Last Update 23 Jun 26

AFN: Governance Reset And Board Review Will Support Renewed Confidence

Analysts have raised their average CA$ price target on Ag Growth International, citing recent target increases from several firms and upgraded views on the stock as supporting factors for the higher valuation range.

Analyst Commentary

Recent research on Ag Growth International shows a mix of optimism and caution, with several firms revising price targets and ratings in both directions over the past few updates. For you as an investor, the key takeaway is that analysts are actively reassessing where the stock should trade based on their views of execution, balance sheet risk, and growth potential.

Bullish Takeaways

- Bullish analysts have recently raised their CA$ price targets, which signals a higher assessed fair value for Ag Growth International relative to earlier views.

- Upgrades in rating suggest improved confidence in the company’s ability to execute on its plans and support higher long term earnings power.

- The cluster of upward target revisions indicates that, among more optimistic analysts, the risk or discount previously applied to the stock is being reconsidered.

- Supportive commentary around the latest target increases points to a view that recent developments at Ag Growth International justify revisiting prior, more conservative assumptions.

Bearish Takeaways

- Within the same research set, some bearish analysts have lowered their CA$ price targets, which points to concern that prior expectations for Ag Growth International were too high.

- Downgrades in rating reflect a more cautious stance on execution risk, with these analysts less confident that the company will meet earlier growth or profitability assumptions.

- Reduced targets from the more cautious group imply greater focus on potential downside scenarios, such as slower growth, margin pressure, or balance sheet constraints.

- The combination of downgrades and lower targets highlights that, while there is upside argued by some, others see limited room for multiple expansion without clearer evidence of consistent performance.

What's in the News for Ag Growth International

- Ag Growth International has formed a Strategic Review Committee of independent directors to evaluate a range of potential alternatives intended to maximize shareholder value, with external financial and legal advisors to be engaged as needed. Source: Company key developments.

- The company reached a cooperation agreement with Plantro Ltd., under which Plantro withdrew its plan to nominate three directors in return for Ag Growth International agreeing to appoint Mick MacBean and Gary Anderson to the Board following the June 4, 2026 annual and special meeting. Source: Company key developments.

- Plantro Ltd. and Tim Close have publicly called for Board changes and a formal review and potential sale process for Ag Growth International, including the nomination of new directors and a shareholder resolution urging a sale of the company. Source: Company key developments.

- Ag Growth International has undergone leadership changes, including confirming Paul Brisebois as permanent Chief Executive Officer and announcing the resignation of Chief Financial Officer Jim Rudyk. SVP of Finance Nicolle Parker is stepping in as interim CFO while a search for a new CFO begins. Source: Company key developments.

- The company has suspended its quarterly cash dividend, which had been set at an annualized $0.60 per common share, and announced a broad business reorganization that includes leadership restructuring, consolidation of operations into Winnipeg headquarters, changes to compensation structures, and termination of an ERP deployment plan. Source: Company key developments.

Valuation Changes for Ag Growth International

- Fair Value: The CA$26.14 fair value estimate is unchanged, indicating no adjustment in the core valuation anchor for Ag Growth International.

- Discount Rate: The 11.43% discount rate remains the same, so the required return used to assess the stock has not shifted.

- Revenue Growth: The revenue growth assumption remains effectively flat, with only a very small refinement in the projected decline.

- Net Profit Margin: The net profit margin expectation is effectively unchanged at approximately 11.62%, reflecting only a minor technical adjustment.

- Future P/E: The future P/E assumption remains steady at roughly 4.40x, indicating no material change in the multiple applied to projected earnings.

Key Takeaways

- Global expansion and infrastructure investments are driving diversified, visible revenue growth, supported by strong demand trends and a robust project pipeline.

- Operational improvements, financial discipline, and innovation are enhancing margins, boosting cash flow, and positioning for long-term market leadership.

- Weak Farm segment demand, high financial leverage, and dependence on key commercial projects create significant operational and financial risks amid ongoing costly transformation and evolving industry trends.

Catalysts

About Ag Growth International- Manufactures and distributes equipment for bulk agriculture commodities worldwide.

