Last Update 18 Jun 26

Fair value Increased 0.92%CGY: Defence Strategy Champion Positioning Will Support Profitable Stock Repricing

Analysts have nudged their fair value estimate for Calian Group to about CA$94 per share, pointing to updated price targets in the CA$90 to CA$100 range and expectations for a focus on profitable growth, margin expansion, and benefits tied to Canada's Defence Industrial Strategy.

Analyst Commentary

Recent analyst commentary on Calian Group centers on how the company could use its positioning within Canada's Defence Industrial Strategy to support profitable growth and justify higher valuation targets.

Bullish Takeaways

- Bullish analysts highlight Calian Group as a key beneficiary of Canada's Defence Industrial Strategy, viewing its role across multiple "capabilities" as a support for growth in existing defense-related verticals.

- Updated fair value and price targets in the CA$90 to CA$100 range reflect confidence that management's focus on profitable growth could support margin expansion over time.

- The C$100 price target is framed around expectations that structural reorganization will help sharpen execution, which bullish analysts see as important for sustaining returns on invested capital.

- The raised C$90 target underscores a view that current valuation may not fully reflect potential benefits tied to defense procurement and promotion programs.

Bearish Takeaways

- Bearish analysts may question how quickly Calian Group can translate its Defence Industrial Strategy positioning into consistent margin gains, which could affect how close the stock trades to the high end of current target ranges.

- Execution risk around structural reorganization remains a concern, since any delays or missteps could limit the earnings power implied by higher fair value estimates.

- Reliance on defense-related benefits could be seen as a concentration risk if procurement priorities or government programs do not evolve in line with bullish expectations.

- Some investors may view the CA$90 to CA$100 target range as leaving less room for error on growth and profitability assumptions, leading to a more cautious stance on valuation.

What’s in the News for Calian Group

- Calian Group and Cohere announced a collaboration agreement to evaluate and integrate sovereign artificial intelligence in defence environments, using Cohere’s North platform within controlled settings to test how secure, Canadian-developed enterprise AI can support mission planning, decision support, training and operational workflows. (Source: Key Developments)

- Through Calian VENTURES, the Cohere collaboration is set up to give Canadian small to mid-sized enterprises access to and evaluation of AI capabilities, with a focus on supporting innovation, adoption of sovereign AI and Canada’s defence industrial base. (Source: Key Developments)

- Calian Group launched ATHORA, a sovereign system-of-systems interoperability and orchestration platform designed to connect platforms, communications systems, sensors and mission systems across land, sea, air, space, cyber and electromagnetic domains within a common operational environment. (Source: Key Developments)

- ATHORA is being advanced with the Canadian defence industry, including foundational partner Evertz Microsystems, and is designed to support secure interoperability, faster capability integration, continuous modernization and alignment with Canada’s Defence Industrial Strategy while preserving sovereign control of systems and data. (Source: Key Developments)

- Calian Group exercised CA$75 million of its accordion feature under its credit facility, bringing total committed capacity to CA$275 million. The credit facility was renewed to a total capacity of CA$350 million, with CA$165 million drawn as of December 31, 2025. Management indicates this structure supports plans to pursue acquisitions and internal investment. (Source: Key Developments)

Valuation Changes for Calian Group

- Fair Value: CA$94.07, up slightly from CA$93.21, keeping Calian Group within the previously discussed CA$90 to CA$100 range.

- Discount Rate: 6.35%, down marginally from 6.40%, indicating a slightly lower required return in the updated model.

- Revenue Growth: 7.72%, trimmed slightly from 7.79%, implying a modestly more conservative CA$ revenue growth assumption.

- Net Profit Margin: 3.41%, up fractionally from 3.40%, reflecting a very small improvement in projected profitability.

- Future P/E: 35.10x, up slightly from 34.82x, signaling a minor increase in the valuation multiple used for Calian Group in the updated analysis.

Key Takeaways

- Strong growth in defense, space, and cybersecurity positions Calian to capitalize on expanding government budgets and heightened digital infrastructure needs.

- Targeted acquisitions and recurring healthcare contracts support margin expansion, diversification, and increased shareholder value through enhanced earnings and buybacks.

