Last Update 26 Jun 26

Fair value Decreased 0.48%FYB: Confirmed 2025 And 2026 Revenue Guidance Will Support Bullish Outlook

Analysts have trimmed their price target for Formycon slightly to about €39.67 from around €39.86. This reflects updated views on discount rates, growth assumptions and future P/E expectations.

What’s in the News for Formycon

- Formycon confirmed earnings guidance for fiscal 2026, stating that the group expects revenue in a range of €60.0 million to €70.0 million. (Source: Company guidance)

- Formycon provided earnings guidance for fiscal 2026, indicating an expected revenue range of €60.0 million to €70.0 million for the Formycon Group. (Source: Company guidance)

- Formycon maintained earnings guidance for 2025, with preliminary group revenues stated at approximately €45 million. (Source: Company guidance)

- Formycon and licensing partner Klinge Biopharma announced the European Union launch of FYB203, a biosimilar to Eylea 2mg, under the Ahzantive and Baiama brands in pre-filled syringes for intravitreal injections. (Source: Product announcement)

- The FYB203 rollout began on May 15, 2026, in key markets including Germany, France and Italy, with additional Central and Eastern European countries and vial presentations planned over the coming months, supported by settlement and licensing agreements with Regeneron Pharmaceuticals and Bayer Healthcare. (Source: Product announcement)

Valuation Changes

- Fair Value was trimmed slightly from €39.86 to €39.67, indicating only a small adjustment to the central valuation estimate for Formycon.

- The Discount Rate was nudged up from 5.26% to 5.32%, which generally means a marginally higher required return is being applied to Formycon.

- Revenue Growth was revised from 46.67% to 41.09%, pointing to a lower projected growth rate for future € revenue.

- The Net Profit Margin was adjusted from 46.91% to 40.13%, reflecting a reduced assumed profitability level on future € earnings.

- The Future P/E was raised from 10.21x to 13.37x, implying that a higher earnings multiple is now being used for Formycon in forward-looking estimates.

Key Takeaways

- Waiving the Phase III study for FYB206 cuts significant R&D costs, improving net margins and freeing capital for other uses.

- Strategic regional expansions and targeted product introductions, like the FYB201 syringe, boost market penetration and revenue potential.

- Market volatility, deferred tax liabilities, litigation, and rising costs threaten Formycon's revenue and financial performance amidst biosimilar sales challenges in the U.S.

Catalysts

About Formycon- A biotechnology company, develops biosimilar drugs in Germany and Switzerland.

- The waiver of the Phase III study for the KEYTRUDA biosimilar (FYB206) reduces R&D expenses by over €75 million over the next four years, freeing up capital and improving future net margins.

- Strategic expansion into new regions such as Latin America, MENA, and others with biosimilar products enhances market penetration and potential revenue growth.

- Introduction of a prefilled syringe for FYB201 in European markets is expected to drive market adoption and improve sales, positively impacting revenue.

- Continued regulatory progress and approvals, such as in Canada and the U.K., are expected to lead to new market entries and bolster revenue streams.

- Partnership strategies focusing on regional rather than global deals for FYB206, which could lead to incremental revenue from milestone payments and diversified commercial partnerships.

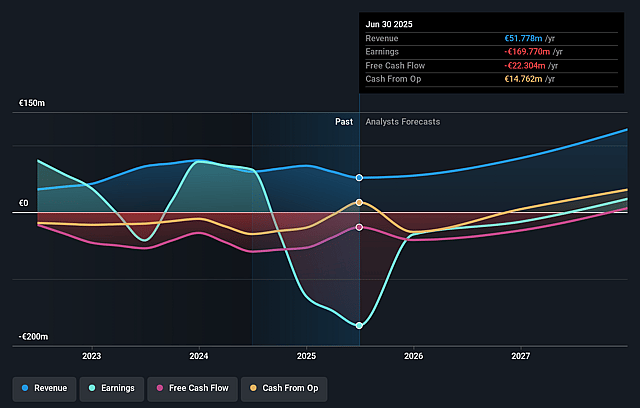

Formycon Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Formycon's revenue will grow by 41.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from -108.8% today to 40.1% in 3 years time.

- Analysts expect earnings to reach €58.9 million (and earnings per share of €0.85) by about June 2029, up from -€56.9 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €-18.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.9x on those 2029 earnings, up from -6.0x today. This future PE is lower than the current PE for the DE Biotechs industry at 94.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.32%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The halting of product sales by Sandoz in the U.S. due to falling reimbursement prices raises concerns about potential revenue loss and reflects the market's volatility impacting formycon's earnings.

- FYB202 faces significant deferred tax liabilities and an impairment, indicating high uncertainty in financial performance and impacting net margins.

- The dynamic market environment for biosimilars in the U.S. requires flexible commercial strategies, yet a year-long pause in sales for some products indicates potential revenue stagnation.

- Ongoing litigations for products like FYB203 contribute to uncertainty in market entry and revenue timing.

- Rising development and operational costs for projects like FYB208 and the uncertain success rates of strategic partnerships for FYB206 may suppress net financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €39.67 for Formycon based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €51.0, and the most bearish reporting a price target of just €30.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €146.8 million, earnings will come to €58.9 million, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 5.3%.

- Given the current share price of €19.28, the analyst price target of €39.67 is 51.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Formycon?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.