Last Update 15 Jul 26

Fair value Decreased 28%PXA: Proposed Fee Cuts And New CFO Appointment Will Support Future Upside

Analysts have lowered their price target for PEXA Group from A$15.84 to A$11.36, citing updated expectations for revenue growth, profit margins, and a higher assumed future P/E multiple in their valuation work.

What's in the News for PEXA Group

- The Independent Pricing and Regulatory Tribunal of New South Wales (IPART) issued a draft report recommending a 20% cut to regulated service fees on PEXA Group's electronic conveyancing exchange, with a potential revenue impact of about A$70 million over the regulatory period, according to recent news reports.

- The proposed fee reductions are scheduled to commence on 1 July 2027 and apply over a four year regulatory period ending in FY2030/2031, subject to the outcome of the ongoing public consultation process.

- IPART's draft suggests implementing the entire fee cut within one year, while PEXA is advocating for a phased reduction over four years to spread the financial impact, based on the primary news coverage.

- News reports highlight that PEXA's shares fell between 11.8% and 18% across different trading sessions following the draft recommendation, reflecting market sensitivity to potential changes in regulated revenue.

- PEXA Group announced that Graham Curtin has been appointed as Group Chief Financial Officer, effective 1 September 2026, with the current interim CFO, Liz Warrell, remaining through delivery of the FY26 results to support the transition.

Valuation Changes for PEXA Group

- Fair Value: revised lower from A$15.84 to A$11.36, indicating a materially reduced central valuation estimate for PEXA Group.

- Discount Rate: adjusted slightly higher from 8.40% to 8.59%, pointing to a modestly higher required return in the updated model.

- Revenue Growth: reduced from 8.37% to 0.82%, reflecting much more conservative assumptions for future A$ revenue expansion.

- Net Profit Margin: lowered from 17.09% to 7.61%, indicating a materially smaller share of A$ revenue expected to fall to the bottom line.

- Future P/E: increased from 39.30x to 78.98x, suggesting a higher assumed valuation multiple applied to future earnings despite the lower earnings assumptions.

Key Takeaways

- Expansion into the UK, regulatory support, and partnerships with major lenders are set to accelerate adoption and diversify revenue sources.

- Investments in compliance, automation, and data-driven solutions position the company for higher-margin growth and increased customer retention.

- Heavy upfront investment, regulatory pressures, and region-specific risks pose ongoing challenges to PEXA's earnings growth, margin stability, and diversification ambitions.

Catalysts

About PEXA Group- Operates a digital property settlements platform in Australia.

- The company's expansion into the UK, leveraging its proven Australian platform and with the recent onboarding of Tier 1 lender NatWest, represents a significant near-term catalyst for increased adoption, market share gains, and revenue diversification as more lenders and conveyancers are targeted and integrated.

- Regulatory momentum and government mandates in both Australia and the UK toward transparent, efficient, and paperless property transactions are likely to drive continued acceleration of electronic settlements, thereby supporting long-term growth in transaction volumes and recurring revenue streams.

- PEXA's strategic investment in next-generation AML solutions and enhanced cybersecurity-aligned with incoming AML regulations (effective July 2026) and greater industry focus on data security-positions the company to capture higher-margin, value-added service revenue from its established customer base as compliance obligations intensify.

- Ongoing operational automation, platform modernization (through modular architecture), and productivity initiatives are expected to further reduce cost per transaction and enhance group EBITDA and Exchange margins over time, supporting disproportionate earnings growth relative to revenue.

- Emerging demand for robust property data analytics and integrated digital solutions (e.g., expanded API offerings and automated valuation models) provides additional cross-sell and upsell opportunities, supporting margin expansion and user stickiness, which are undervalued in current financials.

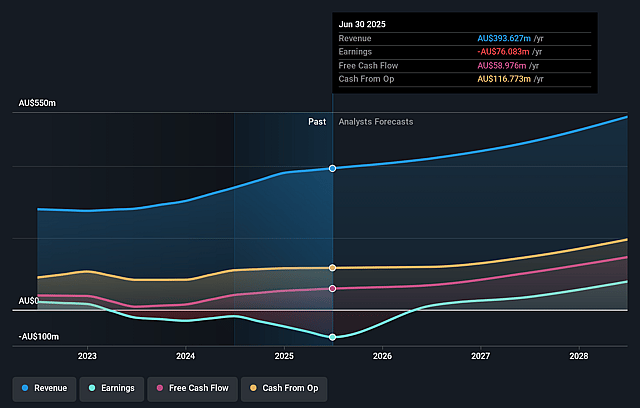

PEXA Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming PEXA Group's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from -7.5% today to 7.6% in 3 years time.

- Analysts expect earnings to reach A$32.2 million (and earnings per share of A$0.19) by about July 2029, up from -A$31.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting A$54.2 million in earnings, and the most bearish expecting A$8.4 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 79.4x on those 2029 earnings, up from -43.0x today. This future PE is greater than the current PE for the AU Real Estate industry at 11.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.59%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- PEXA's long-term success is highly dependent on adoption in the UK market, but management notes that operating and onboarding costs will outpace revenue for several years; if lender and conveyancer adoption is slower than anticipated, or if network effects don't materialize, projected diversification and revenue growth could stall, weighing on both revenue and net margins.

- Ongoing high levels of investment in technology, international expansion, platform modernization, and regulatory compliance (e.g., cybersecurity and AML readiness) lead to persistently elevated CapEx and OpEx, which may constrain free cash flow generation and limit near

- to medium-term earnings growth.

- PEXA's financial performance is closely tied to property transaction volumes in Australia and the UK; macroeconomic factors such as slow housing stock growth, interest rate uncertainty, and affordability constraints could dampen volumes in both markets over the long term, directly impacting revenue and earnings growth prospects.

- Despite strong current market share in Australia (≈90% digitization), management guides only slow incremental penetration and notes potential commoditization risks and regulatory reviews (e.g., IPART pricing review), which could pressure pricing and thus lower net margins over time.

- The company's digital solutions segment is under strategic review, with possible divestment under consideration; lack of scale or unclear fit within the group could result in foregone cross-selling opportunities or one-off impairments, both of which may adversely affect longer-term revenue streams and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$11.36 for PEXA Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$16.0, and the most bearish reporting a price target of just A$9.2.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be A$423.2 million, earnings will come to A$32.2 million, and it would be trading on a PE ratio of 79.4x, assuming you use a discount rate of 8.6%.

- Given the current share price of A$7.61, the analyst price target of A$11.36 is 33.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on PEXA Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.