Key Takeaways

- Strong housing demand and infrastructure investment are expected to drive revenue growth, margin improvements, and increased plant utilization across core divisions.

- Acquisitions, geographic expansion, and sustainability initiatives are set to enhance revenue diversity, synergy realization, and long-term competitive positioning.

- Aggressive acquisitions, reliance on public infrastructure pipelines, regional market weakness, capital-intensive property exposure, and rising compliance costs collectively threaten margins, growth prospects, and liquidity.

Catalysts

About MAAS Group Holdings- Together with subsidiaries, engages in the provision of construction materials to the civil infrastructure, renewable energy, building and construction, and mining sectors.

- Demand for construction materials and residential land development is positioned to benefit from Australia's strong population growth, pent-up housing demand, low rental vacancy rates, and expectations of interest rate cuts-catalysts that should drive higher revenues and margin improvements, especially in the second half of FY '26 as residential construction activity rebounds.

- Increasing federal and state government investment in infrastructure and renewable energy projects is supporting a robust project pipeline for MAAS's Construction Materials and Civil Construction & Hire divisions, pointing to longer-term top-line growth and higher plant utilization, which can lift EBITDA and return on capital.

- Recent acquisitions and geographic expansion into new regions (e.g., Illawarra, Greater Melbourne) are set to contribute fully in FY '26, broadening the revenue base, enabling MAAS to realize synergy benefits, and supporting both revenue growth and net margin expansion as integration progresses.

- Company investments in modern, strategically located asset bases (including quarries and equipment) and asset recycling initiatives have enhanced liquidity and balance sheet strength, improving earnings stability and enabling ongoing investment in growth opportunities, which can underpin higher future net earnings and lower leverage.

- Heightened focus on sustainability, integration of environmental initiatives, and early adoption of reporting standards can position MAAS to meet emerging regulatory and customer expectations, opening up new project opportunities and supporting premium pricing/margin protection, thus benefitting long-term margins and competitive positioning.

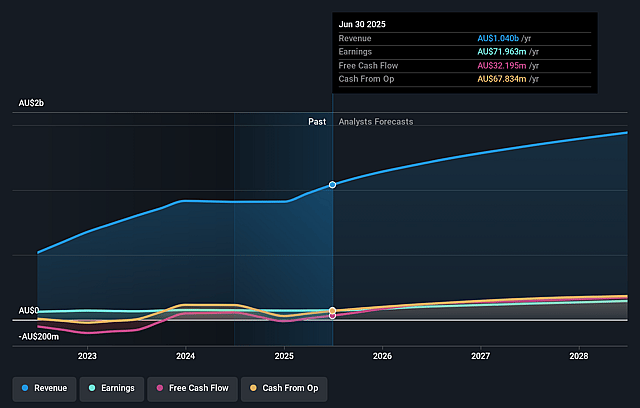

MAAS Group Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MAAS Group Holdings's revenue will grow by 11.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.9% today to 10.0% in 3 years time.

- Analysts expect earnings to reach A$144.4 million (and earnings per share of A$0.41) by about September 2028, up from A$72.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.4x on those 2028 earnings, down from 22.2x today. This future PE is lower than the current PE for the AU Construction industry at 18.7x.

- Analysts expect the number of shares outstanding to grow by 1.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.83%, as per the Simply Wall St company report.

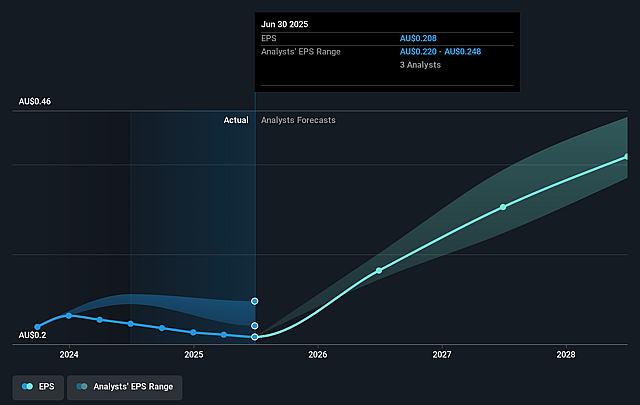

MAAS Group Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The group's aggressive acquisition strategy, while enabling rapid growth in Construction Materials, has increased operating expenses and leverage; the short-term drag on margins and lower return on capital employed (down from 13% to 11%) raises risks related to overextension, potential integration challenges, and higher financing costs, all of which could pressure net margins and earnings if acquisition synergies do not materialize as expected.

- The performance and growth outlook remain heavily reliant on government and infrastructure project pipelines-delays in renewable energy and transmission projects have already depressed Civil Construction and Hire (CCH) EBITDA by 35% year-on-year; continued project deferrals, regulatory bottlenecks, or changes in government spending priorities could reduce or postpone revenue and profitability, particularly in CCH.

- Regional market softness, especially in key areas like Melbourne where concrete demand is weak, has negatively impacted volumes and is only expected to recover in the latter half of FY '26; extended regional market weakness, or a slower-than-expected recovery in residential and commercial construction, could further suppress revenue and margin expansion in core business segments.

- The company's asset-backed growth strategy locks significant capital into residential and commercial property developments; if demographic shifts (slowing population growth, housing demand volatility, or rising interest rates) reduce settlement rates or pricing power, this could expose MAAS to liquidity risks and impair future revenue and earnings from property sales.

- Increased compliance requirements and expectations around sustainability, coupled with higher costs for decarbonisation initiatives and the need for more transparent environmental reporting, may elevate operating expenses and limit MAAS's eligibility for certain public and private sector projects, thus compressing net margins over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$4.903 for MAAS Group Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$5.45, and the most bearish reporting a price target of just A$3.8.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$1.4 billion, earnings will come to A$144.4 million, and it would be trading on a PE ratio of 16.4x, assuming you use a discount rate of 8.8%.

- Given the current share price of A$4.42, the analyst price target of A$4.9 is 9.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.