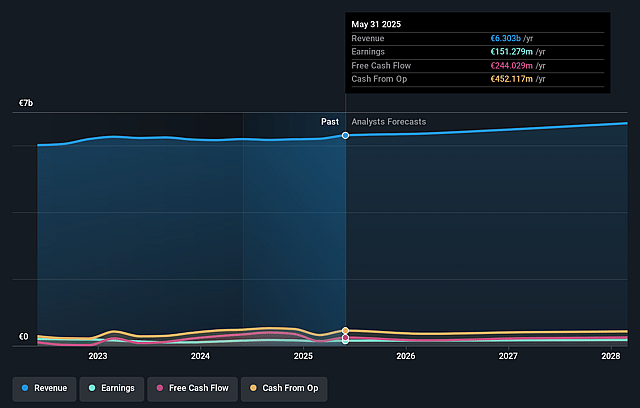

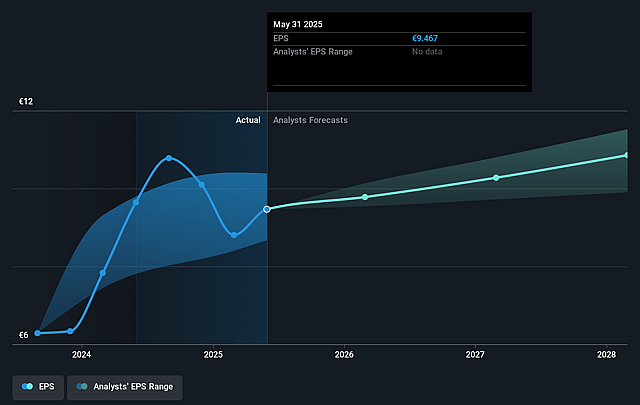

- The bearish analysts expect earnings to reach €143.5 million (and earnings per share of €8.97) by about January 2029, up from €133.5 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €189.0 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 11.4x on those 2029 earnings, up from 9.8x today. This future PE is lower than the current PE for the GB Specialty Retail industry at 18.9x.

- The bearish analysts expect the number of shares outstanding to decline by 0.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.05%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Persistent store expansion in existing European markets and the planned entry into Serbia with 6 to 8 large formats, each with CapEx of €25 million to €40 million, could support higher long term sales and market share than implied by a flat share price view. This would feed through to revenue and potentially earnings.

- The strong long term home improvement potential that management highlights, combined with HORNBACH's history of gaining market share in countries like Germany, the Netherlands and Czechia, may support ongoing like for like sales growth and customer footfall. This could put upward pressure on revenue and EBIT rather than leaving the share price unchanged.

- Ongoing investment in IT infrastructure, software, AI and e commerce, which already accounts for 12.9% of sales and is growing, is aimed at efficiency and better working capital management over time. If these benefits come through more strongly than expected they could lift net margins and free cash flow, challenging the assumption that the share price will stay flat.

- Growing exposure to professional customers, building renovation and installation services, all of which management reports as growing faster than group sales with double digit growth in installation services, could support a higher quality revenue mix and better EBIT contribution in the long run. This may not be consistent with a static share price.

- The company reports an equity ratio of 47.1% and a net financial debt to EBITDA ratio of 2.5x. If this balance sheet strength allows HORNBACH to keep funding higher CapEx while maintaining dividends, future improvements in leverage metrics and returns on invested capital could support a re rating of the shares through higher earnings and potentially a higher P/E multiple.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for HORNBACH Holding KGaA is €80.0, which represents up to two standard deviations below the consensus price target of €100.57. This valuation is based on what can be assumed as the expectations of HORNBACH Holding KGaA's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €117.0, and the most bearish reporting a price target of just €80.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be €6.6 billion, earnings will come to €143.5 million, and it would be trading on a PE ratio of 11.4x, assuming you use a discount rate of 9.0%.

- Given the current share price of €81.8, the analyst price target of €80.0 is 2.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on HORNBACH Holding KGaA?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.