Last Update 31 Jul 26

Fair value Increased 4.87%2379: Open Security Partnership Will Balance Modest Revisions To Earnings Outlook

Analysts have lifted their fair value estimate for Realtek Semiconductor from NT$618.69 to NT$648.80, citing updated assumptions for revenue growth, profit margins, a slightly lower discount rate, and a revised future P/E multiple.

What's in the News for Realtek Semiconductor

- Realtek Semiconductor has joined the OpenTitan project, an open source silicon Root of Trust initiative stewarded by lowRISC. Source: Key Developments

- Through OpenTitan, Realtek plans to focus on transparent, high quality hardware security across its telecommunications, networking, and IoT product portfolio. Source: Key Developments

- As an OpenTitan project partner, Realtek will work with other coalition members on silicon design, reference firmware, and verification collateral. Source: Key Developments

- Realtek intends to use OpenTitan’s vendor and platform agnostic IP to develop discrete hardware Root of Trust devices for data center servers, storage, peripherals, and edge devices. Source: Key Developments

- The addition of Realtek to OpenTitan follows the project’s move to bring a commercial quality open source Root of Trust chip design to market. Source: Key Developments

Valuation Changes for Realtek Semiconductor

- Fair Value has risen slightly from NT$618.69 to NT$648.80 based on updated assumptions.

- Discount Rate has edged lower from 9.83% to 9.78%, reflecting a modest adjustment to the risk profile used in the model.

- Revenue Growth assumption has been set higher from 12.54% to 13.87%, indicating a stronger outlook for NT$ revenue expansion in the forecasts.

- Net Profit Margin forecast has moved up from 12.37% to 12.76%, pointing to slightly improved expected profitability on future NT$ earnings.

- Future P/E multiple has been trimmed from 19.59x to 19.21x, implying a marginally lower valuation multiple applied to expected earnings.

Key Takeaways

- Strategic inventory management and diversification into high-growth sectors are driving revenue growth and operational resilience, boosting earnings stability.

- Focus on AI-enabled technologies and emerging innovations like smart glasses is poised to enhance market penetration and increase revenue.

- Geopolitical tensions and tariffs threaten Realtek's supply chain, demand, revenue growth, and margins, with competition and macroeconomic uncertainties exacerbating financial risks.

Catalysts

About Realtek Semiconductor- Engages in the research, development, production, and sale of various integrated circuits and related application software in Taiwan, Asia, and internationally.

- Realtek is capitalizing on strategic inventory build-ups, driven by customers preparing for market uncertainties, potentially resulting in boosted revenue growth as these inventories are utilized.

- Management expects continued demand in consumer electronics, networking, and automotive sectors, which are anticipated to enhance gross margins through product mix optimization with high-margin products like IoT devices and automotive Ethernet.

- The diversification of supply chain partnerships and market expansion efforts, particularly into high-growth areas like automotive and enterprise networks, are likely to drive sustainable revenue streams and improve operational resilience, positively impacting earnings stability.

- Realtek's strategic focus on AI-enabled and high-speed technology developments, including Wi-Fi 7 and advanced automotive Ethernet, presents potential catalysts for innovative product offerings, likely leading to increased revenue and higher net margins over time.

- Collaborations and advancements in emerging technologies such as smart glasses, humanoid robotics, and system-on-panel ESL indicate broader market penetration opportunities, potentially contributing to diversified and future revenue growth.

Realtek Semiconductor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

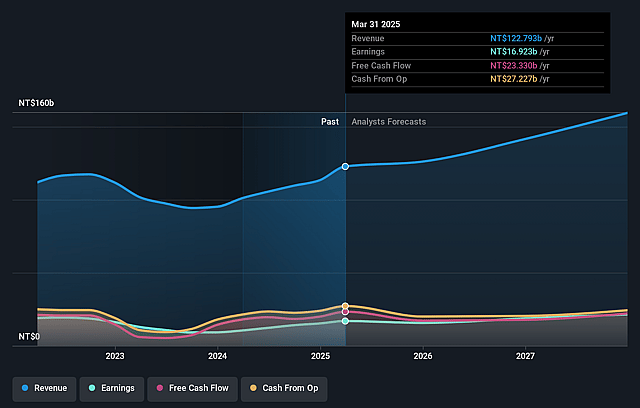

- Analysts are assuming Realtek Semiconductor's revenue will grow by 13.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.5% today to 12.8% in 3 years time.

- Analysts expect earnings to reach NT$23.4 billion (and earnings per share of NT$43.34) by about July 2029, up from NT$14.3 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as NT$27.4 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.2x on those 2029 earnings, down from 24.6x today. This future PE is lower than the current PE for the TW Semiconductor industry at 33.5x.

- Analysts expect the number of shares outstanding to grow by 0.52% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.78%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Geopolitical tensions and tariff uncertainties, particularly between the U.S. and China, may adversely impact Realtek's supply chain and market demand, affecting revenue growth and margins.

- Strategic customer order adjustments and potential pull-forward effects due to tariffs could lead to temporary demand distortions, affecting future revenue sustainability.

- Macroeconomic uncertainties and potential tariff impacts may dampen consumer and end-market demand, posing risks to revenue and net margins.

- Increased costs from tariffs or reshoring efforts could challenge Realtek’s ability to maintain high gross margins, especially if lower-margin products become more prevalent in a weakened macroeconomic environment.

- Heightened competition and potential oversupply issues in both domestic and international markets, driven by national self-sufficiency policies, could lead to irrational price competition, impacting Realtek’s revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NT$648.8 for Realtek Semiconductor based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NT$750.0, and the most bearish reporting a price target of just NT$540.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be NT$183.3 billion, earnings will come to NT$23.4 billion, and it would be trading on a PE ratio of 19.2x, assuming you use a discount rate of 9.8%.

- Given the current share price of NT$684.0, the analyst price target of NT$648.8 is 5.4% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Realtek Semiconductor?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.