Last Update 05 Jun 26

Fair value Decreased 0.97%FLOW: Future Returns Will Rely On Rebuilding Capital And Market Share

Analysts have trimmed their price target on Flow Traders to about €29.78 from about €30.07, citing weaker confidence around the company's capital build and market share trends, despite modestly firmer profit margin and P/E assumptions.

Analyst Commentary

Recent commentary on Flow Traders points to growing caution around how the company is handling capital and defending its position in the market, with these concerns feeding directly into lower price targets and more conservative ratings.

Bearish Takeaways

- Bearish analysts highlight that the move to cut and suspend the dividend to grow capital has not yet delivered the intended benefits, which they view as a sign of weaker execution on capital management.

- There is concern that efforts to ease market share losses have not been effective so far, raising questions about the company’s ability to protect or improve its trading footprint over time.

- One firm reduced its price target to €24.90 from €28.77 and shifted to a more cautious rating, signalling that in their view the current valuation still does not fully reflect the risks around capital build and competition.

- Some analysts see limited justification to pay a higher multiple until there is clearer evidence that the capital retention policy and market share strategy are translating into more reliable earnings power.

What's in the News

- Flow Traders scheduled an Analyst/Investor Day, giving the market a dedicated forum to hear management’s latest views on the business and capital priorities. (Source: Key Developments)

- The company launched a digital assets OTC offering providing 24/7 proprietary, two-way liquidity for tokenized money-market funds, equities and commodities, including Franklin Templeton's BENJI and Tether Gold. (Source: Key Developments)

- The new digital assets OTC platform supports trading and hedging of tokenized equity and commodity exposures against fiat or stablecoins, using familiar OTC workflows, with access via FIX connectivity, OMS/EMS platforms, ECNs or high-touch execution. (Source: Key Developments)

- Flow Traders indicated that asset coverage in its digital assets offering will evolve over time, with availability differing by jurisdiction, regulatory status and counterparty eligibility within the group. (Source: Key Developments)

Valuation Changes

- Fair Value: trimmed slightly to €29.78 from €30.07, a small downward move that aligns with the more cautious stance on capital build and market share.

- Discount Rate: raised modestly to 10.58% from 10.43%, indicating a slightly higher required return in the updated assumptions.

- Revenue Growth: the revenue line is still assumed to decline, but the projected fall has eased slightly, to 14.74% from 14.84%.

- Net Profit Margin: increased to 38.69% from 37.23%, reflecting slightly firmer expectations for € earnings quality on each € of revenue.

- Future P/E: reduced to 9.00x from 9.66x, indicating that the stock is now being valued on a lower earnings multiple in the updated model.

Key Takeaways

- Volatility in digital asset investments and strategic partnerships may negatively affect future earnings and profitability if gains turn into unrealized losses.

- Rising fixed operating expenses and the need for capital investment may reduce net margins and impact competitiveness, dividends, and market positioning.

- Diversification, strategic partnerships, and capital expansion position Flow Traders for revenue growth and improved margins in emerging and digital asset markets.

Catalysts

About Flow Traders- Operates as a financial technology-enabled multi-asset class liquidity provider in Europe, the Americas, and Asia.

- Concerns about potential volatility and reversals in digital asset investments that have contributed to recent income might impact future earnings negatively if these gains turn into unrealized losses.

- Anticipated increase in fixed operating expenses, projected to be €190 million to €210 million in 2025, could compress net margins due to additional technology investments and hiring of subject matter experts.

- Ongoing need for additional trading capital to capture growth opportunities in emerging markets such as China may require continued retention of earnings or external financing, potentially impacting dividend distributions and return on equity.

- There is a risk of losing market share to better-capitalized competitors, necessitating significant capital investment to remain competitive in providing liquidity, which could affect revenue and market positioning.

- Unrealized gains from strategic investments in digital assets and partnerships may decrease if market dynamics shift, which could reduce other income and overall profitability.

Flow Traders Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Flow Traders's revenue will decrease by 14.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 18.0% today to 38.7% in 3 years time.

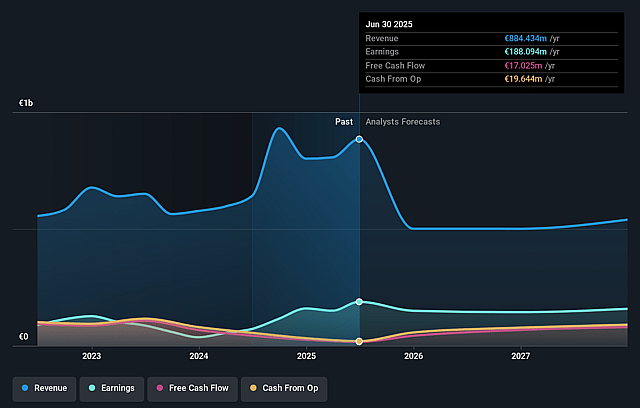

- Analysts expect earnings to reach €196.8 million (and earnings per share of €4.38) by about June 2029, up from €147.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 9.2x on those 2029 earnings, up from 7.3x today. This future PE is lower than the current PE for the GB Capital Markets industry at 10.2x.

- Analysts expect the number of shares outstanding to grow by 0.8% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.58%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Flow Traders achieved record fourth-quarter results and the second-best annual result in the company's history in 2024, with a strong increase in trading volume and profitability across various asset classes, suggesting continued revenue and earnings growth potential.

- The company's diversification strategy, including investments in digital assets and regional expansions, has positioned it to capture opportunities in emerging markets, potentially boosting revenue and net margins.

- Strategic partnerships and technological investments have enhanced Flow Traders' trading capabilities, which may lead to increased trading efficiency and improved net margins.

- The Trading Capital Expansion Plan and the increase in trading capital by 33% over the year have enhanced Flow Traders' ability to capture market opportunities, potentially raising revenues and returns on capital.

- Megatrends such as the growth in ETPs, digital assets, and electronic trading provide a favorable market environment for Flow Traders, which could support long-term revenue and profit growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €29.77 for Flow Traders based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €34.2, and the most bearish reporting a price target of just €24.9.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €508.7 million, earnings will come to €196.8 million, and it would be trading on a PE ratio of 9.2x, assuming you use a discount rate of 10.6%.

- Given the current share price of €24.72, the analyst price target of €29.77 is 17.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Flow Traders?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.