Last Update 24 Jun 26

8591: Leadership Changes And Shareholder Returns Will Guide A Balanced Future Outlook

Analysts have left their fair value estimate for ORIX broadly unchanged at around ¥6,328 per share. They cited only minor adjustments to the discount rate, long term revenue growth, profit margin assumptions, and future P/E expectations rather than any major shift in the fundamental outlook.

What’s in the News for ORIX

- ORIX appointed Satoru Matsuzaki as Representative Executive Officer, Deputy President, and COO of the Japan and Asia Pacific Business Unit, effective June 23, 2026. The company also began consolidating Greater China operations into its Asia Pacific Business Headquarters to tighten regional coordination and governance. (Source: recent company announcement)

- Executive Officer Hao Li, former head of the Greater China Group, is retiring as ORIX integrates its Greater China operations into the wider Asia Pacific structure. The move reflects a shift toward a more unified regional organization. (Source: recent company announcement)

- Recent commentary highlights ORIX stock’s 118.6% return over the past year, with some analysts describing the shares as undervalued based on P/B, P/S, and P/E metrics compared with industry peers. The stock is also cited as having a Zacks Rank #2 (Buy) rating. (Source: Zacks / market coverage)

- Management guidance points to higher net income targeted for the fiscal year ending March 31, 2027, together with an authorized share repurchase program and an increased annual dividend. These measures are described as signaling an emphasis on shareholder returns. (Source: company guidance and board resolutions)

- Media reports indicate Apollo Global Management is in early stage talks that include considering a potential acquisition of an ORIX life insurance subsidiary in Japan, with regulatory approval identified as a key uncertainty. (Source: Financial Times report)

Valuation Changes

- Fair Value: The fair value estimate for ORIX remains unchanged at ¥6,327.78 per share, indicating no revision to the central valuation level.

- Discount Rate: The discount rate has fallen slightly from 5.11% to 5.05%, reflecting a small adjustment in the required return used in the valuation model.

- Revenue Growth: The long term revenue growth assumption is effectively unchanged at 4.49%, with only an immaterial rounding difference between the prior and updated figures.

- Net Profit Margin: The net profit margin assumption is effectively unchanged at 14.17%, with only a very minor numerical adjustment in the model.

- Future P/E: The assumed future P/E multiple has edged down slightly from 13.81x to 13.79x, indicating a small reduction in the valuation multiple applied to ORIX earnings.

Key Takeaways

- Strategic divestments and investments in green energy and asset management enhance growth, profitability, and exposure to sustainability trends.

- Expanding global asset management, fee-based revenue, and digitalization drive operating efficiency, diversify income, and improve long-term earnings stability.

- Profit growth is driven by one-off asset sales and volatile gains, raising concerns over sustainability amid macroeconomic uncertainties, asset impairments, and constrained long-term revenue visibility.

Catalysts

About ORIX- Provides financial services in Japan, the United States, Asia, Europe, and Australasia.

- ORIX's ongoing capital recycling strategy, highlighted by portfolio optimization through divesting non-core assets (e.g., the sale of Greenko and ORIX Asset Management & Loan Services), and reallocating proceeds into higher-growth areas like green energy and private asset management, is expected to drive higher ROE and long-term net income growth.

- The company is leveraging the global increase in demand for alternative and private capital, as seen by robust inflows at Robeco and strong growth in third-party AUM (¥81 trillion, up ¥7 trillion in three months), pointing to a secular shift towards sustainable fee-based revenue and improving margins.

- Substantial expansion into renewable energy and sustainable infrastructure projects (e.g., AM Green, Kinokawa Energy Storage Plant, Elawan electricity sales, Ormat stake), coupled with demonstrated project pipeline and new investments, positions ORIX to benefit from long-term sustainability trends driving both recurring revenue and valuation multiples.

- Digitalization efforts, such as success in U.S. CLO and securitization product arrangements and Rentec's ICT equipment rental growth, support operational leverage and efficiency in diversified financial services-enabling higher operating margins and resilience in core businesses.

- The continued globalization and shift in ORIX's asset management footprint (e.g., Hilco Global acquisition, growth in private credit, expanding U.S. and European platforms) is set to further increase steady fee income and diversify revenue streams, reducing earnings volatility and enhancing long-term earnings quality.

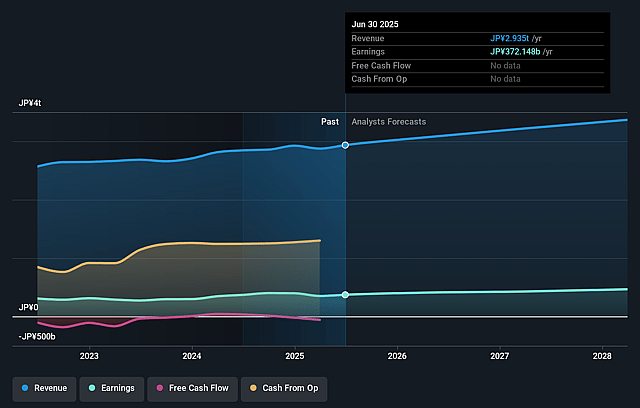

ORIX Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming ORIX's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.4% today to 14.2% in 3 years time.

- Analysts expect earnings to reach ¥538.5 billion (and earnings per share of ¥529.73) by about June 2029, up from ¥447.2 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ¥615.7 billion in earnings, and the most bearish expecting ¥484.5 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.8x on those 2029 earnings, down from 15.6x today. This future PE is about the same as the current PE for the US Diversified Financial industry at 13.8x.

- Analysts expect the number of shares outstanding to decline by 2.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.05%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on capital gains from asset sales (e.g., Greenko and Hotel Universal Port VITA) and valuation gains to achieve profit growth, rather than recurring operational improvements, raises the risk of lumpy and unsustainable earnings, potentially impacting net income and future EPS growth.

- Persistent macroeconomic uncertainty, particularly high interest rates in key markets like the U.S., is negatively impacting core businesses such as real estate lending and private equity, leading to recognized impairments, conservative asset reduction, and lower segment profitability-potentially reducing revenue and net margins.

- Exposure to legacy asset impairments-including goodwill and credit losses in the U.S. as well as unrealized losses in ORIX Life's bond portfolio-creates a risk of significant capital losses or reserve build-ups, which could depress reported earnings and shareholder equity.

- Management's admission that certain profit increases are driven by technical or one-off factors (e.g., early recognition of banking segment profits and capital gains in energy) suggests that base profit momentum may not be sustainable if market conditions worsen, potentially leading to disappointing results and lower ROE.

- The need to repeatedly review and potentially delay investment decisions, capital recycling schedules, and major acquisitions due to uncertain market conditions or tariff/geo-political impacts may limit ORIX's ability to deploy capital efficiently or achieve stable AUM growth, constraining long-term revenue and margin expansion.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ¥6327.78 for ORIX based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥7500.0, and the most bearish reporting a price target of just ¥4800.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ¥3799.5 billion, earnings will come to ¥538.5 billion, and it would be trading on a PE ratio of 13.8x, assuming you use a discount rate of 5.1%.

- Given the current share price of ¥6342.0, the analyst price target of ¥6327.78 is 0.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ORIX?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.