Last Update 06 Jun 26

Fair value Decreased 6.39%BUR: Future Upside Will Rely On YPF Windfall And Litigation Outcomes

Analysts have trimmed their average price target on Burford Capital by £0.44 to reflect updated assumptions for fair value, discount rates and future profitability, while still highlighting differing views on upside potential after recent target moves and rating changes across the Street.

Analyst Commentary

Recent research shows a mixed but engaged analyst backdrop around Burford Capital, with several firms adjusting targets and ratings in quick succession. Taken together, these moves highlight both confidence in aspects of the story and caution around execution, profitability and how to value the portfolio.

Bullish Takeaways

- Bullish analysts who have raised price targets see room for upside relative to current trading levels, suggesting they view the recent assumptions on fair value as still supportive of a higher equity value.

- Comments that downside is limited from current levels point to a view that, even after target cuts, the risk or reward profile remains attractive enough to justify keeping exposure.

- Maintaining positive ratings alongside trimmed targets indicates that some analysts are recalibrating models on profitability and discount rates without abandoning their constructive stance on the business model.

- The willingness to adjust targets both up and down over a short period signals that analysts are actively refining their valuation work as new information on performance and case outcomes becomes available.

Bearish Takeaways

- Multiple downward target revisions highlight concern that earlier fair value and earnings assumptions may have been too optimistic, with analysts now baking in more conservative profitability expectations.

- Recent downgrades signal that some bearish analysts are less comfortable with the balance between potential upside and the execution risk tied to Burford Capital's case pipeline and capital deployment.

- Lower targets from previously higher levels suggest that, for more cautious analysts, the margin of safety has narrowed, especially if cash realization or case resolutions fall short of prior forecasts.

- The cluster of downgrades and target cuts within a compressed timeframe underscores that not all analysts are aligned on how to price the inherent uncertainty in litigation outcomes and the associated discount rates.

What's in the News

- No recent news stories, periodical coverage or key developments were provided for Burford Capital, so current market discussion is being driven mainly by analyst target and rating changes rather than specific new events. (Sources: Recent News Stories, Periodicals, Key Developments)

- The absence of flagged company specific news means investors may want to focus on existing disclosures, previous case updates and financial reports when assessing the stock. (Sources: Recent News Stories, Periodicals, Key Developments)

- With no new items listed, recent analyst model tweaks appear to reflect updated views on valuation inputs rather than reactions to fresh company announcements. (Sources: Recent News Stories, Periodicals, Key Developments)

Valuation Changes

- Fair value was trimmed from £6.88 to £6.44, reflecting a modest reduction in the implied equity valuation per share.

- The discount rate was adjusted slightly lower from 7.24% to 7.05%, indicating a small change in the required return used in analyst models.

- Revenue growth was reset from 27.03% to 888.97%, marking a major shift in top line growth assumptions in the updated model.

- The profit margin was reduced from 29.40% to 16.06%, pointing to a lower expected share of revenue converting into earnings.

- The future P/E moved higher from 10.86x to 14.86x, suggesting that analysts are now applying a richer earnings multiple to the forecast period.

Key Takeaways

- Burford Capital's impressive portfolio recovery and case conclusions support future revenue and cash flow growth, enhancing net margins and earnings potential.

- Transitioning to U.S. filing standards aims to improve transparency, attract investors, and positively influence stock valuation and earnings per share.

- Burford Capital's reliance on fair value accounting and high-stakes legal outcomes creates financial volatility, with regulatory and interest rate risks impacting operations and market sentiment.

Catalysts

About Burford Capital- Provides legal finance products and services worldwide.

- Burford Capital has seen an impressive recovery in its portfolio performance, resulting in record levels of net realized gains for 2024, which could support future revenue and cash flow growth as more cases are concluded successfully.

- The company is experiencing significant growth in its litigation finance portfolio, having achieved a compound annual growth rate of about 15% over the last few years. This growth, combined with higher target realizations, is expected to drive future revenue and earnings.

- Burford Capital's expanding focus on originating high-quality new business, including corporate monetizations and diverse case types, should enhance its future net margins and earnings potential, even as individual investment strategies evolve.

- The firm's effective cash management and realization of significant amounts of cash from concluded cases underscore operational efficiencies, potentially providing better net margins and positively impacting future earnings.

- Burford's ongoing transition to U.S. domestic filing standards and enhanced disclosure aims to provide greater transparency and attract investor interest, potentially influencing stock valuation and market perception, thereby supporting higher earnings per share in the future.

Burford Capital Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

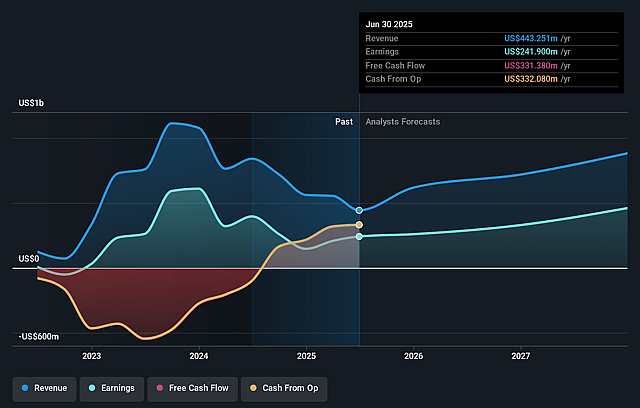

- Burford Capital currently has no revenue. Analysts are forecasting revenue to reach $967.3 million by June 2029.

- As a pre-revenue company, Analysts expect Burford Capital to achieve a profit margin of 16.1% in 3 years time.

- Analysts expect earnings to reach $155.4 million (and earnings per share of $0.47) by about June 2029, up from -$1.6 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.9x on those 2029 earnings, up from -0.6x today. This future PE is greater than the current PE for the GB Diversified Financial industry at 14.0x.

- Analysts expect the number of shares outstanding to grow by 0.12% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.05%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The reliance on fair value accounting and unrealized gains remains a concern for some investors, as any negative unrealized loss figures can trigger adverse market reactions, impacting overall investor sentiment and potentially affecting share price. (Earnings)

- The business model’s dependence on high realization of legal cases can lead to volatile revenue streams, and any downturn in legal case success rates or longer case durations could negatively affect financial performance. (Revenue, Earnings)

- Significant returns are tied to large, high-stakes cases like YPF. Delays or unfavorable outcomes in such cases could adversely impact Burford's financial outcomes. (Net Margins, Earnings)

- The firm's cash-oriented focus combined with exposure to variable interest rates could pose financial risks during periods of interest rate volatility, potentially affecting valuation metrics used in their assets. (Net Margins, Earnings)

- New U.S. regulatory changes, although considered unlikely, could impact the firm’s ability to operate freely, potentially affecting future revenue and market expansion. (Revenue, Net Margins)

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £6.44 for Burford Capital based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £16.72, and the most bearish reporting a price target of just £3.71.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $967.3 million, earnings will come to $155.4 million, and it would be trading on a PE ratio of 14.9x, assuming you use a discount rate of 7.1%.

- Given the current share price of £3.31, the analyst price target of £6.44 is 48.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Burford Capital?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.