Last Update 28 Mar 26

Fair value Decreased 0.66%ANN: Sustainable Chemical Protection And Capital Returns Will Support Future Upside Potential

Analysts have nudged their fair value estimate for Ansell slightly lower, trimming the price target from about A$36.47 to A$36.23 as they refresh assumptions around discount rates, long term revenue growth, profit margins and the future P/E multiple.

What's in the News

- Announced an interim dividend of US$0.266 per share for the six months ended December 31, 2025, with an ex date of February 23, 2026, record date of February 24, 2026, and payment date of March 13, 2026 (Key Developments).

- Completed a share buyback program covering 1,372,236 shares, about 0.95% of shares, for A$47.2 million between August 25, 2025 and February 16, 2026 (Key Developments).

- Launched TouchNTuff 93-800, a disposable glove designed to provide at least 15 minutes of acetone resistance, described as fifteen times longer than standard nitrile disposable gloves, targeting workers in sectors such as aerospace, automotive, chemical manufacturing and maintenance (Key Developments).

- Positioned TouchNTuff 93-800 with EN ISO 374-1 Type A chemical resistance and EN388 2110A abrasion and cut resistance, along with high visibility orange coloring intended to improve foreign object detection in controlled or high precision environments (Key Developments).

- Highlighted that TouchNTuff 93-800 contains more than 60% bio-based carbon and is TUV certified, described as a more sustainable chemical protection option without compromising performance in the product description (Key Developments).

Valuation Changes

- Fair Value: Trimmed slightly from A$36.47 to A$36.23, reflecting a modest reset in the valuation anchor.

- Discount Rate: Adjusted marginally higher from 8.06% to 8.06%, a very small shift in the required return used in the model.

- Revenue Growth: Held effectively steady at about 4.18%, indicating no material change to long term top line assumptions.

- Net Profit Margin: Kept broadly unchanged at about 10.89%, suggesting stable expectations for underlying profitability.

- Future P/E: Reduced from 17.73x to 17.25x, implying a slightly lower valuation multiple applied to future earnings.

Key Takeaways

- Strong demand in PPE, new product innovation, and global expansion support sustained revenue and earnings growth for Ansell.

- Automation, efficiency improvements, and sustainability initiatives are expected to drive margin expansion and higher long-term cash flow.

- Shifting regulatory, competitive, and sustainability dynamics threaten Ansell's profitability and sales growth due to rising costs, changing customer preferences, and margin pressures.

Catalysts

About Ansell- Designs, sources, develops, manufactures, distributes, and sells hand and body protection solutions in the Asia Pacific, Europe, the Middle East, Africa, Latin America, the Caribbean, and North America.

- Accelerating demand for healthcare PPE and medical products, fueled by the aging global population and rising regulatory safety standards-combined with Ansell's new product launches and innovation (such as antimicrobial gloves and sustainable materials)-should support robust multi-year revenue growth and an improving gross margin profile.

- Heightened workplace safety awareness and infectious disease concerns, post-COVID, continue to drive durable, higher-value PPE usage, supporting both volume and pricing power for Ansell's specialized offerings and thus expected to boost long-term earnings growth.

- Ongoing automation, ERP rollout, and productivity investments (APIP), along with the successful KBU integration, are expected to drive further cost reductions, manufacturing efficiency, and operational leverage-translating into EBIT margin expansion and stronger free cash flow.

- Ansell's diversified geographic and vertical market presence-in combination with growth in emerging market healthcare infrastructure (e.g., India, China, Brazil)-strategically positions the company to capture international expansion opportunities and underpin resilient, above-market revenue growth.

- Increased customer focus on supply chain security and sustainability, compounded by Ansell's leadership in recycling programs (e.g., RightCycle) and low-carbon/eco-friendly products, is likely to enhance customer loyalty and unlock higher-margin sales channels, positively impacting net margins and return on capital over the long run.

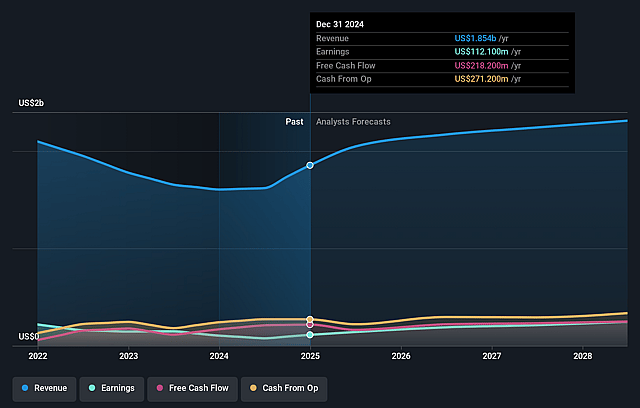

Ansell Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Ansell's revenue will grow by 4.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.7% today to 10.9% in 3 years time.

- Analysts expect earnings to reach $247.6 million (and earnings per share of $1.76) by about March 2029, up from $135.4 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $289.5 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.3x on those 2029 earnings, down from 20.5x today. This future PE is lower than the current PE for the AU Medical Equipment industry at 25.4x.

- Analysts expect the number of shares outstanding to decline by 1.56% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.06%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Rising global focus on sustainability and environmental regulations could increase the regulatory burden and costs associated with Ansell's reliance on single-use plastics and synthetic materials in its PPE products, risking margin pressure and potential revenue declines if product portfolios are perceived as less eco-friendly.

- Ongoing margin pressure from higher raw material costs (such as latex and nitrile) combined with limited ability to pass those costs to customers-especially in more commoditized product segments-could weigh on net margins and earnings growth, particularly if tariffs and inflation persist or intensify.

- Growing competition from lower-cost Asian manufacturers as well as potential industry commoditization may erode Ansell's market share and price realization, resulting in slower revenue growth and downward pressure on profitability over the long term.

- The emergence of advanced reusable or biodegradable alternatives in PPE, alongside evolving customer sustainability preferences and regulatory changes, may reduce demand for Ansell's core disposable glove products and negatively affect long-term sales growth.

- Ongoing industry consolidation, including increased purchasing power among healthcare group purchasing organizations and major distributors, could further compress prices and contract terms, impacting Ansell's ability to maintain revenue growth and healthy net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$36.23 for Ansell based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$40.97, and the most bearish reporting a price target of just A$34.37.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.3 billion, earnings will come to $247.6 million, and it would be trading on a PE ratio of 17.3x, assuming you use a discount rate of 8.1%.

- Given the current share price of A$28.67, the analyst price target of A$36.23 is 20.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Ansell?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.