Last Update 17 Jun 26

Fair value Increased 4.97%HLMA: Post Selloff Repricing Will Likely Support Future Share Price

Halma's analyst price target has been revised higher to £43.76 from £41.69, with analysts pointing to valuation support after the recent selloff and the removal of what they describe as a "photonics premium" on the shares.

Analyst Commentary

Recent research on Halma highlights a split between analysts who see the recent share price pullback as an opportunity and those who remain more neutral, focusing on execution and valuation risk. The latest price targets cluster in the £45.00 to £46.00 range, which investors may view as a reference point when assessing Halma shares after the selloff.

Bullish Takeaways

- Bullish analysts point to valuation support, arguing that the recent selloff has reset expectations and removed what they describe as a prior photonics premium in Halma stock.

- The revised £43.76 average price target, alongside specific targets around 4,500 GBp to 4,600 GBp, is framed as more closely aligned with Halma's fundamentals following the de-rating.

- Upgrades in stance from more neutral views are being justified by the view that current pricing better reflects execution risks, which some see as improving the risk or reward balance.

- The clustering of higher targets is interpreted by bullish analysts as a sign that the stock's valuation is no longer stretched relative to its perceived quality and growth profile.

Bearish Takeaways

- Bearish analysts, or those staying neutral, are keeping more cautious ratings even as they lift price targets, indicating ongoing concern about paying too much for Halma's execution track record.

- The decision to maintain an Equal Weight stance alongside a higher 4,500 GBp target suggests some see limited upside from current levels once execution and valuation risks are factored in.

- There is an implicit caution that, even after the removal of the photonics premium, Halma could still trade at a level where further rerating depends on consistent delivery against expectations.

- Some analysts appear to view the recent target increases as adjustments to reflect market pricing rather than a clear signal that Halma shares are mispriced on a long term basis.

What’s in the News for Halma

- Halma's board has recommended a final dividend of 15.11 pence per share for the financial year ended 31 March 2026, compared with 14.12 pence per share for the prior year, according to the company’s key developments disclosure.

- The total dividend per share proposed for the year is 24.74 pence, compared with 23.12 pence per share in the previous year. The company stated this 7.0% change is in line with its medium term organic revenue growth rate. Source: Halma key developments.

- The proposed final dividend remains subject to shareholder approval at Halma's Annual General Meeting on 23 July 2026. Any approved payment is scheduled for 14 August 2026 to shareholders on the register at 10 July 2026. Source: Halma key developments.

Valuation Changes for Halma

- Fair Value has been revised from £41.69 to £43.76, indicating a modest uplift in the central valuation estimate for Halma shares.

- The Discount Rate has been adjusted from 9.42% to 9.49%, which generally implies a marginally higher required return in the updated assumptions.

- Revenue Growth has moved from 11.21% to 9.95%, suggesting more cautious expectations for Halma's future top line expansion within the model.

- The Net Profit Margin has been updated from 15.38% to 15.09%, reflecting a small reduction in assumed profitability levels.

- The Future P/E has shifted from 40.37x to 41.81x, indicating a higher earnings multiple embedded in the revised valuation framework.

Key Takeaways

- Strong cash generation and balance sheet support significant R&D and acquisition investments, ensuring sustainable growth and increased future revenues and earnings.

- Focus on niche markets and talent investment boosts high margins and long-term growth potential, enhancing future profit margins and earnings.

- Geopolitical instability, currency impact, and reliance on M&A and niche markets may challenge Halma's revenue, profit margins, and financial flexibility.

Catalysts

About Halma- Together its subsidiaries, provides technology solutions in the safety, health, and environmental markets in the United States, Mainland Europe, the United Kingdom, the Asia Pacific, Africa, the Middle East, and internationally.

- Continued strong cash generation and a healthy balance sheet have enabled substantial investments in R&D and acquisitions, ensuring sustainable future growth, which is likely to drive up revenues and earnings.

- Acquisitions and a robust M&A pipeline spanning all sectors are contributing to EBIT growth and are expected to enhance future profit margins and earnings growth.

- Organic revenue growth supported by price increases and strong demand ensures maintained high gross margins and potentially improved earnings.

- Investment in talent and collaborative culture across a diverse portfolio positions Halma for consistent growth, enhancing long-term earnings potential.

- Focus on high-value niche markets with strong, long-term growth drivers supports high margins and returns on invested capital, suggesting an increase in future net margins and earnings.

Halma Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

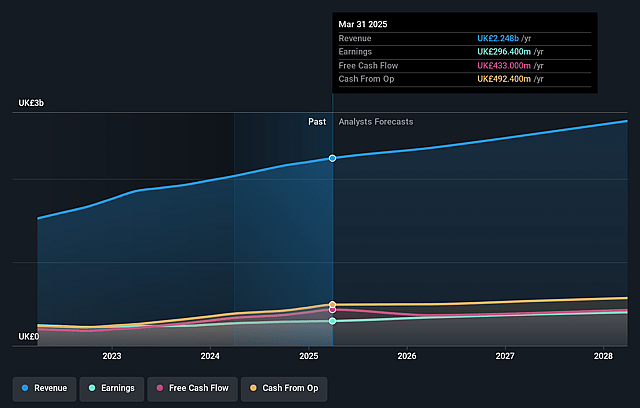

- Analysts are assuming Halma's revenue will grow by 10.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.4% today to 15.1% in 3 years time.

- Analysts expect earnings to reach £518.0 million (and earnings per share of £1.38) by about June 2029, up from £372.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 41.9x on those 2029 earnings, up from 39.3x today. This future PE is greater than the current PE for the GB Electronic industry at 18.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.49%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The ongoing geopolitical and economic volatility, along with an adverse currency movement impacting revenue growth, presents a risk that could limit Halma's financial performance. This currency drag, specifically the strengthening of sterling, has been noted as a headwind (revenue impact).

- The decline in the Healthcare sector, notably in eye health therapeutics due to delays in OEM product launches and destocking, offsets growth in other areas and could strain profit margins if not rectified promptly (net margin and revenue impact).

- The strategy of continuous M&A could present risks, especially if integration challenges arise or if acquired companies underperform. Recently acquired businesses, despite contributing to growth, sometimes require additional investment, affecting short-term profitability (earnings impact).

- The reliance on high-margin niche markets and regulated industries means any shifts in regulatory policies or changes in market conditions could impact revenue streams and the overall margin performance, particularly if robustness in sustainability diminishes (net margins and revenue impact).

- While current cash generation and dividend growth are strong, any shift in interest rates or economic conditions affecting cash conversion rates could challenge Halma's financial flexibility and ability to sustain high reinvestment and acquisition activities (cash flow and earnings impact).

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £43.76 for Halma based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £50.1, and the most bearish reporting a price target of just £30.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £3.4 billion, earnings will come to £518.0 million, and it would be trading on a PE ratio of 41.9x, assuming you use a discount rate of 9.5%.

- Given the current share price of £38.74, the analyst price target of £43.76 is 11.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Halma?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.