Last Update 06 Dec 25

Fair value Increased 0.84%BOKF: Deposit Mix And Regional Lending Strength Will Support Balanced Future Returns

Analysts have nudged their price target on BOK Financial higher by about $1, to reflect expectations for a richer non-interest-bearing deposit mix, above-average loan growth in its Texas and Oklahoma footprint, and a strong capital position that can fund buybacks and organic expansion.

Analyst Commentary

Recent street research reflects a constructive shift in sentiment on BOK Financial, with price targets moving higher alongside improving expectations for growth and returns. Analysts are recalibrating their views based on a more favorable balance of loan momentum, deposit mix, and capital deployment potential.

Bullish Takeaways

- Bullish analysts point to the improving non interest bearing deposit mix as a key driver of higher net interest margins, which supports a valuation re rating as funding costs stabilize.

- Above average loan growth, particularly in the core commercial and energy related portfolios, is seen as a differentiator that can sustain revenue expansion relative to peers.

- Nearly half of the loan book being concentrated in the strong performing Texas and Oklahoma markets is viewed as a structural advantage for asset quality and long term growth visibility.

- The strong capital position, with capacity for buybacks alongside organic expansion, underpins expectations for improved return on equity and supports a higher target multiple.

Bearish Takeaways

- Bearish analysts caution that expectations for sustained above trend loan growth could prove optimistic if regional economic conditions in Texas and Oklahoma normalize or soften.

- There is concern that reliance on improving non interest bearing deposit mix may leave earnings sensitive to renewed competition for deposits if rates remain higher for longer.

- Some remain wary that capital deployment into buybacks, while supportive for near term EPS, could limit flexibility if credit costs or regulatory requirements rise.

- Valuation risk is highlighted, as the recent move in the price target assumes successful execution on growth and deposit initiatives with limited room for missteps.

What's in the News

- BOK Financial Corporation raised its quarterly dividend to USD 0.63 per share, payable November 26, 2025, with an ex dividend and record date of November 12, 2025 (Key Developments).

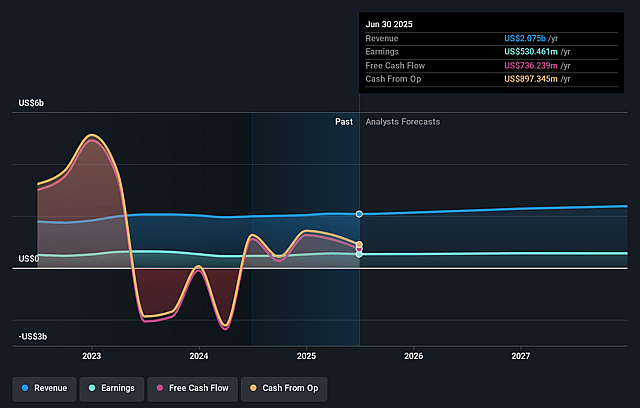

- The company issued 2025 earnings guidance, targeting net interest income of USD 1.325 billion to USD 1.35 billion and projecting mid single digit total revenue growth versus the prior year (Key Developments).

- Between July 29, 2025 and September 30, 2025, BOK Financial repurchased 365,547 shares, or 0.57 percent of shares outstanding, for USD 40.58 million, completing the buyback announced July 30, 2025 (Key Developments).

- Under a separate authorization announced November 2, 2022, the company has completed repurchases totaling 4,130,318 shares, or 6.29 percent of shares outstanding, for USD 360.17 million as of July 29, 2025 (Key Developments).

- For the third quarter ended September 30, 2025, BOK Financial reported net charge offs of USD 3.627 million (Key Developments).

Valuation Changes

- The fair value estimate has risen slightly to about $119.70 from $118.70, implying a modestly higher intrinsic valuation.

- The discount rate has edged down marginally to roughly 7.24 percent from 7.26 percent, reflecting a slightly lower required return.

