Last Update 17 Jun 26

SENS: Hydrogen Safety Sensors And Carbon Removal Efforts Will Support Balanced Outlook

Analysts have maintained their CHF fair value estimate for Sensirion Holding at CHF 82.0, making only minor adjustments to the discount rate, revenue growth, profit margin and future P/E assumptions, which results in a largely unchanged price target narrative.

What's in the News for Sensirion Holding

- Sensirion launched the STC42A automotive hydrogen sensor globally, targeting early detection of thermal runaway in electric vehicle batteries and hydrogen leaks, and aligning with new five minute warning safety rules. Source: recent product announcement.

- The STC42A hydrogen sensor is now available through Sensirion’s global channel partners, qualified to AEC Q100 (Grade 2) for automotive use and designed for reliable hydrogen concentration measurements in clean air for battery monitoring systems.

- The STC42A integrates a digital I2C interface that can autonomously communicate with the SHT41A humidity and temperature sensor. This enables real time absolute humidity compensation and delivers factory calibrated, fully compensated digital hydrogen output.

- ATMO’s new Atmotube PRO 2 portable air quality tracker incorporates multiple Sensirion sensors, including CO2, VOC and NOx, particulate matter, temperature and humidity solutions, to provide real time air quality monitoring in a compact device.

- Sensirion partnered with ClimeFi to secure a portfolio of durable carbon removal solutions across direct air capture, biomass with carbon removal and storage, and mineralization, supporting the company’s commitment to the Swiss net zero 2050 target.

Valuation Changes for Sensirion Holding

- Fair Value: CHF 82.0 remains unchanged, with no material shift in the overall CHF fair value estimate for Sensirion stock.

- Discount Rate: The discount rate assumption is adjusted slightly from 5.53% to 5.56%, indicating a modest tweak to the risk or return profile used in the model.

- Revenue Growth: The long term revenue growth assumption is effectively unchanged at about 5.96%, reflecting a stable view of Sensirion’s top line outlook in the model.

- Net Profit Margin: The net profit margin input is steady at roughly 9.50%, with only a minor rounding adjustment and no change in the underlying profitability view.

- Future P/E: The future P/E assumption is revised marginally from 37.37x to 37.40x, implying only a very small change in the valuation multiple used for Sensirion Holding.

Key Takeaways

- Innovation in environmental sensors and strategic acquisitions are driving expansion into new applications, supporting higher margins and recurring revenue streams.

- Strong market position in regulatory-driven HVAC sensors and targeted Asian growth ensure resilience and above-market revenue growth amid global sustainability trends.

- Heavy reliance on short-term industrial growth drivers and vulnerability to currency, policy, and regional demand shifts threaten future revenue stability and diversification.

Catalysts

About Sensirion Holding- Engages in the development, production, sale, and servicing of sensor systems, modules, and components in the Asia Pacific, Europe, the Middle East, Africa, and the Americas.

- Sensirion's ongoing commercialization of innovative CO₂ chip-level sensors is expected to unlock new applications and markets in environmental monitoring and building controls, positioning the company to benefit from increasing global emphasis on sustainability and decarbonization-this should drive revenue growth and support higher margins as adoption broadens.

- The market leadership in A2L refrigerant leakage sensors for HVAC systems directly addresses new U.S. and international regulations around climate-friendly, low-global-warming-potential refrigerants, setting up sustained demand as regulatory frameworks tighten-supporting stable to rising topline and margin resilience.

- Expansion into high-growth Asian markets and the ability to leverage Chinese stimulus efforts through diversified sales channels strengthens regional diversification and aligns with the broader proliferation of IoT and sensor-driven smart devices, which should underpin above-market revenue CAGR.

- Strategic acquisition of Kuva Systems and continued R&D investment point toward Sensirion's intent to move up the value chain with data-driven solutions and environmental sensing for industrial and energy applications, creating potential for higher-margin, recurring revenue streams.

- Ongoing operational leverage from productivity gains, capacity utilization improvements, and disciplined OpEx management are expected to enable incremental EBITDA and net margin expansion as sales volumes grow, amplifying earnings potential over the medium term.

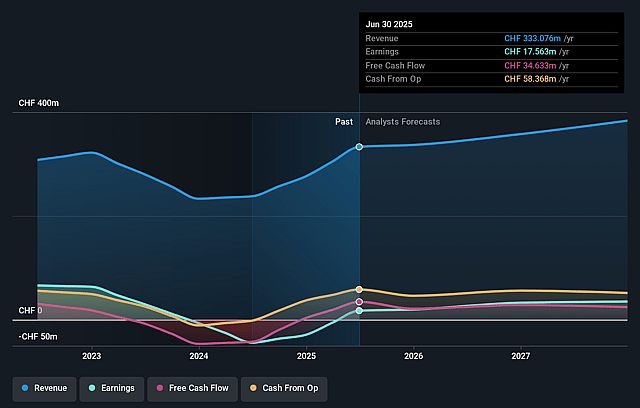

Sensirion Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Sensirion Holding's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.9% today to 9.5% in 3 years time.

- Analysts expect earnings to reach CHF 38.7 million (and earnings per share of CHF 2.48) by about June 2029, up from CHF 20.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CHF51.5 million in earnings, and the most bearish expecting CHF34.2 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 38.6x on those 2029 earnings, down from 64.5x today. This future PE is lower than the current PE for the CH Electronic industry at 60.5x.

- Analysts expect the number of shares outstanding to decline by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.56%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Significant exposure to currency fluctuations, particularly Swiss franc appreciation against other major currencies like the US dollar, has already led to a negative financial impact (CHF 10 million finance loss in H1 2025) and could further erode net income and future earnings.

- Persistent and unpredictable changes in US trade policy, including tariffs, create ongoing uncertainty in key markets, which may indirectly reduce global demand and directly disrupt supply chains-both posing medium

- to long-term risks to top-line revenue growth.

- The recent spike in industrial segment growth is heavily reliant on the one-off ramp-up of A2L refrigerant leakage sensors, with management already warning of normalization and no further growth expected from this application; failure to identify similarly high-impact growth drivers in the future could stall revenue and profit momentum.

- Weakness or stagnation in the automotive sector, Sensirion's second-largest segment (21% of sales), due to limited new project rollouts and exposure to struggling Western markets (rather than high-growth Asian markets), poses structural risk to diversification and future revenue streams.

- Partial phase-out of stimulus programs in China is likely to dampen demand in consumer and appliance sensor markets, threatening sustained growth in APAC and putting pressure on consolidated revenue as regulator-driven and stimulus-driven demand wanes.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CHF82.0 for Sensirion Holding based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF92.0, and the most bearish reporting a price target of just CHF70.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CHF407.3 million, earnings will come to CHF38.7 million, and it would be trading on a PE ratio of 38.6x, assuming you use a discount rate of 5.6%.

- Given the current share price of CHF83.4, the analyst price target of CHF82.0 is 1.7% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Sensirion Holding?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.