Last Update 17 Jun 26

UTL: Neutral Coverage And Stable Assumptions Will Shape Fairly Valued Stock

Analysts have kept their blended fair value estimate for Unitil steady at about $55.67 per share, with recent neutral initiations and a downgrade contributing to only minimal tweaks in underlying growth, margin, and P/E assumptions rather than a decisive shift in the stock’s overall outlook.

Analyst Commentary

Recent research on Unitil circles around a neutral stance, with analysts pointing to a mix of support factors and potential pressure points that help explain why the blended fair value estimate sits around $55.67 per share.

Bullish Takeaways

- Bullish analysts view the current fair value estimate near $55.67 as broadly aligned with Unitil’s execution profile. This suggests the stock price is reasonably anchored to underlying fundamentals.

- Neutral initiations signal that coverage is being built out without a strong negative bias. Some investors read this as a sign that Unitil’s risk profile is relatively balanced for a regulated utility.

- Only modest adjustments to growth and margin inputs in recent research imply that analysts see Unitil’s business model as relatively stable, with no major revisions required to support their valuation work.

- The absence of aggressive P/E changes across the latest reports points to a view that Unitil’s earnings power is neither overstated nor under serious question at current pricing.

Bearish Takeaways

- Bearish analysts highlight that neutral views and a recent downgrade cluster around the same fair value area. This can signal limited upside potential at or near the current estimate of $55.67 per share.

- Some caution reflects concern that, without clearer growth catalysts, Unitil’s valuation could remain capped by conservative assumptions for both margin expansion and earnings progression.

- Where P/E assumptions are tweaked, it tends to be in small, careful steps rather than in a way that suggests meaningful re-rating potential. This reinforces the idea of a fairly fully valued stock.

- The presence of a downgrade within recent coverage underlines the risk that any slip in execution or regulatory outcomes could lead analysts to revisit the fair value band and pull estimates lower.

What’s in the News for Unitil

- No recent news items are available for Unitil based on the provided sources.

Valuation Changes for Unitil Stock

- Fair Value: The blended fair value estimate for Unitil remains unchanged at $55.67 per share, with no shift in the underlying valuation output.

- Discount Rate: The discount rate stays effectively stable at 7.11%, indicating no material adjustment to the required return used in the model.

- Revenue Growth: The long term revenue growth input is essentially flat at about 2.05%, with only a minimal technical adjustment in the calculation.

- Net Profit Margin: The projected net profit margin assumption is steady at roughly 11.66%, reflecting no practical change in expected profitability.

- Future P/E: The future P/E multiple remains virtually unchanged at about 20.87x, suggesting no shift in how Unitil’s earnings are being valued within the model.

Key Takeaways

- Acquisition and sustainability initiatives are expected to drive future growth by boosting revenue, brand strength, and attracting ESG-conscious investors.

- Significant investments in infrastructure and modernization plan support earnings growth and improve operational efficiency, potentially enhancing customer satisfaction and margins.

- Increased operating expenses and substantial investments could compress margins and heighten financial risk, while regulatory challenges and competition may impact future revenue growth.

Catalysts

About Unitil- A public utility holding company, engages in the distribution of electricity and natural gas.

- The acquisition of Bangor Natural Gas is expected to drive future growth through increased customer base and operating synergies, potentially boosting future revenue and earnings.

- Advanced Metering Infrastructure (AMI) project, costing approximately $40 million, aims to enhance operational efficiency and could lead to improved net margins and customer satisfaction.

- The uncontested rate case settlement with FERC for Granite State Gas Transmission allows for a $3 million annual revenue increase, directly improving future revenue streams.

- The plan to achieve a 50% reduction in greenhouse gas emissions by 2030 through sustainability initiatives may attract ESG-conscious investors, potentially driving up the stock value and affecting earnings positively by enhancing brand strength and customer loyalty.

- Increased capital expenditure planning, with significant portions aimed at electric sector modernization, indicates future rate base growth between 6.5% to 8.5%, which is expected to support earnings growth of 5% to 7%.

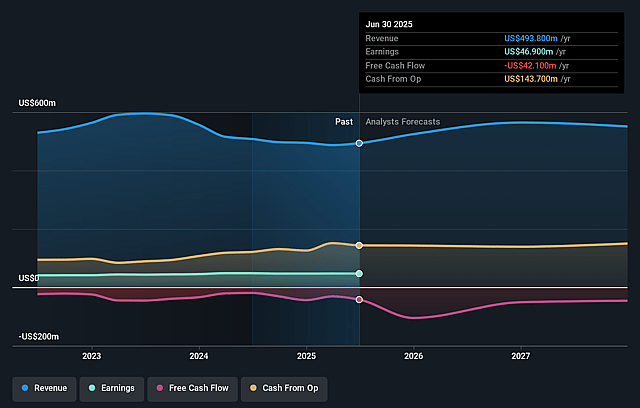

Unitil Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Unitil's revenue will grow by 2.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.6% today to 11.7% in 3 years time.

- Analysts expect earnings to reach $72.1 million (and earnings per share of $3.76) by about June 2029, up from $55.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 20.9x on those 2029 earnings, up from 16.7x today. This future PE is greater than the current PE for the US Integrated Utilities industry at 20.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company reported breakeven financial results for the third quarter, indicating limited profitability which could impact net margins and earnings.

- There is an increase in operating expenses, including labor and utility costs, which might compress margins despite revenue growth.

- Future investments, such as the $40 million AMI project, require substantial capital spending that may impact cash flow and increase financial risk.

- Regulatory proceedings and dependency on favorable outcomes, like for the Bangor Natural Gas acquisition, carry uncertainty that might affect revenue projections.

- Increasing competition between electric and gas investments in response to state policy shifts could alter expected revenue growth and affect rate base growth targets.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $55.67 for Unitil based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $618.6 million, earnings will come to $72.1 million, and it would be trading on a PE ratio of 20.9x, assuming you use a discount rate of 7.1%.

- Given the current share price of $51.47, the analyst price target of $55.67 is 7.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Unitil?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.