Last Update 23 Jun 26

Fair value Increased 0.46%506285: Dividend Strength And Compostable Nursery Initiative Will Support Upside Potential

The analyst price target for Bayer CropScience has been modestly adjusted to ₹5,186.83 from ₹5,163. This reflects updated views on a slightly higher profit margin outlook, a revised discount rate and a recalibrated future P/E assumption.

What's in the News

- Natur-Tec India Private Limited and Bayer CropScience signed a Memorandum of Understanding to jointly develop biodegradable and compostable seedling cups aimed at replacing single-use plastic nursery cups, with designs intended to work alongside common nematicides and fungicides. (Source: Key Developments)

- The planned seedling cups are designed to support early stage seedling growth, including germination, root development and vigor during crop protection treatments, and to break down within typical transplant cycles to help reduce nursery waste and support a circular economy. (Source: Key Developments)

- Pilot trials for the compostable seedling cups are scheduled in vegetable and fruit nurseries across India, with measurements focused on germination, growth parameters and yield outcomes, followed by a plan to scale across India and internationally after validation. (Source: Key Developments)

- Bayer CropScience scheduled a Board Meeting on May 26, 2026, to consider audited financial results for the quarter and financial year ended March 31, 2026, and to consider recommending a final dividend for the 2025–26 financial year. (Source: Key Developments)

- At the Board Meeting on May 26, 2026, Bayer CropScience recommended a final dividend of ₹60 per share, subject to shareholder approval at the upcoming Annual General Meeting. (Source: Key Developments)

Valuation Changes for Bayer CropScience

- Fair Value: The analyst fair value estimate for Bayer CropScience has been nudged higher from ₹5,163 to ₹5,186.83.

- Discount Rate: The discount rate has risen slightly from 12.64% to 12.67%, indicating a marginally higher required return in the model.

- Revenue Growth: Forecast revenue growth has been trimmed from 9.77% to 8.30%, reflecting a more conservative topline outlook in the valuation inputs.

- Net Profit Margin: The assumed net profit margin has been raised from 13.12% to 14.06%, pointing to expectations of stronger profitability on each ₹ of revenue.

- Future P/E: The future P/E assumption has been reduced from 33.0x to 32.21x, implying a slightly lower valuation multiple applied to projected earnings.

Key Takeaways

- Strategic cost reductions and efficiency improvements are expected to enhance net margins and unlock substantial additional cash.

- Developing biological solutions and biofuels aims to offer new revenue streams, boosting future growth prospects.

- Regulatory challenges, market cyclicality, and rising production costs threaten Bayer CropScience's profitability and revenue stability, compounded by competitive pressures from generics and climate change complications.

Catalysts

About Bayer CropScience- Engages in the manufacture, sale, and distribution of insecticides, fungicides, herbicides, and various other agrochemical products and corn seeds in India, Germany, Bangladesh, and internationally.

- Bayer CropScience plans to capitalize on its innovation pipeline, with a focus on seeds and traits, predicting incremental sales of over EUR 3.5 billion by 2029, which will significantly drive revenue.

- The company aims to expand its EBITDA margin annually by 100 to 150 basis points through controllable measures within a diversified margin program, impacting earnings positively.

- Strategic cost reductions and efficiency improvements across R&D, product supply, and go-to-market approaches are expected to unlock over EUR 1 billion in margin improvement and more than EUR 1.5 billion in cumulative cash, enhancing net margins.

- Dedicated efforts toward developing new value pools, such as biological solutions and biofuels, are anticipated to provide significant additional revenue streams by 2030, positively influencing future growth.

- By pursuing strategic divestments and optimizing the portfolio, Bayer CropScience expects to streamline operations and enhance free cash flow, estimating over EUR 3 billion in free operating cash flow by 2029.

Bayer CropScience Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

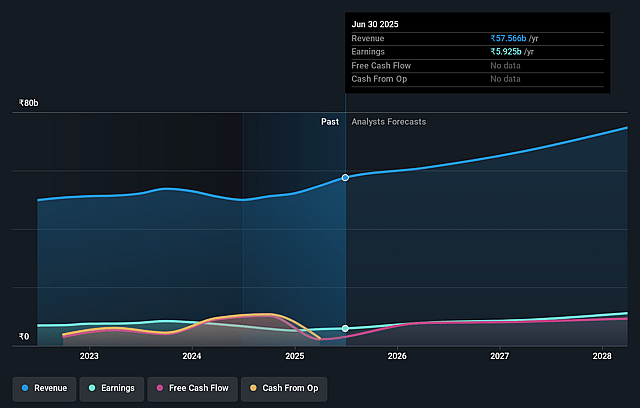

- Analysts are assuming Bayer CropScience's revenue will grow by 8.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.1% today to 14.1% in 3 years time.

- Analysts expect earnings to reach ₹10.1 billion (and earnings per share of ₹225.8) by about June 2029, up from ₹6.9 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 32.9x on those 2029 earnings, up from 27.3x today. This future PE is greater than the current PE for the IN Chemicals industry at 21.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.67%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Bayer CropScience is experiencing pricing pressures in its Crop Protection segment due to the increase in generics, specifically from Chinese producers, which could lead to strained profit margins. This impacts net margins and overall profitability.

- Regulatory disruptions in Europe and other regions can lead to significant sales losses, impacting revenue growth and creating uncertainty around future earnings.

- Cyclical nature and volatility in the agriculture market, driven by factors such as grain prices and currency fluctuations, can lead to unpredictable revenue and earnings outcomes.

- Climate change and increasing pest pressures add complexity and risk in product planning, potentially affecting yields and future revenue streams.

- Rising production costs in Europe and North America, contrasted with lower costs in regions like China, can disadvantage Bayer's cost structure, further pressuring net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹5186.83 for Bayer CropScience based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹72.1 billion, earnings will come to ₹10.1 billion, and it would be trading on a PE ratio of 32.9x, assuming you use a discount rate of 12.7%.

- Given the current share price of ₹4193.3, the analyst price target of ₹5186.83 is 19.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bayer CropScience?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.