Last Update 23 Jun 26

Fair value Increased 0.30%IAG: Dividends Buyback And Climate Resilience Will Support Measured Future Returns

Analysts have made a small upward adjustment to their fair value estimate for Insurance Australia Group, lifting it from A$8.32 to A$8.35, citing updated assumptions for revenue trends, profit margins and the stock's future P/E multiple.

What’s in the News for Insurance Australia Group

- Insurance Australia Group is backing prefabricated and modular building techniques for disaster recovery, aiming to shorten rebuild times and manage claims costs more efficiently, according to recent coverage.

- The company is highlighting climate resilience measures, including disciplined underwriting and the use of reinsurance, as part of its response to rising natural catastrophe exposure, based on recent news reports.

- Recent articles report that Insurance Australia Group reached a confidential settlement with the administrators of collapsed Greensill Capital, resolving significant Federal Court claims that had been an overhang for the stock.

- News sources note that the company is running an on market share buyback and other capital management measures. These have been presented as signals of management confidence in Insurance Australia Group’s valuation.

- Commentary on the sector points to Insurance Australia Group’s premium volumes in motor and home insurance and the expansion of its RACQI franchise in Queensland, alongside references to its regulatory capital position and dividend and buyback activity, as context for its role as a defensive income stock on the ASX.

Valuation Changes for Insurance Australia Group

- Fair Value: Nudged higher from A$8.32 to A$8.35. This reflects a very small adjustment to the central valuation point for Insurance Australia Group.

- Discount Rate: Held effectively steady at about 7.00%. This indicates no meaningful change in the rate used to discount future cash flows.

- Revenue Growth: The assumed revenue contraction has been revised slightly, with the decline now set at about 13.08%, compared with the prior 13.07% decline.

- Net Profit Margin: Margin expectations have been trimmed marginally to about 10.11%, from 10.12%. This implies a very small shift in expected profitability.

- Future P/E: The assumed future P/E multiple has edged up from 19.92x to 20.02x, signalling a modestly higher valuation multiple in the model.

Key Takeaways

- Overly optimistic assumptions on customer growth, margin expansion, and M&A synergies could expose downside if execution or market conditions disappoint.

- Rising competition, technological uncertainty, and climate-related claims risk threaten growth, profitability, and long-term sector dominance.

- Strong growth momentum, conservative risk management, and ongoing tech investment position IAG for sustained margin expansion, market share gains, and improved shareholder returns.

Catalysts

About Insurance Australia Group- Insurance Australia Group Limited underwrites general insurance products and provides investment management services in Australia and New Zealand.

- The stock appears to be pricing in continued robust revenue and earnings growth from expected organic customer gains, boosted by IAG's strong brand portfolio and advanced digital platforms that increase policy retention and simplify customer acquisition; any disappointment in customer growth rates or market share could pressure top-line and net income in future periods.

- Investors seem to be assuming substantial near

- and medium-term operating margin expansion as heavy investment in risk analytics, AI underwriting, and process automation will rapidly drive higher efficiency and lower claims ratios; however, if technology implementation lags, or cost savings prove slower to materialize, operating leverage and net margins could be lower than current expectations.

- Current valuation likely factors in sustained favorable conditions for property and catastrophe insurance, as heightened climate risk awareness is expected to expand IAG's gross written premiums and addressable market; if future weather events are more severe or frequent than modeled, claims could spike and reinsurance costs rise, harming profitability.

- The market may be too optimistic regarding long-term sector consolidation benefiting IAG, assuming disciplined pricing and low competition will persist; if disruptive digital-first competitors or insurtechs gain traction faster than anticipated, market share erosion and price competition could crimp revenue growth and profitability.

- There seems to be an expectation for the integration of large acquisitions (RACQ, RAC WA) to deliver quick and substantial synergy benefits to group earnings and EPS; however, if integration is slower, cost savings less than forecast, or reinsurance/IT challenges emerge, realized earnings accretion could lag current projections, impacting reported earnings growth.

Insurance Australia Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

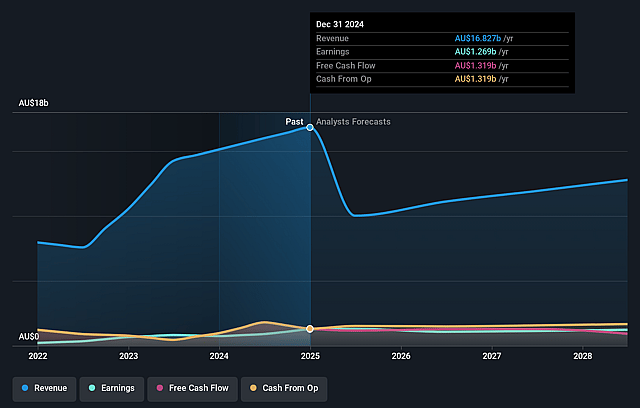

- Analysts are assuming Insurance Australia Group's revenue will decrease by 13.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.9% today to 10.1% in 3 years time.

- Analysts expect earnings to reach A$1.2 billion (and earnings per share of A$0.51) by about June 2029, up from A$1.1 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as A$1.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 20.0x on those 2029 earnings, up from 17.8x today. This future PE is greater than the current PE for the AU Insurance industry at 19.5x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent organic growth in retail customer numbers and high policy retention rates, along with scalable technology platforms, suggest IAG is well positioned to expand revenue and market share, especially with the successful migration of policies to the Retail Enterprise Platform expected to drive further customer and premium growth.

- The acquisition of RACQ and RAC in WA, which will add around $3 billion of premiums and at least $300 million in insurance profits, is projected to deliver double-digit earnings per share accretion and support ongoing revenue and earnings growth.

- Mature and conservative reinsurance arrangements, featuring downside protection against perils volatility and profit-sharing mechanisms, provide margin stability and potential upward bias to net margins and earnings in periods of benign claims experience.

- Robust capital position, disciplined underwriting, and consistent margin delivery (targeting 14%-16%, with a through-the-cycle goal of 15%) backed by improving claims efficiency and supply chain management, indicate the likelihood of maintaining healthy net margins and sustainable earnings.

- Continued investment in technology (including AI and advanced efficiencies), process automation, and integration of acquisitions is forecast to lower the expense ratio, expand operating leverage, and further enhance net margins and shareholder returns over the medium to long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$8.35 for Insurance Australia Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$10.0, and the most bearish reporting a price target of just A$6.8.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be A$12.0 billion, earnings will come to A$1.2 billion, and it would be trading on a PE ratio of 20.0x, assuming you use a discount rate of 7.0%.

- Given the current share price of A$8.28, the analyst price target of A$8.35 is 0.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Insurance Australia Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.