Last Update 24 Jun 26

DHT: Tanker Rate Upside And Fleet Renewal Balance Reversion Risk

Analysts have adjusted their view on DHT Holdings with a higher consolidated price target, including a $5 increase from one firm, while another has taken a more cautious stance, citing both optimism around the company and concerns about potential reversion risk.

Analyst Commentary

Recent research on DHT Holdings highlights a split view, with some bullish analysts lifting their price targets and others turning more cautious on the stock's risk and return trade off. For investors, the key messages center on how current expectations line up with execution and the potential for reversion in the share price.

Bullish Takeaways

- Bullish analysts raised their price targets on DHT Holdings, which signals greater confidence in the stock's valuation support at current levels.

- The higher target levels imply that, in their view, DHT Holdings is positioned to justify a richer multiple if the company delivers on its current plan.

- Positive commentary highlights an improved risk reward profile, suggesting that upside potential is seen as more attractive relative to perceived execution risks.

- The revised targets indicate that bullish analysts see room for the stock to better reflect their outlook on the company’s fundamentals over time.

Bearish Takeaways

- Bearish analysts downgraded DHT Holdings and pointed to reversion risk, signalling concern that the stock price could move back toward prior trading levels if expectations prove too optimistic.

- The downgrade reflects caution that recent enthusiasm may already be embedded in the valuation, leaving less margin for error on execution.

- These analysts emphasize that, if current assumptions around the business do not play out as expected, downside risk to the stock could increase.

- Overall, the more cautious stance frames DHT Holdings as a stock where investors may need to weigh potential upside against the risk of a pullback from current pricing.

What’s in the News for DHT Holdings

- DHT Holdings was the focus of an upgrade in a recent report titled "DHT: The Strait Of Hormuz Is Open, VLCC Tanker Rates Set To Soar (Upgrade)," which cited robust Q1 results, strong Q2 guidance, and expectations around VLCC rate trends as key factors. [Source: Recent research summary]

- The same report highlighted that DHT Holdings keeps roughly 50% of its fleet on charter, which provides earnings stability but can limit upside when spot markets are strong. It also indicated no current plans to expand that charter coverage. [Source: Recent research summary]

- Commentary also pointed to DHT Holdings’ balance sheet, describing cash levels, debt profile, and a refinanced credit facility that supports a dividend payout policy tied to 100% of net income. [Source: Recent research summary]

- Geopolitical tensions around the Strait of Hormuz drew attention to tanker stocks, including DHT Holdings, after comments from President Donald Trump about Iran’s actions in the region. Observers noted the Strait’s importance for crude exports and the potential impact on freight rate volatility and war risk premiums. [Source: Trump’s Hormuz warning news]

- DHT Holdings reported progress in its fleet modernization program, taking delivery of the VLCC newbuilding DHT Gazelle, which will begin a five to seven year time charter with a major oil company. The company also confirmed the sale and delivery of the older vessel DHT China, with another Antilope class newbuilding and the sale of DHT Bauhinia scheduled around mid 2026. [Source: Company client announcement]

Valuation Changes for DHT Holdings

- Fair Value: The model fair value estimate is unchanged at $20.28 per share, indicating no adjustment to the core valuation output.

- Discount Rate: The discount rate remains steady at 7.11%, so the required return used in the valuation framework has not shifted.

- Revenue Growth: Assumed revenue growth continues to reflect a 13.31% decline, with no change in the modeled trajectory for DHT Holdings' top line.

- Net Profit Margin: The net profit margin assumption is stable at 54.51%, indicating no revision to expected profitability levels in the model.

- Future P/E: The forward valuation multiple assumption is unchanged at 17.13x P/E, so the earnings multiple applied to DHT Holdings has been kept consistent.

Key Takeaways

- Modern fleet renewal and disciplined capital strategy strengthen earnings stability, operational efficiency, and resilience through market cycles.

- Geopolitical shifts and tightening vessel supply create favorable conditions for higher utilization, stable cash flows, and improved profitability.

