Last Update 22 Jun 26

Fair value Decreased 11%AHRT: Share Repurchases And Leasing Progress Will Support Future Margin Stability

The analyst price target for AH Realty Trust has shifted to $7.00 from $7.88 as analysts factor in a lower fair value estimate, along with adjustments to the discount rate, revenue growth, profit margin expectations, and future P/E assumptions informed by recent sector-wide REIT valuation updates.

Analyst Commentary

Recent research on AH Realty Trust reflects a mixed but generally balanced view, with price targets and ratings signaling both optimism about execution and caution around valuation for a smaller REIT in a sector seeing broad recalibrations.

Bullish Takeaways

- Bullish analysts have lifted their price target on AH Realty Trust to US$7, signaling that their updated models still see support for the current fair value estimate despite sector-wide REIT adjustments.

- The higher target from bullish analysts suggests they see AH Realty Trust as able to execute against its current plan, even as they apply more conservative assumptions across the broader REIT sector.

- Positive stance on seniors housing and certain REIT subsectors in recent research supports the view that specialized exposure can still justify a full valuation, which may inform how some investors look at AH Realty Trust.

- Across healthcare-focused REIT coverage, bullish analysts continue to highlight opportunities tied to portfolio quality and balance sheet management, which remains a key focus area for AH Realty Trust investors as well.

Bearish Takeaways

- Bearish analysts maintain an Underperform rating on AH Realty Trust alongside a US$7 target, indicating concern that current pricing may already reflect most of the value they see in the shares.

- One price target cut of roughly US$1 for AH Realty Trust suggests more cautious assumptions around revenue growth, margins, and P/E multiples given updated REIT sector valuation work.

- Recent commentary highlighting REIT valuations as less attractive after a strong start to the year points to a tougher backdrop for multiple expansion, which can limit upside for AH Realty Trust even if execution remains on track.

- The shift of certain REIT subsectors to more neutral views underscores a broader reset in expectations that can weigh on sentiment toward smaller REITs like AH Realty Trust, particularly where growth visibility is closely scrutinized.

What’s in the News for AH Realty Trust

- AH Realty Trust reported that from January 1, 2026 to May 13, 2026, it repurchased 4,318,700 shares for US$27.1 million, bringing total buybacks under the June 15, 2023 program to 5,523,538 shares for US$39.73 million. Source: Company key developments.

- On May 13, 2026, AH Realty Trust announced a change to its equity buyback plan, increasing its share repurchase authorization by US$50 million to a total of US$100 million. Source: Company key developments.

- AH Realty Trust announced a long term office lease of approximately 22,000 square feet at its Southern Post mixed use project in Roswell, Georgia, with Industrious. This location is expected to open in early 2027 and to bring the office component of Southern Post to 83.5% leased. Source: Company key developments.

- Since opening in late 2024, Southern Post, owned by AH Realty Trust, has added multiple office tenants such as Vestis, CA South, and Risk Strategies, along with retail and dining concepts including Watch Your Wrist, Cavina Wellness, Grana, Azotea Cantina, Bey Mediterranean, and Da Vinci's Donuts. Source: Company key developments.

Valuation Changes for AH Realty Trust

- Fair Value: Updated to $7.00 from $7.88, reflecting a modest reduction in the modeled fair value for AH Realty Trust.

- Discount Rate: Adjusted slightly lower to 9.48% from 9.89%, indicating a small change in the required return used in the valuation model.

- Revenue Growth: The expected revenue decline has eased to a fall of 11.36% from a fall of 13.28%, pointing to a less pronounced contraction in the forecast.

- Net Profit Margin: Revised down to 9.33% from 19.37%, representing a significant reduction in projected profitability for AH Realty Trust.

- Future P/E: Increased to 31.55x from 14.63x, meaning the updated model now applies a much higher earnings multiple to AH Realty Trust.

Key Takeaways

- Strong leasing performance and strategic tenant mix are driving higher rents, margin expansion, and stable long-term revenue across diversified, high-demand urban and suburban properties.

- Shifting capital to high-growth assets and optimizing financing structure enhances cash flow predictability, portfolio quality, and positions the company for sustained value accretion.

- High leverage, sector exposure, geographic concentration, execution challenges, and rising compliance costs threaten flexibility, margins, and the stability of long-term earnings.

