Catalysts

About Vitesse Energy

Vitesse Energy participates in oil and gas development in the Bakken through both non operated interests and a growing operated position.

What are the underlying business or industry changes driving this perspective?

- Extended 3 and 4 mile laterals are improving drilling and completion cost per lateral foot. However, any plateau in operator activity across Vitesse acreage could limit how much this efficiency appears in future revenue growth.

- Technology is allowing development to push further into areas where Vitesse holds concentrated non core positions. Returns from these locations may prove less consistent over time and could cap margins if well results differ from the early operated DUCs that came in under budget.

- The company has over 2 million net lateral feet and more than 200 net 2 mile equivalent wells in the inventory. The pace at which third party operators choose to develop this footprint may slow in future planning cycles, which would temper production volumes and EBITDA contributions from this long duration asset base.

- The company is currently using hedges with oil floors near US$70 per barrel and gas collars with floors in the US$3.70 range. Future hedge resets at less favorable prices would reduce cash flow visibility and could squeeze net margins even if physical volumes hold steady.

- Low leverage, with net debt to adjusted annualized EBITDA at 0.65x, supports the current dividend focus. Higher future capital intensity from operated programs or acquisitions in a competitive AFE and M&A market could pressure free cash flow and earnings if returns on new projects do not match historical thresholds.

Assumptions

This narrative explores a more pessimistic perspective on Vitesse Energy compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Vitesse Energy's revenue will remain fairly flat over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 8.4% today to 0.0% in 3 years time.

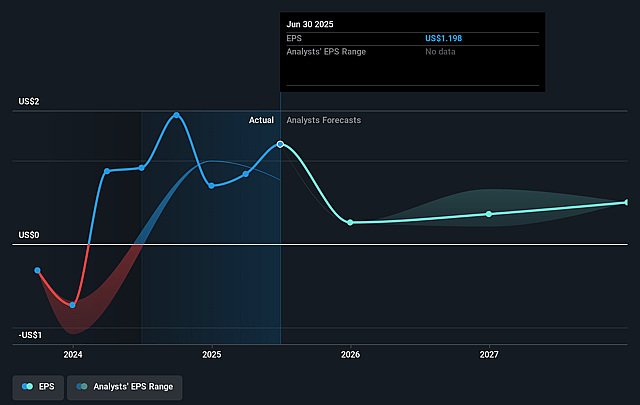

- The bearish analysts expect earnings to reach $30.8 thousand (and earnings per share of $0.42) by about January 2029, down from $20.9 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $169.6 thousand.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 30919.0x on those 2029 earnings, up from 37.1x today. This future PE is greater than the current PE for the US Oil and Gas industry at 13.5x.

- The bearish analysts expect the number of shares outstanding to grow by 0.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.96%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Extended 3 and 4 mile laterals are becoming a larger share of activity and are reported to be delivering strong economic results through lower drilling and completion cost per lateral foot. This could support higher long term production and cash flow than implied by a flat share price view, affecting revenue and earnings.

- Management highlights that drilling activity is progressing further into areas where Vitesse holds concentrated positions and that acreage outside the core is now generating returns comparable to core areas. This could increase the value of the remaining 2 million net lateral feet and more than 200 net 2 mile equivalent wells, with potential upside for revenue and margins.

- The company is actively evaluating a 2026 and 2027 operated program and continues to review around 15 net undeveloped locations from the Lucero acquisition. A step up in operated development at acceptable return thresholds could lift production and improve earnings and free cash flow beyond what a flat share price would suggest.

- Management describes the acquisition market as very strong, with hundreds of AFE opportunities reviewed and about $1b of deals in the internal pipeline. If Vitesse continues to find and fund accretive deals within operating cash flow, this could support long term growth in production, revenue and EBITDA.

- Low leverage with net debt to adjusted annualized EBITDA at 0.65x and a focus on a dividend that is currently set at an annual rate of US$2.25 per share give the company financial flexibility. If this balance sheet strength allows Vitesse to be opportunistic during industry cycles, it could support more resilient margins and earnings than implied by a flat share price expectation.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Vitesse Energy is $20.0, which represents up to two standard deviations below the consensus price target of $25.0. This valuation is based on what can be assumed as the expectations of Vitesse Energy's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $32.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $246.2 million, earnings will come to $30.8 thousand, and it would be trading on a PE ratio of 30919.0x, assuming you use a discount rate of 7.0%.

- Given the current share price of $20.05, the analyst price target of $20.0 is 0.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Vitesse Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.