Last Update 26 Jun 26

Fair value Increased 24%ENVI: Upcoming UK And Poland DRS Deployments Will Support Stronger Outlook

Analysts have raised their price target on Envipco Holding to €8.05 from €6.50, reflecting updated assumptions for revenue growth, profit margins and future P/E levels in their valuation work.

What's in the News

- Envipco Holding signed the final Reverse Vending Machine (RVM) supply contract with Iceland Foods in the UK, covering approximately 1,500 Compact RVMs with service included, with deliveries planned from spring 2027 through the UK Deposit Return Scheme (DRS) launch in October 2027. Source: Envipco press release reference in client announcement.

- Envipco Holding entered an agreement to supply around 700 RVMs to Netto Polska, including service over the contract duration, with deliveries already underway and full deployment expected in 2026. Source: client announcement.

- The Netto Polska agreement is tied to Poland’s DRS, which went live in October 2025 and is targeting coverage of around 14b beverage containers annually and a 90% collection rate by 2029, with Envipco Holding supporting the system through its Warsaw office and regional sales teams. Source: client announcement.

- Envipco Holding has been appointed exclusive RVM supplier to one UK retailer, with plans to deliver approximately 2,300 Compact, Flex and Optima RVMs under a contract that includes service, with deliveries expected to start in the first half of 2027. Source: client announcement.

Valuation Changes for Envipco Holding

- Fair Value: raised from €6.50 to €8.05 per share. This represents a sizeable upward revision in the underlying valuation for Envipco Holding.

- Discount Rate: adjusted slightly lower from 6.95% to 6.92%, reflecting updated assumptions in the risk profile used in the model.

- Revenue Growth: revised from 55.46% to 58.48%, indicating higher projected top line expansion in the updated Envipco Holding forecasts.

- Net Profit Margin: updated from 14.80% to 15.24%, pointing to modestly higher expected earnings efficiency on each € of revenue.

- Future P/E: moved from 12.66x to 14.56x, signalling a higher valuation multiple applied to Envipco Holding’s projected earnings.

Key Takeaways

- Regulatory momentum and growing ESG focus are fueling new demand for Envipco's recycling solutions, expanding its revenue pipeline and service opportunities.

- Strategic investments in capacity, innovation, and recurring services strengthen Envipco's market position and support margin improvement as existing installations mature.

- Ongoing regulatory delays, rising costs, weak operational cash flow, and overreliance on major launches jeopardize Envipco's growth, profitability, and financial stability.

Catalysts

About Envipco Holding- Develops, manufactures, assembles, leases, sells, markets, and services a line of reverse vending machines (RVMs) in the Netherlands, the United States, North America, and Europe.

- Pending regulatory implementation of new deposit return schemes (DRS) in key European markets such as Poland and Portugal, along with mandates like the EU Packaging Waste Regulation (requiring 90% recovery by 2029), are set to drive a significant, multi-year increase in reverse vending machine demand-creating a substantial pipeline of revenue growth as these markets move from pilot to full-scale rollout.

- Rising consumer and corporate focus on sustainability and ESG compliance is prompting major retailers and governments to accelerate the adoption of advanced recycling solutions, directly increasing the addressable market for Envipco's RVMs and supporting both higher unit sales and recurring services revenue in new and existing markets.

- Continued investment in localized production, expanded business development teams, and scalable manufacturing capacity positions Envipco to quickly fulfill large orders as they materialize, supporting top-line acceleration and potential operating margin improvement due to efficiency gains and supply chain flexibility.

- Envipco's expansion of high-margin recurring program services, digital platforms, and long-term service contracts-embedded early in customer relationships-provides a growing earnings base, which will gradually lift net profit margins as installed RVM bases mature beyond initial warranty periods.

- Ongoing innovation in high-speed, AI-integrated RVMs and partnerships for brownfield market entries (e.g., Quantum platform adoption in new regions) will differentiate Envipco's offering, enabling price premiums and market share gains, expected to support both revenue growth and long-term expansion of EBITDA margins.

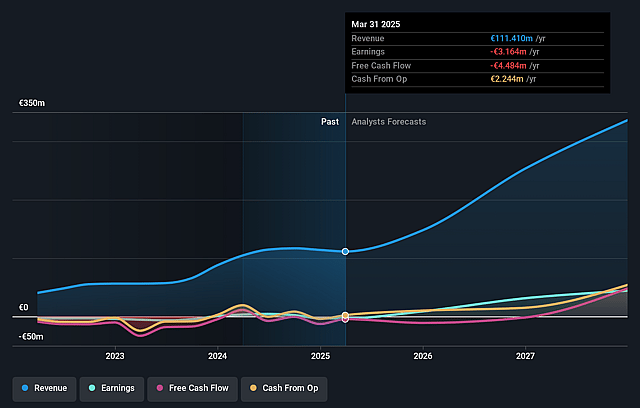

Envipco Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Envipco Holding's revenue will grow by 58.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -14.8% today to 15.2% in 3 years time.

- Analysts expect earnings to reach €54.1 million (and earnings per share of €0.92) by about June 2029, up from -€13.2 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €78.0 million in earnings, and the most bearish expecting €43.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.7x on those 2029 earnings, up from -18.6x today. This future PE is lower than the current PE for the NL Machinery industry at 28.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.92%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Delays and uncertainty in the rollout of new deposit return schemes in key growth markets like Poland and Portugal are pushing customer purchasing decisions into late 2025 and possibly 2026, risking a protracted period of soft revenues and volatility in the company's projected topline growth.

- Heavy ongoing investments in headcount, business development, and R&D (with operating expenses up 17% year-on-year) are currently not matched by revenue growth, pressuring EBITDA and resulting in net losses, which, if prolonged, could erode net margins and threaten profitability.

- Despite stable gross margins, negative cash flow from operations (EUR -4.6 million in Q2) driven by working capital build (higher inventories and receivables) and a reliance on increased borrowings to maintain liquidity (total borrowings up €4.3 million sequentially) may strain the company's financial stability and increase balance sheet risk if soft market conditions persist.

- The decline in North American sales and limited underlying volume growth indicate that the region remains only moderately growing, exposing Envipco to regional demand fluctuations and limiting the company's global revenue diversification.

- Revenue remains heavily dependent on major market launches spurred by regulation, so any changes, delays, or uncertainties in policy implementation, deposit scheme specifications, or interoperability requirements could significantly impact Envipco's sales momentum and earnings visibility in the medium to long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €8.05 for Envipco Holding based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €9.6, and the most bearish reporting a price target of just €6.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €354.6 million, earnings will come to €54.1 million, and it would be trading on a PE ratio of 14.7x, assuming you use a discount rate of 6.9%.

- Given the current share price of €3.71, the analyst price target of €8.05 is 54.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Envipco Holding?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.