- Rapid international commercial expansion-especially in Brazil, EMEA, and India-driven by large-scale processing, handling, and storage projects, is diversifying revenue sources and creating a strong, growing order book (+15% year-over-year in Commercial), indicating visibility into sustained revenue growth through late 2025 and into 2026.

- Increasing investments in food security and agricultural infrastructure globally, including government-backed projects (e.g., corn ethanol, soy crushing, fertilizer capacity) and secular trends of higher food demand and supply chain resilience, are supporting long-term demand for AGI's integrated solutions, benefiting both revenue and margin growth.

- Structural improvements in operational efficiency, including ongoing cost optimization and the ERP system rollout, are helping to offset mix-related margin pressures, with a clear pathway for EBITDA margin expansion as farm recovery occurs and the revenue mix normalizes.

- Monetization of long-term receivables, especially in Brazil, combined with disciplined capex and working capital management, is expected to materially reduce net leverage (from 3.9x towards the low 3x range), improve free cash flow, and enhance financial flexibility for future growth investments.

- Ongoing product innovation, digital offerings, and a premium brand position-alongside market share gains in strategic regions-position AGI to capitalize on broader industry shifts toward mechanization, automation, and more advanced storage/handling technology, supporting sustainable topline and margin expansion over the medium to long term.

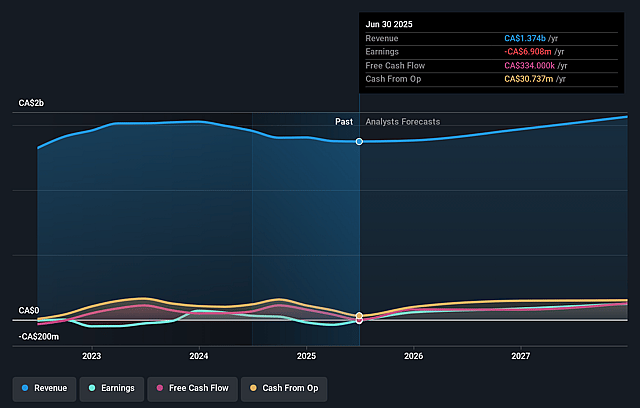

Ag Growth International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Ag Growth International's revenue will decrease by 1.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from -3.8% today to 11.6% in 3 years time.

- Analysts expect earnings to reach CA$156.2 million (and earnings per share of CA$4.28) by about June 2029, up from -CA$53.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 4.4x on those 2029 earnings, up from -7.2x today. This future PE is lower than the current PE for the CA Machinery industry at 24.0x.

- Analysts expect the number of shares outstanding to grow by 0.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.43%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent weakness in the Farm segment, including soft commodity prices, shifting tariff policies, uncertain subsidy programs, and elevated dealer channel inventories, has created challenging market conditions with limited visibility into recovery, potentially restricting revenue and margin growth if the segment remains subdued.

- Elevated net debt leverage ratio (3.9x) driven by sizable temporary working capital investments and customer financing-particularly in Brazil-poses financial risk; any delays or failures in receivables monetization strategies could constrain free cash flow and limit ability to invest in growth or withstand earnings volatility.

- Heavy dependence on the Commercial segment, especially large-scale projects in Brazil and EMEA, concentrates risk as a slowdown, project delay, or geopolitical/infrastructure shift in these markets could materially impact consolidated revenue and EBITDA.

- Ongoing ERP implementation and operational restructuring will continue to incur transformation costs through at least 2027, which may depress net margins and earnings in the medium term, especially if growth in higher-margin Farm segment does not materialize as anticipated.

- Secular trends toward automation, digitalization, and shifts in agricultural practices (e.g., precision farming, changing crop demand, sustainability demands) could outpace AGI's product innovation or dilute demand for traditional grain handling and storage equipment, impacting future topline growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$26.14 for Ag Growth International based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$30.0, and the most bearish reporting a price target of just CA$24.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CA$1.3 billion, earnings will come to CA$156.2 million, and it would be trading on a PE ratio of 4.4x, assuming you use a discount rate of 11.4%.

- Given the current share price of CA$20.61, the analyst price target of CA$26.14 is 21.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Ag Growth International?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.