- Reliance on defense contracts, acquisition risks, segment underperformance, rising competition, and regulatory pressures threaten revenue stability, margins, and long-term profitability.

Catalysts

About Calian Group- Provides business products and solutions in Canada and internationally.

- Substantial recent growth in the defense business (now 50% of revenues and up 19% YoY) alongside a $1.5 billion backlog and a >$1 billion deal pipeline in Europe positions Calian to benefit from rising global defense spending-especially as public sector budgets in Canada and Europe expand in response to geopolitical instability-supporting strong future revenue and earnings growth.

- Intensifying investments in space and cybersecurity solutions-reinforced by increasing digitalization of critical infrastructure and heightened cyber threats-provide Calian with opportunities for premium, differentiated offerings, which should improve margin mix and drive robust EBITDA growth as these segments expand.

- Ongoing healthcare contract expansions (e.g., AMS acquisition and expanded HCPR contract), as well as the sustained need for healthcare and telehealth solutions driven by aging populations and government recruitment targets, underpin stable and recurring high-margin revenue growth for Calian's health business.

- Strategic M&A focus on high-margin, synergistic targets in defense, healthcare, and advanced tech bolsters diversification, accelerates revenue growth, and broadens Calian's cross-solution capabilities, supporting improved net margins and further enhancing the long-term earnings profile.

- Accelerated buyback activity (5% of shares YTD, targeting 6% for FY25), compounded by strong free cash flow generation and a robust balance sheet, will likely boost EPS and shareholder value as recurring revenue and improved segment performance materialize.

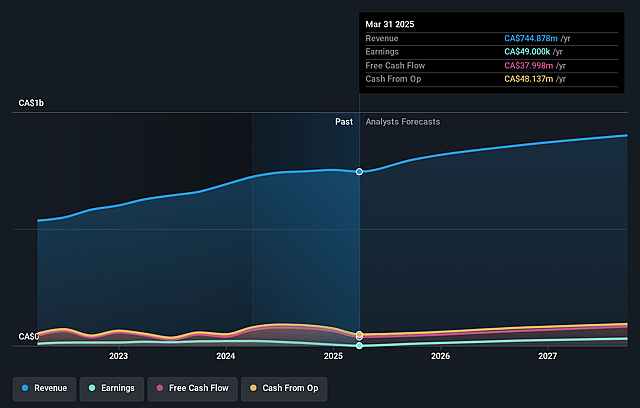

Calian Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Calian Group's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 4.0% today to 3.4% in 3 years time.

- Analysts expect earnings to reach CA$35.5 million (and earnings per share of CA$2.48) by about June 2029, up from CA$33.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CA$51.3 million in earnings, and the most bearish expecting CA$30.4 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 38.1x on those 2029 earnings, up from 27.7x today. This future PE is greater than the current PE for the CA Commercial Services industry at 27.7x.

- Analysts expect the number of shares outstanding to grow by 1.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.35%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent underperformance in the ITCS segment-including ongoing 10% revenue decline, management turnover, and delayed recovery-could signal structural challenges or market share loss, potentially eroding overall revenue and compressing margins if not reversed.

- Heavy reliance on government defense budgets (notably in Canada and Europe, where defense now contributes 50% of revenues) creates elevated exposure to political risk, procurement delays, or abrupt budget shifts, which could lead to revenue volatility and unpredictable contract timing.

- Aggressive expansion via acquisitions, while fueling growth, heightens integration risk and raises goodwill and debt levels; future acquisition missteps or rising valuation multiples for targets could trigger impairment charges and impact net earnings.

- Increased global competition in defense, IT, and healthcare services from both multinational primes and niche specialists may drive down average contract margins, dilute differentiation, and force Calian to spend more on sales, marketing, or hiring, thereby pressuring EBITDA and operating profits.

- Rising compliance costs from security, privacy, and ESG regulations, alongside talent shortages and wage inflation in specialized fields like cyber and engineering, risk inflating operating expenses and could constrain net margins and free cash flow over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$94.07 for Calian Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CA$1.0 billion, earnings will come to CA$35.5 million, and it would be trading on a PE ratio of 38.1x, assuming you use a discount rate of 6.4%.

- Given the current share price of CA$79.61, the analyst price target of CA$94.07 is 15.4% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Calian Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.