Last Update 02 Jun 26

Fair value Decreased 3.04%TEGA: Upcoming Board Decisions And CFO Transition Will Support Future Upside

Analysts have revised their fair value estimate for Tega Industries to ₹2,020.25 from ₹2,083.67, reflecting updated assumptions around the discount rate, revenue growth, profit margin, and a higher future P/E multiple.

What's in the News

- A board meeting is scheduled for May 29, 2026, to consider and approve audited standalone and consolidated financial results for the quarter and financial year ended March 31, 2026, and to consider recommending a dividend on equity shares, if any. (Source: Company filing)

- A board meeting is set for May 18, 2026, at 12:10 Indian Standard Time to review a proposal for executing a facility agreement for a borrowing facility with Standard Chartered Bank and other lenders, along with other matters. (Source: Company filing)

- A board meeting will be held on April 24, 2026, to consider the resignation of Chief Financial Officer Mr. Sharad Kumar Khaitan and the proposed appointment of Mr. Shyama Prasad Ganguly, General Manager, Finance & Accounts, as Interim CFO and Key Managerial Personnel. (Source: Company filing)

- A special or extraordinary shareholders meeting via postal ballot in India is scheduled for April 18, 2026, to consider and approve the reappointment of Mr. Jagdishwar Prasad Sinha as an Independent Director of the company. (Source: Company filing)

Valuation Changes

- Fair Value: Revised to ₹2,020.25 from ₹2,083.67, indicating a modest reduction in the estimated value per share.

- Discount Rate: Adjusted slightly higher to 14.73% from 14.66%, which generally makes future cash flows less valuable in the model.

- Revenue Growth: Assumed revenue growth is now 17.18% compared with 18.50% earlier, pointing to a more conservative growth outlook in the model.

- Net Profit Margin: Margin assumption has been reduced to 11.66% from 16.07%, a significant cut to expected profitability levels.

- Future P/E: The assumed future P/E multiple has moved up to 84.36x from 63.52x, implying a higher valuation multiple applied to expected earnings.

Key Takeaways

- Expanding global footprint and product innovation in sustainability-oriented consumables position Tega to benefit from rising mining activity and evolving ESG requirements.

- Recurring aftermarket demand and strong operational efficiencies enhance earnings resilience, supporting stable margins and improved long-term revenue visibility.

- Global uncertainties, volatile input costs, tough competition, and stricter regulations threaten margins, cash flow stability, and growth prospects for Tega Industries.

Catalysts

About Tega Industries- Designs, manufactures, and installs process equipment and accessories for the mineral processing, mining, and material handling industries.

- The rising demand for copper and gold, driven by global electrification, EVs, infrastructure expansion, and the energy transition, is leading to increased mining activity and related capital expenditure, directly fueling Tega's order book and underpinning multi-year revenue growth.

- Tega's ongoing investments in capacity expansion and global footprint-especially the on-track Chile plant and ramp-up in Latin America and Africa-are set to unlock access to high-growth mining regions, supporting sustained export revenue growth and improved earnings visibility.

- The surge in environmental and ESG compliance requirements is pushing mining customers to favor innovative, wear-resistant, and sustainability-focused consumables, areas where Tega's product development and operational strategy are strongly aligned, potentially supporting premium pricing and margin expansion.

- Recurring aftermarket demand for consumable products, notably for high-growth platforms like DynaPrime, provides a stable, annuity-like revenue stream, enhancing earnings resilience and predictability even through cyclical industry downturns.

- Operational efficiencies, strong gross margins despite raw material volatility, and the ability to flexibly pass on supply chain and freight costs to customers support ongoing EBITDA margin stability and potential expansion as volumes increase over the next several quarters.

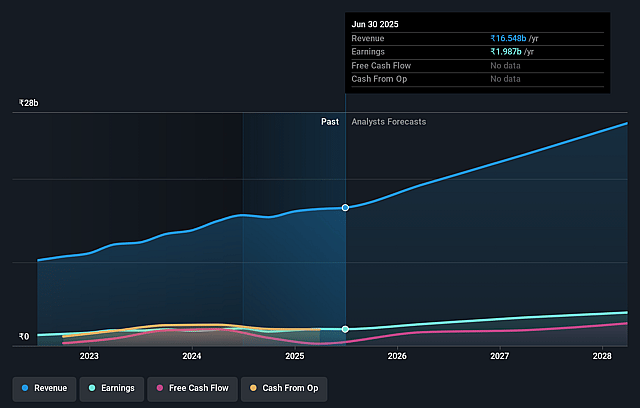

Tega Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Tega Industries's revenue will grow by 17.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.0% today to 11.7% in 3 years time.

- Analysts expect earnings to reach ₹3.3 billion (and earnings per share of ₹44.3) by about June 2029, up from ₹1.4 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 84.4x on those 2029 earnings, down from 95.4x today. This future PE is greater than the current PE for the IN Machinery industry at 25.9x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.73%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Prolonged or worsening global macroeconomic and political uncertainties (such as wars, logistics bottlenecks, supply chain disruptions, and sanctions) could disrupt Tega's ability to serve international markets, which contribute approximately 90% of the company's revenues, directly impacting top-line growth and earnings visibility.

- Rising raw material price volatility (especially for rubber, steel, etc.) amid global supply chain pressures could squeeze gross margins and compress net profitability if Tega cannot pass on costs fully or faces delays in doing so, leading to potential margin erosion over time.

- Declining year-on-year revenues and margins in the key consumables business, combined with customer-driven order deferments and uncertainties in shipping schedules, introduce risks of uneven cash flows and reduced predictability of quarterly earnings.

- Intensifying competition from established global OEMs such as FLSmidth (actively expanding and lowering costs via contract manufacturing and acquisitions) and ongoing presence of Chinese players increase pricing pressure and pose risks to Tega's ability to retain or grow its market share, potentially reducing pricing power and impacting revenues and margins in the long term.

- Heightened ESG and regulatory pressures, particularly in developed markets (e.g., new US tariffs, tougher environmental regulations), could increase compliance costs and create barriers to entry, leading to higher operational expenses and limiting expansion opportunities, negatively affecting both future revenues and bottom-line performance.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹2020.25 for Tega Industries based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹28.5 billion, earnings will come to ₹3.3 billion, and it would be trading on a PE ratio of 84.4x, assuming you use a discount rate of 14.7%.

- Given the current share price of ₹1811.4, the analyst price target of ₹2020.25 is 10.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Tega Industries?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.