Key Takeaways

- Completion and production ramp-up of the Kiaka project are set to significantly boost revenue and increase gold production efficiency.

- Stable mining agreements and ample gold stockpile provide operational certainty, positioning the company for strong future cash flow and net margins.

- The company's financial health is vulnerable to infrastructure delays, regulatory changes, and gold price volatility, all of which pose risks to margins and earnings.

Catalysts

About West African Resources- Engages in the mining, mineral processing, acquisition, exploration, and project development of gold projects in West Africa.

- The Kiaka project is more than 80% complete with planned gold production expected to start in Q3 2025. This is likely to significantly increase revenue as it is expected to contribute to West African Resources becoming a 420,000 ounce per annum gold producer.

- The maiden grade control program at Kiaka has confirmed consistent zones of gold mineralization, which will aid in an efficient ramp-up and could lead to improved earnings due to increased production efficiency.

- The recent signing of new 5-year mining agreements for Toega and Sanbrado under similar terms to previous agreements could stabilize operating costs and positively impact net margins by providing operational certainty.

- West African Resources has a large stockpile of 86,340 ounces of contained gold, providing operational flexibility and a potential buffer that can support stable revenue in market downturns or during operational transitions.

- The company remains unhedged with significant cash reserves, which, combined with planned cost coverage for ongoing development projects, positions it well for future cash flow generation and maintaining healthy net margins.

West African Resources Future Earnings and Revenue Growth

Assumptions

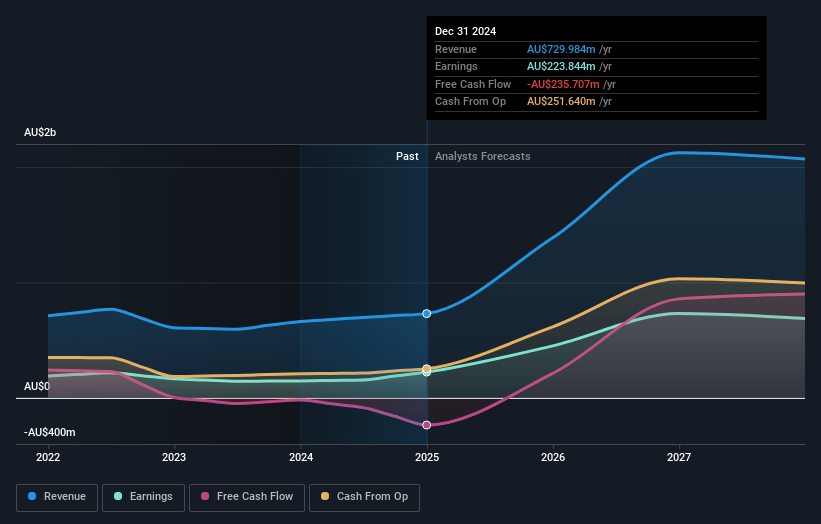

How have these above catalysts been quantified?- Analysts are assuming West African Resources's revenue will grow by 41.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 30.7% today to 33.2% in 3 years time.

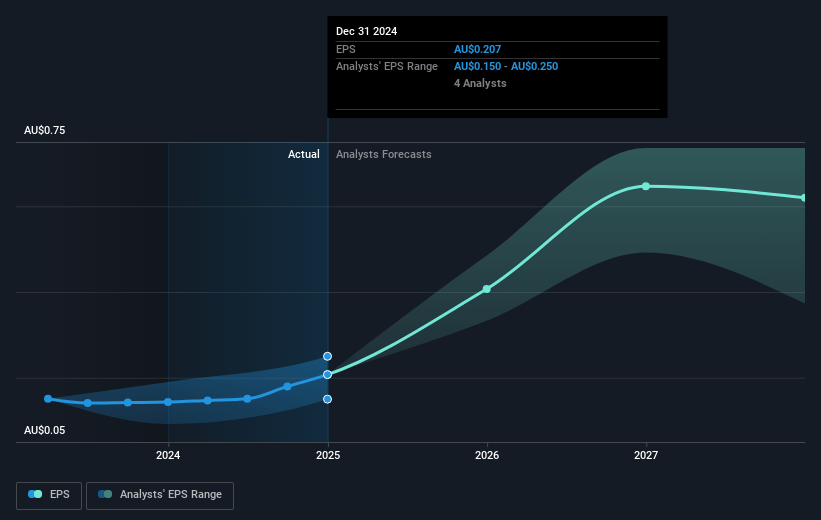

- Analysts expect earnings to reach A$687.5 million (and earnings per share of A$0.58) by about April 2028, up from A$223.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting A$836 million in earnings, and the most bearish expecting A$427.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.9x on those 2028 earnings, down from 11.7x today. This future PE is lower than the current PE for the AU Metals and Mining industry at 12.1x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.53%, as per the Simply Wall St company report.

West African Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's reliance on Burkina Faso's regulatory environment, particularly changes in local content regulations that affect contractor agreements, could increase operational costs or create logistical challenges, impacting net margins.

- Delays in the availability of key infrastructure, such as grid power for the Kiaka project, could result in increased operating costs from reliance on diesel power, affecting earnings.

- A substantial portion of cash flow is being directed towards capital investment in the Kiaka project, which could strain cash resources if unexpected issues arise, impacting net earnings.

- The future production increase is contingent upon successful completion and ramp-up of the Kiaka project, introducing execution risk that could influence projected revenue if not met.

- While the company remains unhedged, fluctuations in gold prices present a risk to revenue stability, with potential negative impacts on net margins if prices fall.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$3.537 for West African Resources based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$4.55, and the most bearish reporting a price target of just A$2.8.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$2.1 billion, earnings will come to A$687.5 million, and it would be trading on a PE ratio of 8.9x, assuming you use a discount rate of 7.5%.

- Given the current share price of A$2.3, the analyst price target of A$3.54 is 35.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.