Catalysts

About Mycronic

Mycronic supplies production equipment and solutions for electronics manufacturing, including pattern generators, PCB assembly systems and related technologies.

What are the underlying business or industry changes driving this perspective?

- Reliance on a concentrated Pattern Generators customer base in photomasks and displays, combined with a quarter of no new system orders and an 84% decline in division order intake to SEK 191 million, points to a risk that even a stable end market could translate into lower system refresh cycles. This could weigh on future equipment revenue and EBIT contribution from what is currently the main profit engine.

- Expanding exposure to consumer electronics and AI or data center driven PCB test demand increases sensitivity to product cycles and investment pauses. Any slowdown in handset launches, data center build outs or Chinese domestic demand could leave the high backlog of SEK 2.3 billion in Pattern Generators and SEK 915 million in High Volume at risk of slower conversion into sales and weaker net margins.

- The acquisition heavy growth path, with three companies bought in the quarter and more than SEK 900 million in investing cash outflows, is already creating earnings drag in Global Technologies through SEK 23 million of negative EBIT impact. If integration or scaling of Surfx, RoBAT and Cowin is slower than planned, group EBIT margin near 27% on the latest quarter could be pressured by rising R&D and G&A without matching revenue.

- Industry moves toward more advanced OLED and AMOLED displays, larger masks and more complex panel architectures require continual R&D increases. With R&D costs already up by SEK 60 million year on year and guided to stay at a high level, any delay in commercial uptake of new tools or plasma based surface treatment solutions could compress operating leverage and earnings despite healthy technology road maps.

- While aftermarket net sales of SEK 465 million and a growing base of installed systems provide some recurring revenue, aftermarket as a share of sales is now 24% and trending slightly lower. If new system orders in Pattern Generators or PCB Assembly Solutions remain uneven, the current mix may not be enough to cushion group revenue or cash flow, especially given higher inventories and working capital swings.

Assumptions

This narrative explores a more pessimistic perspective on Mycronic compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Mycronic's revenue will grow by 3.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 21.9% today to 24.9% in 3 years time.

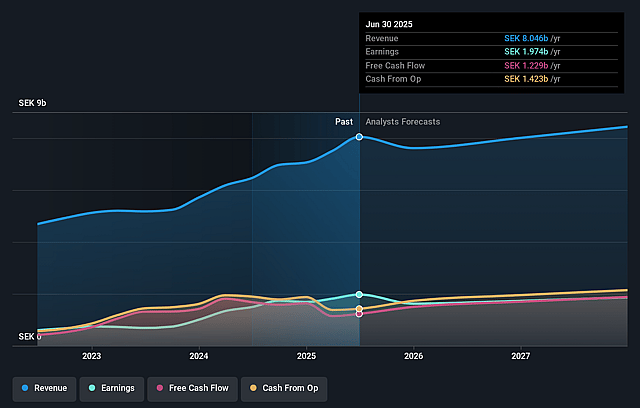

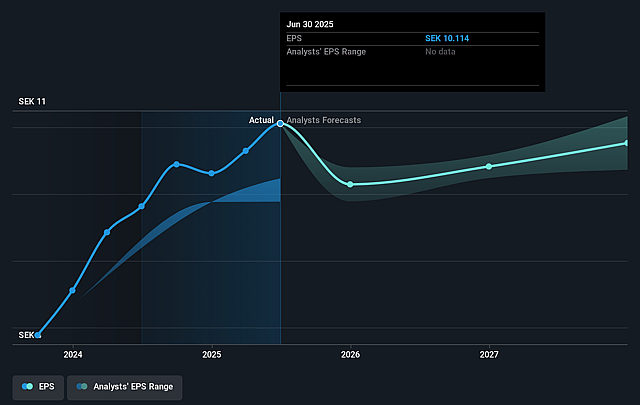

- The bearish analysts expect earnings to reach SEK 2.2 billion (and earnings per share of SEK 9.07) by about January 2029, up from SEK 1.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 17.1x on those 2029 earnings, down from 25.6x today. This future PE is lower than the current PE for the GB Electronic industry at 27.5x.

- The bearish analysts expect the number of shares outstanding to decline by 0.29% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.39%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The Pattern Generators division currently carries a strong backlog of SEK 2.3b with 19 systems, alongside what management describes as stable photomask markets and normal customer discussions. This could help sustain revenue and EBIT even if near-term order timing is uneven, supporting earnings rather than a prolonged decline in profitability.

- High Volume systems are seeing healthy demand from Chinese domestic customers and other regions, with order intake of SEK 383 million, net sales of SEK 443 million and a backlog of SEK 915 million. Any continuation of this trend in consumer electronics and data center related demand could underpin group revenue and EBIT more than a bearish view implies.

- Global Technologies achieved a 95% increase in order intake to SEK 402 million and almost 60% sales growth to SEK 323 million, helped by strong PCB test demand linked to AI and data centers. If this end market continues to require more complex testing capacity, it could support higher long-term revenue and margin resilience.

- Aftermarket net sales of SEK 465 million and a growing installed base across Pattern Generators and other divisions provide recurring contractual revenue. If this service and upgrade stream continues to expand, it may help smooth cash flows and support EBIT margins even during softer capital equipment cycles.

- The company is investing heavily for future growth, with R&D costs up SEK 60 million year on year and three acquisitions in the quarter, including Surfx with atmospheric plasma technology and Cowin in mask and panel repair. If these technologies and capabilities gain broader adoption in semiconductors and advanced displays, they could support revenue growth and possibly higher group margins over the longer term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Mycronic is SEK161.0, which represents up to two standard deviations below the consensus price target of SEK218.67. This valuation is based on what can be assumed as the expectations of Mycronic's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK255.0, and the most bearish reporting a price target of just SEK161.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be SEK8.8 billion, earnings will come to SEK2.2 billion, and it would be trading on a PE ratio of 17.1x, assuming you use a discount rate of 6.4%.

- Given the current share price of SEK228.6, the analyst price target of SEK161.0 is 42.0% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Mycronic?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.