Last Update 22 Jun 26

8572: Rising Dividends And Earnings Guidance Will Support Future Shareholder Returns

Acom's latest narrative update keeps the analyst fair value target steady at ¥501.25. There are slight tweaks to the discount rate, profit margin and forward P/E assumptions as analysts fine-tune their models without changing the overall valuation view.

What’s in the News for Acom

- Acom issued new consolidated and non consolidated earnings guidance for the first half and full year ending March 31, 2027, including targets for operating revenue, operating profit and basic earnings per share across both reporting bases. [Source: Company guidance]

- The company proposed a full year dividend for the year ended March 31, 2026 of ¥12.00 per share, compared with ¥7.00 per share paid a year earlier. Payment is scheduled for June 24, 2026, with a shareholders meeting on June 23, 2026. [Source: Dividend proposal]

- For the second quarter of the fiscal year ending March 31, 2027, Acom outlined dividend expectations of ¥11.00 per share, compared with ¥10.00 per share a year earlier. [Source: Dividend outlook]

- Acom revised its year end dividend forecast for the year ended March 31, 2026 to ¥12.00 per share, compared with a previous forecast of ¥10.00 per share. The company guided for an annual dividend of ¥24.00 per share based on its policy of emphasizing stable and continuous shareholder returns. [Source: Dividend forecast revision]

- The company raised its consolidated and non consolidated earnings forecasts for the year ended March 31, 2026, updating expectations for operating revenue, operating profit, profit attributable to owners of parent and basic earnings per share after reassessing interest on operating loans, yen depreciation effects and operating expenses. [Source: Earnings guidance revision]

Valuation Changes

- Fair Value: Analyst fair value estimate for Acom remains unchanged at ¥501.25 per share, indicating no shift in the core valuation outcome from the updated model.

- Discount Rate: The discount rate has risen slightly from 7.64% to about 7.76%, reflecting a modest adjustment to the required return used in the valuation.

- Revenue Growth: The revenue growth assumption is effectively unchanged at around 4.96%, implying no material revision to Acom's topline outlook within the model.

- Net Profit Margin: The net profit margin assumption remains effectively stable at about 18.13%, suggesting only a technical refinement rather than a directional change in profitability expectations.

- Future P/E: The future P/E multiple has risen slightly from about 13.83x to roughly 13.87x, a minor recalibration of how Acom's earnings are capitalized in the model.

Key Takeaways

- Strong loan and credit demand and strategic international growth could significantly boost Acom's future revenues and earnings.

- Effective financial strategies, including cost management and innovative services, are expected to support profit growth and net margin stability.

- A data breach and rising financial expenses pose risks to ACOM's reputation and earnings, while regulatory changes and economic volatility challenge revenue growth.

Catalysts

About Acom- Offers loans, credit cards, and loan guarantee services in Japan and internationally.

- The strong loan demand and receivables growth in both the Loan and Credit Card business, and the Guarantee business, indicate a potential for increased operating revenue in the future. This growth is crucial for increasing revenue and could enhance overall earnings.

- ACOM's international operations, especially in Thailand, the Philippines, and Malaysia, show potential for sustained growth despite some regional challenges. As these economies grow, ACOM's revenues and earnings from international operations could similarly benefit.

- The company's focus on embedded finance, highlighted through the GeNiE's Money Lamp service, can create new revenue streams by integrating lending services into existing digital platforms. This innovation is expected to drive future revenue growth.

- ACOM's strategy to manage funding costs effectively by optimizing long-term and short-term debt balance, protected mostly against rate hikes, supports maintaining net margins despite rising interest rates. This financial strategy is essential for future profit growth.

- The decline in claims for interest repayments and the related decreases in reserves suggest a potential for lower financial expenses in the future, positively impacting net margins and profitability.

Acom Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

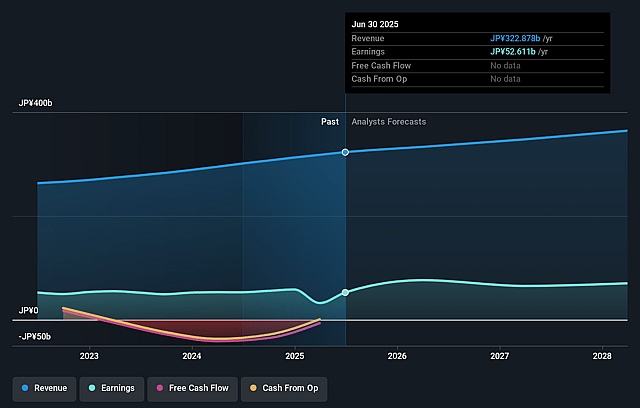

- Analysts are assuming Acom's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 23.6% today to 18.1% in 3 years time.

- Analysts expect earnings to reach ¥70.8 billion (and earnings per share of ¥45.2) by about June 2029, down from ¥79.6 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.9x on those 2029 earnings, up from 8.8x today. This future PE is greater than the current PE for the JP Consumer Finance industry at 10.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.76%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The data breach involving customer personal information, although contained, could damage ACOM’s reputation and impact customer trust, affecting future revenue and market positioning.

- Economic volatility in overseas markets might affect Japan’s economy and dampen personal consumption, potentially impacting ACOM’s loan demand and revenue growth.

- The introduction of responsible lending requirements in Thailand might affect future loan expectations and revenue in the region due to tighter regulations.

- The increasing provision for bad debt, particularly with newer borrowers, indicates a potential risk to net margins and could continue to affect earnings until loan stability is achieved.

- Rising financial expenses due to higher market rates, both in Japan and Thailand, could increase operational costs and impact net earnings if interest rates continue to climb.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ¥501.25 for Acom based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ¥390.5 billion, earnings will come to ¥70.8 billion, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 7.8%.

- Given the current share price of ¥448.6, the analyst price target of ¥501.25 is 10.5% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Acom?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.