Last Update 17 Jun 26

INDGN: Tax Resolution Progress And Final Dividend Plans Will Support Upside

Indegene's analyst price target has been reaffirmed around ₹592, with analysts pointing to relatively unchanged assumptions on fair value, revenue growth, profit margin and future P/E, along with a slightly higher discount rate as the key drivers behind the updated view.

What’s in the News for Indegene

- Indegene received a final assessment order from the Income Tax Department for Assessment Year 2023-24, including an income tax demand of ₹436.88441 million with transfer pricing adjustments of ₹1,234.110559 million cited in the order.

- The company has applied for resolution through the Mutual Agreement Procedure under the Double Taxation Avoidance Agreement between India and the United States, and is also pursuing remedies under the domestic appellate framework in parallel.

- Indegene has stated that, based on its assessment of the tax matter, it does not currently expect any material adverse impact on its financial position or operations, and will update stock exchanges on further developments as required.

- The board has scheduled a meeting on April 29, 2026, to review audited standalone and consolidated financial results for the quarter and year ended March 31, 2026, to consider a final dividend recommendation, and to review ESOP and RSU allotments.

- At the upcoming Annual General Meeting, Indegene plans to propose a final dividend of ₹2.25 per equity share with a face value of ₹2 for the financial year ending March 31, 2026. If approved by shareholders, the dividend is to be paid within 30 days of approval, with the record date and AGM date to be announced.

Valuation Changes for Indegene

- Fair Value: Fair value remains unchanged at ₹592.43 per share, indicating no revision to the central valuation estimate for Indegene.

- Discount Rate: The discount rate has risen slightly from 13.48% to 13.73%, reflecting a modestly higher required return being applied in the valuation model.

- Revenue Growth: The revenue growth assumption is effectively stable at about 16.36%, with only a marginal numerical adjustment.

- Net Profit Margin: The net profit margin assumption remains steady at about 13.53%, with no meaningful change in the profitability outlook used for Indegene.

- Future P/E: The future P/E multiple has edged up from 27.88x to 28.06x, representing a small increase in the valuation multiple applied to Indegene's projected earnings.

Key Takeaways

- AI-driven digital solutions and deeper multi-year client relationships are expanding Indegene's market presence, improving revenue growth and operational efficiencies in pharma services.

- Strategic reinvestment and targeted acquisitions are shifting revenues toward higher-margin, technology-led offerings and expanding capabilities across new verticals and geographies.

- Revenue and margin growth face challenges from client concentration risk, industry conservatism, regulatory-driven volatility, wage inflation, and sector-wide drug pricing pressures.

Catalysts

About Indegene- Operates as a digital-first life sciences commercialization company in India, the United States, Europe, and internationally.

- Indegene is seeing strong client interest in large-scale digital transformation and AI adoption within the pharma industry, supported by the need to improve cost efficiency and speed to market in response to ongoing drug pricing pressures; this is expected to expand Indegene's addressable market, drive higher revenue growth, and enable deeper, multi-year client relationships.

- The company's Tectonic offering, which moves Indegene further up the value chain in commercial content creation by leveraging AI and end-to-end digital solutions, is already generating revenue and is positioned to unlock 2-4x more of clients' marketing budgets, pointing to material revenue acceleration and higher net margins over time as this scales.

- Deepening integration and multi-year engagements with top global pharma clients-alongside a strengthening and broadening sales pipeline-are enhancing long-term revenue visibility and higher operating leverage, which should support improved margin expansion as Indegene's platform-based solutions gain scale.

- Continued, strategic reinvestment into AI-enabled platforms (such as Cortex) and expansion of high-value service offerings are expected to drive differentiation versus competitors and shift more of Indegene's revenues toward higher-margin, technology-led services, with the medium

- to long-term impact being a structural uplift in net margins and earnings.

- Management's active M&A pipeline, fueled by strong cash generation, aims to further accelerate top-line growth by acquiring complementary capabilities in digital health and medical communications both in the US and Europe, enabling cross-sell opportunities and expansion into new service verticals and geographies-supportive of sustained revenue and potential EPS growth.

Indegene Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

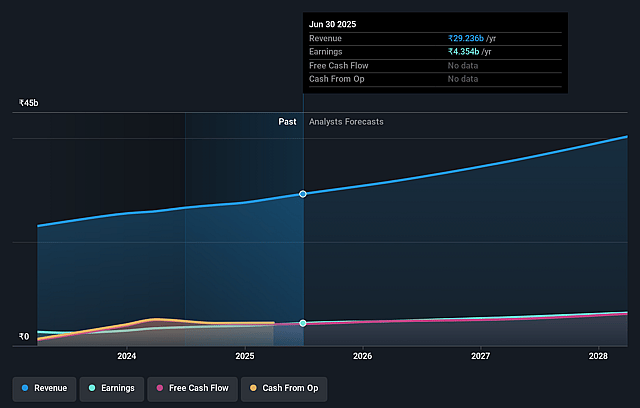

- Analysts are assuming Indegene's revenue will grow by 16.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.4% today to 13.5% in 3 years time.

- Analysts expect earnings to reach ₹7.5 billion (and earnings per share of ₹30.25) by about June 2029, up from ₹4.0 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹8.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 28.1x on those 2029 earnings, down from 30.9x today. This future PE is lower than the current PE for the IN Life Sciences industry at 39.5x.

- Analysts expect the number of shares outstanding to grow by 0.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.73%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company is experiencing significant quarterly variability in its Brand Activation (Omnichannel Activation) segment, with material project deferrals and conclusion of sizable projects due to client regulatory hurdles, potentially leading to revenue volatility and compressed margins if this persists.

- Wage inflation and annual compensation resets, especially with a notable portion of staff outside India, are expected to continue putting pressure on margins; ongoing reinvestment in AI and transformation initiatives may offset productivity benefits, limiting net margin expansion in the medium term.

- High client concentration risk remains, with 76% of revenues coming from the top 20 clients; though efforts to broaden the client base are ongoing, loss or slowdown in a single large account (as experienced in the previous year) could materially impact revenues and earnings.

- Despite strong positioning around AI offerings, client adoption continues to be slow due to the conservative nature of the pharma industry and significant risk perceptions, which could delay the realization of differentiated revenue streams and limit margin upside from new platforms.

- The pharma industry's persistent pressure on drug pricing and potential reduction in US federal drug spending via Medicaid-even if currently non-material-signals secular headwinds that may drive long-term pricing pressures on Indegene's core services, potentially impacting future revenue growth and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹592.43 for Indegene based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹705.0, and the most bearish reporting a price target of just ₹480.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹55.3 billion, earnings will come to ₹7.5 billion, and it would be trading on a PE ratio of 28.1x, assuming you use a discount rate of 13.7%.

- Given the current share price of ₹515.6, the analyst price target of ₹592.43 is 13.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Indegene?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.