- Revenue growth assumptions are essentially unchanged at about 6.07 percent, indicating a stable medium-term growth outlook.

- The net profit margin remains effectively flat at approximately 23.80 percent, signaling no material shift in long-run profitability expectations.

- The future P/E multiple has increased modestly to about 14.79x from 14.68x, suggesting a slightly richer valuation framework for forward earnings.

Key Takeaways

- Strategic expansion into growth regions and enhanced digital banking drive operational efficiencies, increased loan activity, and resilient earnings diversification.

- Robust wealth management fueled by demographic trends and strong fee income streams supports sustained, stable growth amid shifting economic conditions.

- Concentrated loan risk, regional dependence, margin pressure, rising costs, and competitive threats could hinder growth, earnings, and profitability for BOK Financial over time.

Catalysts

About BOK Financial- Operates as the financial holding company for BOKF, NA that provides various financial products and services in Oklahoma, Texas, New Mexico, Northwest Arkansas, Colorado, Arizona, and Kansas/Missouri.

- Sustained population and economic growth in the Sun Belt and Midwest regions are driving strong demand for lending, commercial real estate, and wealth management-reflected in accelerating loan growth in core C&I, CRE, and new mortgage finance initiatives-supporting ongoing revenue expansion.

- Broader adoption of digital banking, combined with BOK Financial's continued investments in technology and customer experience, is expected to yield long-term operational efficiencies, reduce operating costs, and enhance net margins.

- Rising intergenerational wealth transfers and an increased focus on retirement planning are fueling robust growth in the wealth management and fiduciary business, as seen in record asset management revenue and consistent high-single-digit growth rates, strengthening diversified fee-based income streams.

- BOK Financial's strategic expansion into fast-growing markets like Texas and Arizona, alongside talent acquisition in key markets, positions the company to capitalize on secular migration and economic trends, propelling above-peer loan and revenue growth.

- The company's diversified fee income-including trading, wealth management, and treasury services-provides resilience against interest rate fluctuations and contributes to a more stable and growing earnings base.

BOK Financial Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming BOK Financial's revenue will grow by 5.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 25.6% today to 23.5% in 3 years time.

- Analysts expect earnings to reach $579.1 million (and earnings per share of $9.36) by about September 2028, up from $530.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.3x on those 2028 earnings, up from 13.3x today. This future PE is greater than the current PE for the US Banks industry at 11.9x.

- Analysts expect the number of shares outstanding to decline by 0.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.27%, as per the Simply Wall St company report.

BOK Financial Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Overconcentration in the commercial real estate (CRE) and energy loan portfolios presents elevated credit risk, especially as recent growth in CRE could expose BOK Financial to sector-specific downturns; this may result in higher-than-expected loan losses, negatively impacting net income and earnings over the long term.

- BOK Financial remains heavily dependent on the economic health of the Midwest and Southwest regions, so any localized economic downturns or demographic stagnation could disproportionately hamper deposit and loan growth, limiting revenue expansion and overall earnings potential.

- The company acknowledged ongoing "hypercompetitive" market conditions in its core regions, which may continue to drive spread and margin compression in C&I lending, limiting net interest margin and net interest income growth in the coming years.

- Rising technology and operational costs, such as those related to the build-out of the new mortgage finance business and ongoing digital investments, could pressure expense growth relative to revenue if scale benefits fail to materialize, weakening net margins and return on equity.

- Heightened regulatory focus and increasing compliance/technology demands, alongside the persistent threat from fintech and non-bank competitors, may raise structural costs and make it more difficult to attract younger, digitally native customers-potentially resulting in lower deposit growth, reduced fee income, and long-term margin dilution.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $116.1 for BOK Financial based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.5 billion, earnings will come to $579.1 million, and it would be trading on a PE ratio of 15.3x, assuming you use a discount rate of 7.3%.

- Given the current share price of $110.58, the analyst price target of $116.1 is 4.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on BOK Financial?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.