Last Update 20 Apr 26

BANR: Trimmed Price Views And Buybacks Will Shape Forward Return Profile

Analysts have trimmed their price targets on Banner by $4 to reflect slightly softer revenue growth expectations and a modestly adjusted outlook for forward P/E and margins.

Analyst Commentary

Recent research pieces highlight a mix of optimism and caution around Banner, with the $4 trim in price targets reflecting a more measured view of revenue growth, profitability and valuation.

Bullish Takeaways

- Bullish analysts still see the current P/E as reasonable relative to Banner's earnings profile, even after adjusting price targets to reflect softer revenue expectations.

- They point to Banner's ability to support margins as a key factor that, if maintained, could help justify the updated valuation ranges.

- Some see the more conservative revenue assumptions as creating room for upside if execution on growth initiatives keeps earnings close to prior expectations.

- The fact that price targets were trimmed rather than fully reset is viewed as a sign that long term earnings power is still intact in their models.

Bearish Takeaways

- Bearish analysts view the softer revenue outlook as a signal that Banner may need to work harder to support earnings growth, which they factor into lower target multiples.

- They are cautious that any pressure on margins, combined with slower top line trends, could leave less room for P/E expansion from current levels.

- Some see the $4 target reduction as a reflection of execution risk around Banner's growth plans, especially if revenue trends remain below earlier expectations.

- There is also concern that if growth stays muted for longer, valuation support could rely more heavily on cost control than on sustained revenue momentum.

What's in the News

- Banner reported fourth quarter 2025 net charge offs of $934,000, compared with $2,283,000 for the same quarter a year earlier (Key Developments).

- From October 1, 2025 to December 31, 2025, Banner repurchased 249,975 shares, representing 0.73% of shares, for $15.79 million (Key Developments).

- Banner has completed the repurchase of 499,975 shares in total, representing 1.45% of shares, for $31.5 million under the buyback announced on July 24, 2025 (Key Developments).

Valuation Changes

- Fair Value remained steady at $69.33, with no change in the modelled estimate.

- The Discount Rate was unchanged at 6.98%, indicating the same required return in the updated assumptions.

- Revenue Growth was trimmed slightly from 6.85% to 6.71%, reflecting a modestly softer topline outlook in the model.

- The Net Profit Margin was adjusted slightly higher from 28.61% to 28.66%, suggesting a small improvement in expected profitability.

- The Future P/E was nudged up from 12.02x to 12.04x, indicating a very small change in the valuation multiple applied to forward earnings.

Key Takeaways

- Strategic digitization and focus on relationship banking with growing markets support revenue expansion, improved efficiency, and operational leverage.

- Strong capital and liquidity enable continued growth through acquisitions, increasing market presence amid ongoing consolidation.

- Heavy exposure to CRE loans, funding imbalances, and rising expenses from digital investments create profitability risks, especially amid uncertain regional economic and policy conditions.

Catalysts

About Banner- Operates as the bank holding company for Banner Bank that engages in the provision of commercial banking and financial products and services to individuals, businesses, and public sector entities in the United States.

- Banner continues to benefit from strong population and business growth in the Pacific Northwest and West, particularly in secondary metropolitan areas, supporting long-term loan and deposit growth, which positions the company to drive higher revenues over time.

- The company's investments in new deposit and loan origination systems, as well as ongoing digitization efforts, are expected to reduce branch and back-office costs, while also expanding its reach to new customer segments, potentially improving net margins and efficiency ratios.

- Robust recent loan growth-driven by origination activity in owner-occupied commercial real estate, C&I, construction, and small business lending-indicates Banner is effectively capitalizing on economic and demographic shifts in its regions, supporting sustained top-line growth and earnings expansion.

- Banner's relationship banking focus, especially with small businesses and middle-market clients, is helping to drive both deposit and loan growth, which supports stable or improved net interest margins and greater operational leverage.

- Strong capital and liquidity positions, coupled with prudent funding strategies, provide Banner with flexibility to continue scaling through potential future acquisitions, further improving revenue and operating leverage as market consolidation persists.

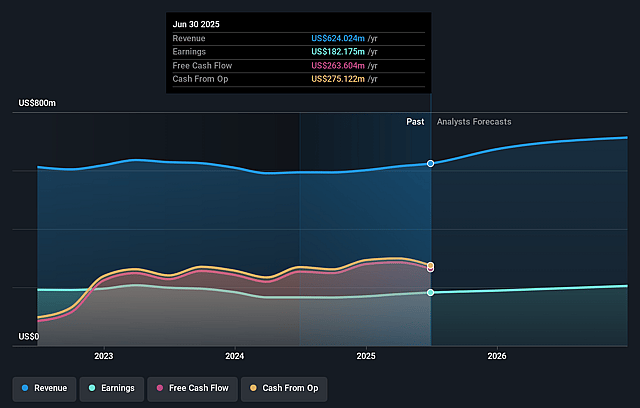

Banner Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Banner's revenue will grow by 6.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 30.2% today to 28.7% in 3 years time.

- Analysts expect earnings to reach $225.6 million (and earnings per share of $6.63) by about April 2029, up from $195.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 12.3x on those 2029 earnings, up from 11.2x today. This future PE is greater than the current PE for the US Banks industry at 11.9x.

- Analysts expect the number of shares outstanding to decline by 1.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.98%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Banner's loan growth is increasingly concentrated in commercial real estate (CRE) and construction lending, exposing the firm to heightened credit risk if regional economic conditions deteriorate, which could lead to elevated loan loss provisions and lower net income.

- Continued economic and policy uncertainty, particularly with the potential implementation of new tariffs and shifting trade negotiations, may negatively impact the West Coast economy-Banner's core market-and its small business clients, posing risks to loan growth, asset quality, and long-term revenue.

- The company continues to rely on core deposits for funding, but recent periods showed loan growth outpacing deposit growth, leading to a temporary reliance on higher-cost Federal Home Loan Bank (FHLB) advances; persistent funding imbalances or industry-wide deposit competition could reduce net interest margins and pressure earnings.

- Banner is in the process of ongoing digital investments and back office consolidations, which will elevate IT and nonrecurring expenses in the near-to-medium term; execution risk in these projects or delays in achieving efficiency gains could suppress net margins and profitability.

- Although Banner is focused on organic growth, the broader trend of regional bank consolidation and scale pressures could force it to pursue mergers or acquisitions; such moves may present integration risks, increased expenses, and potential shareholder dilution, adversely affecting long-term earnings and returns.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $69.33 for Banner based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $786.9 million, earnings will come to $225.6 million, and it would be trading on a PE ratio of 12.3x, assuming you use a discount rate of 7.0%.

- Given the current share price of $64.58, the analyst price target of $69.33 is 6.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Banner?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.