Last Update 22 Jun 26

FLOW: Future Returns Will Depend On Rebuilding Capital After Dividend Suspension

Analysts have lowered the Flow Traders price target to €24.90 from €28.77, citing a dividend suspension that, in their view, has not yet delivered the intended support for capital growth or market share.

Analyst Commentary

Recent research on Flow Traders focuses heavily on the dividend suspension and its impact on capital allocation, growth prospects, and valuation. The latest downgrade and price target cut to €24.90 highlight where analysts see execution gaps and where expectations around the company may need recalibrating.

Bearish Takeaways

- Bearish analysts argue that the dividend suspension, which was intended to support capital growth, has not yet translated into clearer benefits for shareholders. This has created questions around capital allocation discipline.

- Commentary points to limited evidence that the higher retained capital is easing market share pressure. This feeds into more cautious assumptions on Flow Traders' ability to defend or expand its trading footprint.

- The lower price target to €24.90 from €28.77 reflects a more restrained view on valuation, with bearish analysts assigning less credit for the dividend policy shift without clearer execution progress.

- The downgrade to a more cautious rating underscores concerns that the current business trajectory may not fully support prior expectations for growth or returns on the capital being retained.

What’s in the News for Flow Traders

- Flow Traders has scheduled an Analyst/Investor Day, giving the market a fresh chance to hear management’s current priorities on capital allocation, growth plans, and the impact of the dividend suspension. (Source: Key Developments)

- The upcoming Analyst/Investor Day is expected to focus on how Flow Traders is using retained earnings after suspending its dividend, a key topic for investors assessing whether the company’s balance sheet and capital position align with its trading ambitions. (Source: Key Developments)

- With analysts revisiting their assumptions on valuation and execution, the Flow Traders Analyst/Investor Day is positioned as an important touchpoint for updated guidance, risk discussion, and Q&A with management. (Source: Key Developments)

Valuation Changes for Flow Traders

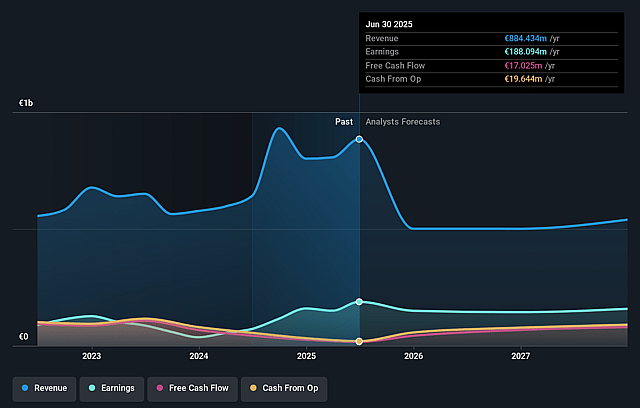

- Fair Value: Estimated fair value remains unchanged at €29.78 per share, indicating no model adjustment on this metric.

- Discount Rate: The discount rate is steady at 10.58%, with no revision to the required return used in the valuation model.

- Revenue Growth: Expected revenue growth is effectively unchanged at a decline of about 14.74%, reflecting the same outlook as before.

- Net Profit Margin: Projected net profit margin remains stable at about 38.69%, with only an immaterial rounding difference in the updated figure.

- Future P/E: The future P/E assumption stays at roughly 9.00x, with no material change in the multiple applied to Flow Traders earnings outlook.

Key Takeaways

- Volatility in digital asset investments and strategic partnerships may negatively affect future earnings and profitability if gains turn into unrealized losses.

- Rising fixed operating expenses and the need for capital investment may reduce net margins and impact competitiveness, dividends, and market positioning.

- Diversification, strategic partnerships, and capital expansion position Flow Traders for revenue growth and improved margins in emerging and digital asset markets.

Catalysts

About Flow Traders- Operates as a financial technology-enabled multi-asset class liquidity provider in Europe, the Americas, and Asia.

- Concerns about potential volatility and reversals in digital asset investments that have contributed to recent income might impact future earnings negatively if these gains turn into unrealized losses.

- Anticipated increase in fixed operating expenses, projected to be €190 million to €210 million in 2025, could compress net margins due to additional technology investments and hiring of subject matter experts.

- Ongoing need for additional trading capital to capture growth opportunities in emerging markets such as China may require continued retention of earnings or external financing, potentially impacting dividend distributions and return on equity.

- There is a risk of losing market share to better-capitalized competitors, necessitating significant capital investment to remain competitive in providing liquidity, which could affect revenue and market positioning.

- Unrealized gains from strategic investments in digital assets and partnerships may decrease if market dynamics shift, which could reduce other income and overall profitability.

Flow Traders Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Flow Traders's revenue will decrease by 14.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 18.0% today to 38.7% in 3 years time.

- Analysts expect earnings to reach €196.8 million (and earnings per share of €4.38) by about June 2029, up from €147.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 9.2x on those 2029 earnings, up from 7.6x today. This future PE is lower than the current PE for the GB Capital Markets industry at 11.1x.

- Analysts expect the number of shares outstanding to grow by 0.8% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.58%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Flow Traders achieved record fourth-quarter results and the second-best annual result in the company's history in 2024, with a strong increase in trading volume and profitability across various asset classes, suggesting continued revenue and earnings growth potential.

- The company's diversification strategy, including investments in digital assets and regional expansions, has positioned it to capture opportunities in emerging markets, potentially boosting revenue and net margins.

- Strategic partnerships and technological investments have enhanced Flow Traders' trading capabilities, which may lead to increased trading efficiency and improved net margins.

- The Trading Capital Expansion Plan and the increase in trading capital by 33% over the year have enhanced Flow Traders' ability to capture market opportunities, potentially raising revenues and returns on capital.

- Megatrends such as the growth in ETPs, digital assets, and electronic trading provide a favorable market environment for Flow Traders, which could support long-term revenue and profit growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €29.77 for Flow Traders based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €34.2, and the most bearish reporting a price target of just €24.9.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €508.7 million, earnings will come to €196.8 million, and it would be trading on a PE ratio of 9.2x, assuming you use a discount rate of 10.6%.

- Given the current share price of €25.82, the analyst price target of €29.77 is 13.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Flow Traders?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.