- Intensifying regulatory and market pressures threaten long-term revenue stability, with aggressive dividend policy and earnings volatility limiting financial flexibility and investment in fleet renewal.

Catalysts

About DHT Holdings- Through its subsidiaries, owns and operates crude oil tankers primarily in Monaco, Singapore, Norway, and India.

- Persistent growth in energy demand from emerging markets, notably in Asia, and evolving global refinery patterns are driving longer trade routes and increased ton-mile demand, supporting sustained high vessel utilization and, therefore, improved revenue visibility for DHT Holdings.

- DHT's active fleet renewal-selling older vessels and acquiring modern, fuel-efficient VLCCs-positions the company to capture premium charter rates and reduce operating expenses, likely supporting higher net margins and more stable long-term earnings.

- Attractive new time-charter fixtures and continued high-level customer interest, fueled by geopolitical shifts such as Indian sourcing changes and OPEC production decisions, are creating more predictable and resilient cash flows, positively impacting future revenue and earnings stability.

- Current limited global newbuild VLCC supply, shipyard constraints, and regulatory favor for newer, eco-efficient ships provide a supportive industry backdrop; DHT's modern fleet is well-positioned to benefit from tightening supply and potentially rising vessel day rates, aiding future profitability.

- Strong balance sheet, low leverage, competitive financing, and a disciplined capital allocation strategy (including dividend payouts and buybacks) enhance DHT's ability to invest in growth and navigate market cycles, supporting long-term EPS and shareholder returns.

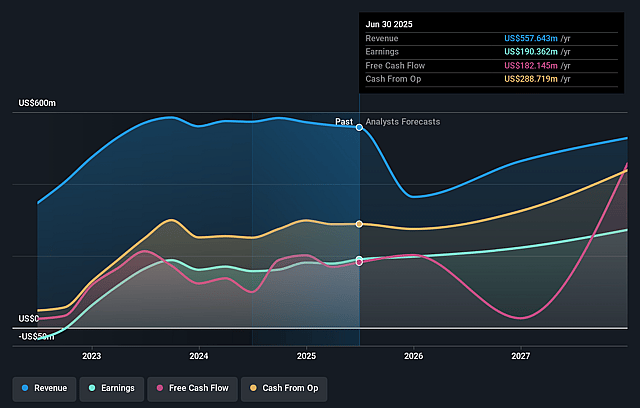

DHT Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming DHT Holdings's revenue will decrease by 13.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 50.3% today to 54.5% in 3 years time.

- Analysts expect earnings to reach $234.2 million (and earnings per share of $1.66) by about June 2029, down from $331.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $282.5 million in earnings, and the most bearish expecting $204.5 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.2x on those 2029 earnings, up from 9.7x today. This future PE is greater than the current PE for the US Oil and Gas industry at 13.0x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Increasing global momentum toward renewable energy and decarbonization could erode long-term demand for crude oil transportation, creating structural headwinds for VLCC utilization and DHT's future revenue streams.

- The company's aggressive policy of allocating 100% of ordinary net income as quarterly dividends may constrain retained earnings and reduce flexibility for fleet renewal or adoption of costly new technologies, thereby potentially impacting future earnings resilience.

- Persistent lack of scrapping in the sector due to high demand for older vessels in sanctioned trades could extend oversupply, pressuring freight rates industry-wide and negatively affecting DHT's revenues and net margins.

- Elevated acquisition and newbuilding capital expenditures to maintain fleet competitiveness, combined with potential increases in regulation-driven costs (e.g., compliance with environmental standards), could pressure net margins and require ongoing financing-especially if vessel earnings soften.

- Continued reliance on spot market exposure for a portion of the fleet results in earnings volatility during periods of weak rates or unfavorable macroeconomic conditions, with potential for prolonged periods of depressed cash flows and negative impact on net income.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $20.28 for DHT Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $23.0, and the most bearish reporting a price target of just $18.7.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $429.6 million, earnings will come to $234.2 million, and it would be trading on a PE ratio of 17.2x, assuming you use a discount rate of 7.1%.

- Given the current share price of $19.96, the analyst price target of $20.28 is 1.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on DHT Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.