Key Takeaways

- Expansion in HIV and Oncology divisions suggests potential for increased revenue through further expansion.

- Strategic partnerships and advances in Cell Therapy capabilities indicate a forward-looking approach to pipeline development and market leadership.

- Dependance on specific drugs and facing competition, manufacturing, and legal challenges could significantly impact Gilead Sciences' revenue and profitability.

Catalysts

What are the underlying business or industry changes driving this perspective?

- HIV and Oncology divisions are showing strong year-over-year growth, indicating potential for further expansion and increased revenue.

- More than 20 clinical updates expected in 2024 across various treatment areas, including Oncology and HIV, could lead to new approvals and expanded indications, driving future earnings growth.

- Investment in expanding Cell Therapy capabilities, particularly through reducing Yescarta manufacturing time, could enhance market leadership and contribute to revenue growth.

- Upcoming Phase III data for lenacapavir in HIV prevention and updates in the HIV treatment program might lead to new product launches and expanded use cases, positively impacting revenue.

- Strategic partnerships and acquisitions, as seen with Arcus and other collaborations, indicate a forward-looking approach to pipeline development, potentially leading to revenue growth from new therapeutic areas.

Assumptions

How have these above catalysts been quantified?

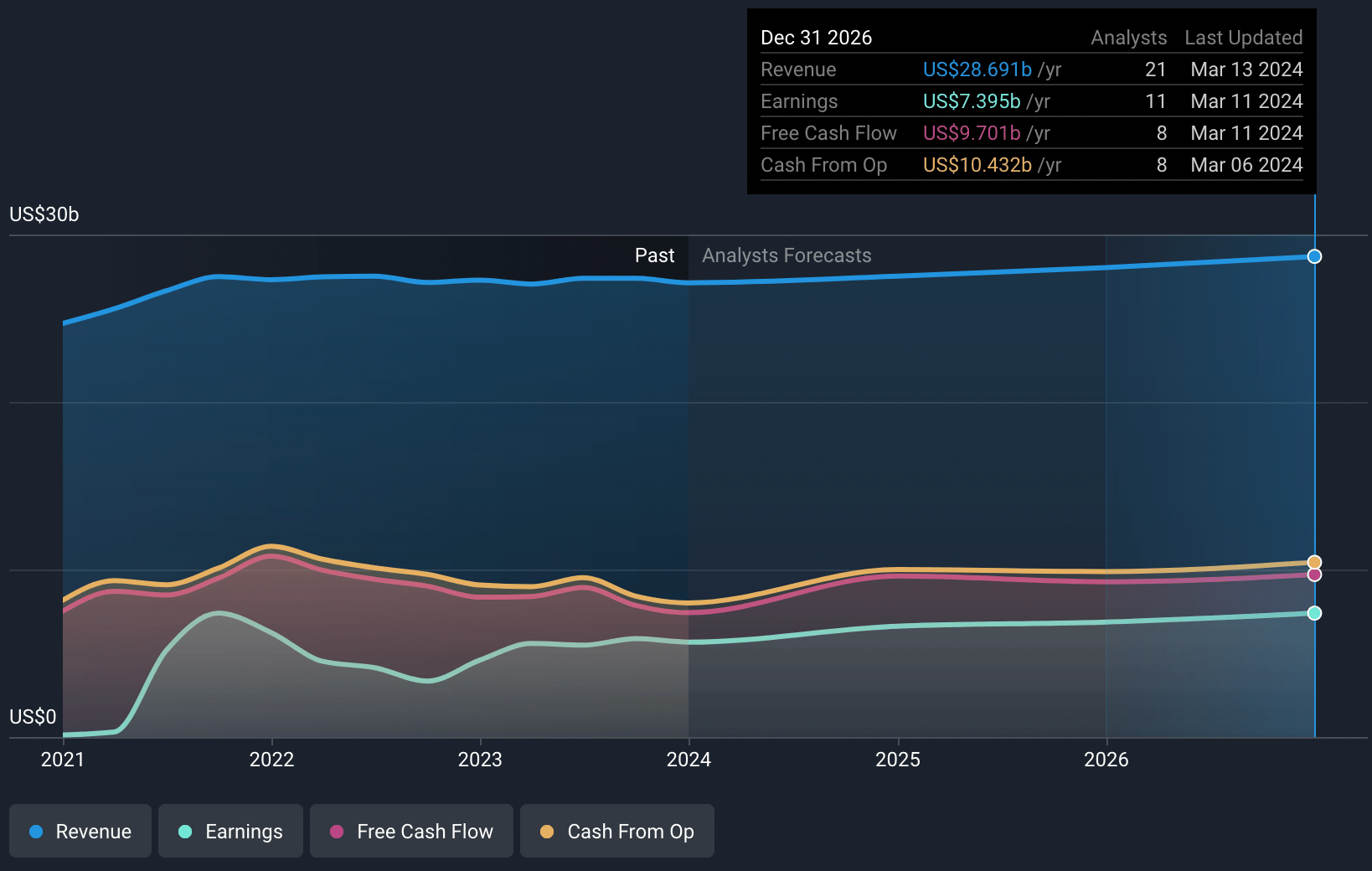

- Analysts are assuming Gilead Sciences's revenue will grow by 1.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 20.9% today to 25.8% in 3 years time.

- Analysts expect earnings to reach $7.4 billion (and earnings per share of $5.97) by about March 2027, up from $5.7 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.7x on those 2027 earnings, up from 16.3x today.

- To value all of this in today’s dollars, we will use a discount rate of 6.62%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The decline in Veklury (remdesivir) sales, as the need for COVID-19 treatments decreases, could lead to a significant reduction in revenue.

- The reliance on key products like HIV therapies, particularly Biktarvy, exposes the company to risks if competitive pressures or loss of market share occurs, potentially impacting revenue.

- Manufacturing challenges or delays, especially with innovative products like cell therapies, could affect the ability to meet demand, impacting revenue growth and profitability.

- The evolving competitive landscape in oncology, with ongoing investments in Trodelvy and CAR T-cell therapies, involves high R&D costs and execution risks which could impact net margins if these therapies do not meet sales expectations.

- Legal challenges related to drug development and patents, especially in the highly competitive HIV and oncology markets, could lead to unexpected financial liabilities or restrict market access, impacting earnings.

valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $87.64 for Gilead Sciences based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with this, you'd need to believe that by 2027, revenues will be $28.7 billion, earnings will come to $7.4 billion, and it would be trading on a PE ratio of 16.7x, assuming you use a discount rate of 6.6%.

- Given the current share price of $74.21, the analyst's price target of $87.64 is 15.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company’s future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.’s analysis may not factor in the latest price-sensitive company announcements or qualitative material.