Last Update 23 Jun 26

CAT: Women’s Football Partnership Will Drive Future Performance Analytics Upside

Analysts have kept their A$5.57 price target for Catapult Sports steady, citing only minor tweaks to discount rate, revenue growth, profit margin and future P/E assumptions that largely offset one another.

What’s in the News for Catapult Sports

- Mercury13, a multi club ownership group focused on women's football, has entered a multi year partnership with Catapult Sports as its exclusive Official Elite Sports Performance Analytics and GPS Partner, and non exclusive Official Thought Leadership Partner. Source: Company client announcement.

- The agreement covers all Mercury13 clubs and extends Catapult Sports' existing work with Bristol City Women to FC Badalona Women First Teams and Academies, and FC Como Women Academy, forming a central element of Mercury13's performance approach. Source: Company client announcement.

- Catapult Sports will provide a fully integrated performance system, including wearable devices, analytics platforms, centralised data management and on site practitioner support across the Mercury13 club network. Source: Company client announcement.

- The partnership is designed to support a female led, women specific performance model that combines athlete monitoring, sports science research and coach education, with a focus on female athlete health, training load and long term player welfare in elite women's football. Source: Company client announcement.

Valuation Changes

- Fair Value: A$5.57 remains unchanged, indicating no revision to the central valuation estimate for Catapult Sports.

- Discount Rate: Discount Rate has fallen slightly from 8.41% to 8.39%, a small adjustment to the assumed risk profile.

- Revenue Growth: Revenue Growth has eased modestly from 16.40% to 15.82%, reflecting a slightly lower growth assumption for future sales.

- Net Profit Margin: Net Profit Margin has risen marginally from 3.35% to 3.35%, indicating a very small change in expected earnings efficiency.

- Future P/E: Future P/E has risen slightly from 250.79x to 251.63x, implying a marginally higher multiple applied to projected earnings.

Key Takeaways

- Strong revenue growth driven by cross-selling, innovative product introductions, and entry into new verticals and markets.

- High customer retention and operating leverage highlight stable revenue stream and significant growth potential in emerging women's sports market.

- Heavy reliance on new products and key sports markets faces execution risks and potential revenue fluctuations amidst competitive, geopolitical, and regulatory challenges.

Catalysts

About Catapult Group International- A sports science and analytics company, provides sporting teams and athletes with technologies designed to optimize athlete performance, avoid injury, and improve return to play in Australia, Europe, the Middle East, Africa, the Asia Pacific, and the Americas.

- Catapult's annualized contract value (ACV) rose by 20% year-over-year, driven by cross-selling and expansion into new verticals, indicating strong future revenue growth and increased customer engagement.

- The introduction of innovative products such as the Sideline Video analysis for American Football and new algorithms for various sports is expected to enhance the product suite and drive revenue growth by attracting new customers and expanding the existing base.

- High customer retention rates (96.2%) and strong growth in average ACV per Pro Team (11% year-over-year) suggest a stable revenue stream and potential for further margin expansion through ongoing cross-selling efforts.

- The company's operating leverage has resulted in a 75% year-over-year incremental profit margin, highlighting efficiencies that are expected to enhance net margins as the business scales.

- Expansion into the growing women's sports market and potential adoption of new technologies by major leagues (e.g., NFL) represent significant growth opportunities that could positively impact revenue and contribute to sustained earnings growth.

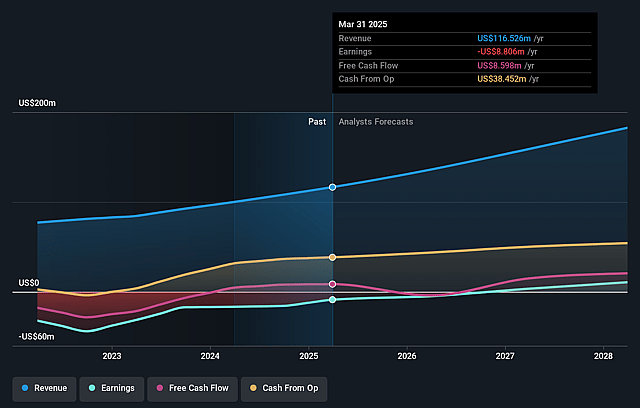

Catapult Group International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Catapult Sports's revenue will grow by 15.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from -17.0% today to 3.3% in 3 years time.

- Analysts expect earnings to reach $7.3 million (and earnings per share of $0.03) by about June 2029, up from -$24.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $22.6 million in earnings, and the most bearish expecting $-961.9 thousand.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 252.2x on those 2029 earnings, up from -24.6x today. This future PE is greater than the current PE for the AU Software industry at 24.1x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.39%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Catapult's growth strategy relies heavily on the success of its new products and cross-selling, especially the Sideline Video product in American Football, which could face competitive threats or changes in NCAA rules impacting revenue and ACV growth.

- The company's decision to cease operations in the Russian market, though only impacting less than 1% of future revenue, highlights risks related to geopolitical issues that could affect earnings in other regions.

- The reliance on a few key sports markets, such as American Football and soccer, may expose Catapult to revenue fluctuations due to changes in those industries, like shifts in league investments or regulations.

- There is a dependence on maintaining high ACV retention and successful multi-vertical growth, which carries execution risks; any decline in customer satisfaction or increased churn could impact recurring revenues and profitability.

- Despite impressive growth and cash flow improvements, the company's need to strengthen its balance sheet and reduce remaining debt underscores potential financial instability risks, affecting net margins in the event of unexpected expenses or revenue shortfalls.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$5.57 for Catapult Sports based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$8.0, and the most bearish reporting a price target of just A$3.97.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $218.6 million, earnings will come to $7.3 million, and it would be trading on a PE ratio of 252.2x, assuming you use a discount rate of 8.4%.

- Given the current share price of A$2.77, the analyst price target of A$5.57 is 50.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Catapult Sports?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.