Last Update 14 Jun 26

Fair value Decreased 1.97%PNN: Repricing Will Reflect Cash Flow Visibility And Progressive Dividend Support

The analyst fair value estimate for Pennon Group has been nudged lower, tracking recent price target cuts of roughly £0.10 to £0.13 per share as analysts factor in tempered growth assumptions along with updated profitability and valuation inputs.

Analyst Commentary

Bullish Takeaways

- Bullish analysts continue to assign Buy ratings even as price targets are revised, which suggests they still see the current valuation as leaving room for upside if execution matches their expectations.

- Earlier target increases to £6.50 and a separate uplift of £0.50 highlighted prior confidence in Pennon Group's ability to support higher valuations when assumptions on returns and profitability were more supportive.

- Recent target levels in the £5.50 to £5.52 range still sit above the latest fair value revisions mentioned by the analyst community. This points to some remaining optimism on the stock's longer term positioning.

- For investors, the cluster of Buy ratings can be read as a signal that, despite recent adjustments, analysts see scope for Pennon Group to deliver on the growth and efficiency assumptions embedded in their models.

Bearish Takeaways

- Successive target cuts, from £6.56 to £5.52 and from £6.20 to £5.50, highlight growing caution around the assumptions underpinning Pennon Group's earnings power and growth profile.

- The shift from prior targets of around £6.50 down to the low £5 range points to analysts reassessing the risk and reward balance, with more conservative inputs on profitability and returns.

- Lowered targets imply that some of the earlier optimism around valuation multiples and medium term growth is being scaled back. This can cap near term rerating potential if sentiment remains cautious.

- For investors, the direction of these revisions is a reminder to stress test expectations on regulatory outcomes, capital spending and execution risks, as these are likely key drivers behind the more conservative target ranges.

What's in the News

- Pennon Group has recommended a final dividend of 20.03p per share for the year ended 31 March 2026, giving a total dividend of 29.29p per share when combined with the 9.26p interim dividend paid on 1 April 2026. Source: Key Developments.

- Shareholders are being offered a Dividend Reinvestment Plan (DRIP), allowing them to take the dividend in additional shares instead of cash. Source: Key Developments.

- The ordinary shares are quoted ex dividend on 23 July 2026, with a record date of 24 July 2026 and a final dividend payment date of 4 September 2026. Source: Key Developments.

- The company has delayed the release of its audited results for the year ended 31 March 2026 to 10 June 2026, from the previously scheduled 2 June 2026. Source: Key Developments.

Valuation Changes

- Fair value trimmed slightly to £6.02 from £6.14, reflecting a modest reduction of around 2% in the analyst fair value estimate.

- The discount rate is held steady at 7.38%, so the required return assumption on the stock is unchanged in the latest update.

- Revenue growth is reduced to 4.96% from 7.64%, a meaningful cut of roughly one third in projected top line expansion assumptions.

- The net profit margin is lowered to 9.05% from 10.61%, pointing to slightly more conservative expectations for future profitability.

- The future P/E is raised to 26.0x from 23.0x, indicating a higher valuation multiple being applied to projected earnings despite the softer growth and margin inputs.

Key Takeaways

- Strategic investments in infrastructure, digital technologies, and renewables are bolstering operational efficiency, margin resilience, and sustainability credentials.

- Acquisitions and population growth are driving stable revenue expansion, with enhanced long-term earnings and cash flow visibility.

- Rising infrastructure and compliance costs, operational and reputational risks, high leverage, and shifting market dynamics could constrain margins, earnings, and long-term shareholder returns.

Catalysts

About Pennon Group- Provides water and wastewater services in the United Kingdom.

- Pennon's accelerated capital investment in water network resilience, advanced treatment works, and leakage reduction positions the company to benefit from increased demand for water infrastructure upgrades, regulatory incentives, and long-term asset base growth, which should support a reliable upward trajectory in regulated revenues and future earnings.

- Ongoing adoption of digital technologies, including smart metering, network monitoring, and customer engagement platforms, is driving operational efficiencies and cost savings, which are expected to improve operating margins as these initiatives scale across their networks.

- Strategic acquisitions and integration (e.g., Bristol Water, Sutton & East Surrey) are unlocking synergies and operational efficiencies, with identified and progressing cost savings and EBITDA enhancement, setting up sustained medium

- to long-term earnings growth and margin expansion.

- Pennon's proactive investments in renewable energy generation for its operations reduce energy costs and exposure to volatility, supporting both margin resilience and progress towards net zero targets-enhancing long-term cost competitiveness and sustainability credentials that could attract regulatory and investment benefits.

- Population growth and urbanization, especially in the South West and newly acquired regions, are expected to drive stable or rising water demand and household/industrial consumption, bolstering Pennon's revenue base and providing long-term visibility on cash flows.

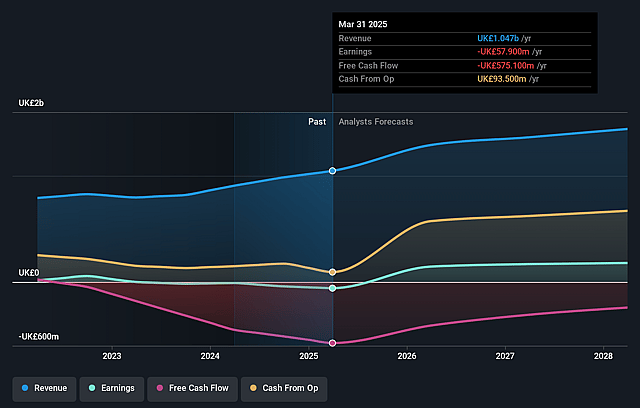

Pennon Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Pennon Group's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.1% today to 9.0% in 3 years time.

- Analysts expect earnings to reach £135.1 million (and earnings per share of £0.29) by about June 2029, up from £91.5 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 26.0x on those 2029 earnings, up from 24.6x today. This future PE is greater than the current PE for the GB Water Utilities industry at 23.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.38%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing and significant investment requirements to maintain, upgrade, and expand ageing infrastructure (especially to meet environmental and water quality standards) may suppress free cash flow and weigh on net margins and return on invested capital (ROIC) over the long term.

- Persistent challenges with environmental compliance-such as high-profile pollution incidents (e.g., Brixham water quality event) and recurring underperformance in Environment Agency (EA) assessment (EPA 2-star forecast for 2024)-could result in fines, heightened regulatory scrutiny, reputational damage, and tighter operational constraints, all negatively impacting earnings and revenue growth.

- Increasingly stringent environmental and water quality regulations, alongside the long-term drive to eradicate storm overflows and reduce pollution, are expected to drive up compliance costs and force additional investment, leading to margin pressure and potential limits on dividend growth.

- The company's relatively high gearing (61.8% at Water Group, 64.3% at Group level, even after the recent rights issue) leaves it exposed to higher interest payments, potential downgrades, and constrained financial flexibility-especially with rising debt costs and a large capital program ahead, which could reduce earnings available for shareholders.

- Long-term demographic shifts and water efficiency measures (actively encouraged by Pennon to support customer affordability) may dampen overall water demand and revenue growth, while any shift toward decentralised water solutions could slowly erode the customer base and recurring revenues.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £6.02 for Pennon Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £6.8, and the most bearish reporting a price target of just £5.2.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £1.5 billion, earnings will come to £135.1 million, and it would be trading on a PE ratio of 26.0x, assuming you use a discount rate of 7.4%.

- Given the current share price of £4.76, the analyst price target of £6.02 is 20.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Pennon Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.