Catalysts

About Armada Hoffler Properties- Armada Hoffler (NYSE: AHH) is a vertically integrated, self-managed real estate investment trust with over four decades of experience developing, building, acquiring, and managing high-quality retail, office, and multifamily properties located primarily in the Mid-Atlantic and Southeastern United States.

- Armada Hoffler's consistent high occupancy and strong re-leasing spreads across its office and retail portfolios-driven by migration towards urban/suburban centers and demand for amenity-rich, mixed-use developments-position its properties to capture higher rents and bolster long-term revenue and NOI growth.

- The successful backfilling of vacated big-box retail spaces with high-credit tenants at substantial rent increases (33–60%) and proactive tenant mix optimization are increasing recurring property-level income, which should directly support margin expansion and earnings reliability.

- The company is experiencing rapid lease-up and resilient demand in its multifamily and mixed-use assets located in high-barrier, coastal, and growth-oriented markets, suggesting further upside for revenue and earnings as demographic shifts and urbanization underpin sustained rental demand.

- Strategic redeployment of capital from fully leased, lower-growth assets to higher-growth, grocery-anchored centers or multifamily acquisitions with favorable demographics enhances portfolio quality and is likely to generate accretive returns and asset value accretion over time.

- The recent transition to long-duration, fixed-rate debt and reduction in exposure to variable rate instruments will enhance cash flow predictability and net margins, especially as interest rate environments stabilize, supporting improved earnings and financing flexibility for future growth initiatives.

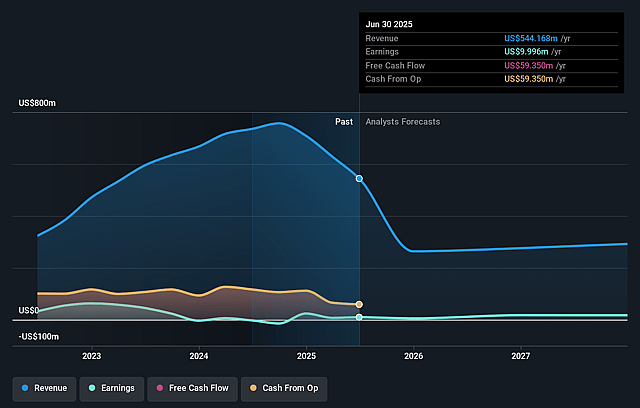

Armada Hoffler Properties Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming AH REALTY TRUST's revenue will decrease by 11.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.3% today to 9.3% in 3 years time.

- Analysts expect earnings to reach $18.6 million (and earnings per share of -$0.41) by about June 2029, up from $785.0 thousand today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 31.9x on those 2029 earnings, down from 645.4x today. This future PE is lower than the current PE for the US REITs industry at 44.5x.

- Analysts expect the number of shares outstanding to decline by 5.24% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.48%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's significant leverage, highlighted by a net debt to adjusted EBITDA of 7.7x and an AFFO payout ratio that rises to 97.2% after adjustments, exposes Armada Hoffler to potential interest rate increases, rising refinancing costs, and restricts flexibility, putting sustained pressure on net margins and distributable earnings.

- Ongoing exposure to the office and retail segments-despite current strong occupancies-remains a structural risk due to industry-wide threats such as persistent remote/hybrid work trends and the shift toward e-commerce, which could lead to longer-term demand declines, higher vacancy rates, and reduce both revenue and NOI over time.

- The company's portfolio concentration in the Mid-Atlantic and Southeastern U.S. markets heightens sensitivity to localized economic downturns, demographic shifts, or oversupply, increasing the risk of volatility in occupancy and rental growth, with direct impacts on both revenue stability and net operating income.

- The strategy's increasing reliance on large multifamily and mixed-use developments introduces execution risk and vulnerability to unexpected construction issues (e.g., the noted water intrusion at Greenside), which can lead to periods of units being offline, delayed lease-up, and higher capital expenditures, all potentially impacting net margins and earnings.

- Elevated ongoing capital and compliance requirements-stemming from tightening ESG, regulatory, and property improvement needs-may compress margins, as costs rise to meet market expectations and legal standards, thereby weighing on long-term profitability and AFFO growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $7.0 for AH REALTY TRUST based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $8.0, and the most bearish reporting a price target of just $6.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $199.8 million, earnings will come to $18.6 million, and it would be trading on a PE ratio of 31.9x, assuming you use a discount rate of 9.5%.

- Given the current share price of $6.67, the analyst price target of $7.0 is 4.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AH REALTY TRUST?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.