Last Update 19 Apr 26

Fair value Increased 1.11%DUK: Data Center Load And New Gas Project Will Shape Balanced Outlook

The analyst price target for Duke Energy has shifted higher, rising about $1.50 to $139.82 as analysts factor in updated assumptions for revenue growth, profit margins and future P/E following a series of recent target revisions across the Street.

Analyst Commentary

Recent research updates on Duke Energy show a mix of higher price targets and at least one rating downgrade. Taken together, these moves frame how the Street is thinking about execution risk, growth opportunities and where the shares sit relative to perceived fair value.

Bullish Takeaways

- Bullish analysts have raised price targets by figures such as $3, $4, $7, $16 and to $139 from $130, reflecting refreshed models that factor in updated assumptions for revenue growth, profit margins and P/E expectations.

- Some bullish commentary highlights Duke's premium-service state service territory and significant load growth pipeline, which they see as supportive of longer term growth in the regulated utility footprint.

- Electric capex that is eligible for efficient recovery mechanisms is cited as a positive for earnings visibility and potential returns on invested capital within the regulated business.

- Where price targets have been maintained or raised while ratings stay at Equal Weight type stances, it signals that analysts see fundamental support for current valuation levels even if they are not leaning aggressively positive.

Bearish Takeaways

- Bearish analysts have lowered some price targets by amounts such as $1, $3 and $11, which points to caution around previous valuation assumptions or risk factors that could affect earnings power.

- A downgrade to an In Line rating with a price target of $139, reduced from $143, reflects a view that after roughly a 15% share price move since early December, the risk or reward trade off is less compelling in the near term.

- Even those who describe themselves as constructive on Duke's growth potential are signaling a preference to wait, suggesting that recent share appreciation may have already captured a meaningful portion of their expected upside.

- Comments around updated price targets for the broader utilities group, alongside utilities underperforming the S&P's return in the referenced month, suggest some analysts are carefully weighing sector level sentiment when setting valuation ranges for Duke.

What's in the News

- Federal Energy Regulatory Commission staff inspected multiple Duke Energy hydro facilities at the Mountain Island, Oxford, Rhodhiss and Lookout Shoals developments and reported no problems that present an immediate concern for dam safety or continued operation, with construction observed to follow approved plans and specifications (FERC correspondence).

- FERC approved a revised Drilling Program Plan for spillway improvements at the Nantahala Dam Project, authorized a named field professional to supervise drilling work and requested notification before field activities so staff can attend, indicating continued regulatory oversight of hydropower projects (FERC correspondence).

- A follow up FERC letter on the Walters Project annual dam safety inspection reported no issues requiring follow up actions and acknowledged Duke Energy's cooperation in maintaining project safety (FERC correspondence).

- The Public Service Commission of South Carolina approved construction of a new natural gas generation facility in Anderson County, expected to provide about 1,365 MW of nominal capacity, with survey estimates of more than 2,200 jobs annually during construction and an annual US$84 million economic impact once operational (company announcement).

- Duke Energy proposed an amendment to its Amended and Restated Certificate of Incorporation to eliminate supermajority requirements at the annual general meeting scheduled for May 7, 2026 (company filing).

Valuation Changes

- Fair Value: updated from $138.29 to $139.82, a small upward adjustment of about 1.1% in the modeled estimate.

- Discount Rate: held essentially steady at 6.98%, indicating no meaningful change in the assumed cost of capital.

- Revenue Growth: revised slightly higher from 4.88% to 4.93%, reflecting a modest uplift in projected top line expansion.

- Net Profit Margin: adjusted marginally lower from 16.88% to 16.86%, a very small refinement in expected profitability.

- Future P/E: moved modestly higher from 21.28x to 21.50x, suggesting a slightly richer multiple in the updated assumptions.

Key Takeaways

- Strong regional economic activity and supportive legislation are expected to drive sustained growth in revenues, earnings stability, and operational efficiency.

- Investment in grid modernization, renewables, and nuclear enhances financial flexibility and positions Duke favorably for the ongoing energy transition.

- Accelerating distributed energy adoption, regulatory risks, capital needs, and fossil fuel reliance threaten Duke Energy's revenue growth, margins, and financial flexibility amid the energy transition.

Catalysts

About Duke Energy- Through its subsidiaries, operates as an energy company in the United States.

- Major economic development wins (e.g., AWS's $10B data center in North Carolina), paired with accelerated migration and manufacturing demand in Duke's service territory, are expected to drive robust, multi-year load and volume growth, supporting higher revenues and long-term EPS growth.

- Supportive state and federal legislation-such as the Power Bill Reduction Act in NC and the Energy Security Act in SC-streamlines cost recovery for new generation and grid investments, reducing regulatory lag and improving cash flow and earnings stability over the next decade.

- Significant infrastructure and grid modernization investment (e.g., over $4 billion incremental CapEx in Florida) is positioned to capitalize on growing needs for digitalization and grid resilience, enabling Duke to enhance operational efficiency and reliability, which benefits both net margins and future rate base growth.

- Proceeds from recent asset sales and the minority stake sale (e.g., Brookfield in Florida) are being used to strengthen the balance sheet and de-risk future equity needs, improving the company's financial flexibility and lowering funding costs, which in turn should protect or expand net margins and earnings.

- Duke's large-scale commitment to nuclear and renewables (operating the nation's largest regulated nuclear fleet, plus long-term renewables investment pipeline) aligns with the ongoing clean energy transition, securing regulatory support and capturing production tax credits-directly boosting earnings and reducing exposure to commodity price volatility.

Duke Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

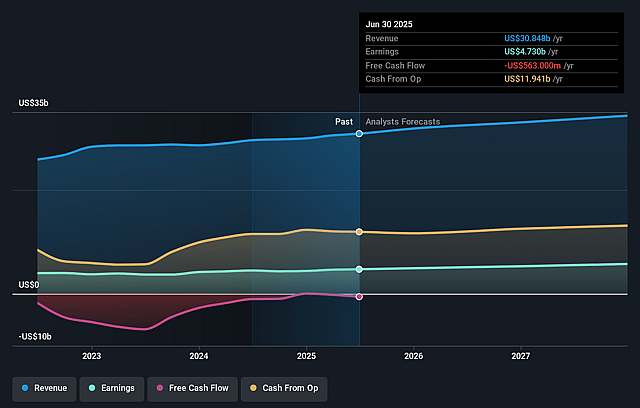

- Analysts are assuming Duke Energy's revenue will grow by 4.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.4% today to 16.9% in 3 years time.

- Analysts expect earnings to reach $6.2 billion (and earnings per share of $7.66) by about April 2029, up from $4.9 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 21.5x on those 2029 earnings, up from 20.3x today. This future PE is lower than the current PE for the US Electric Utilities industry at 22.2x.

- Analysts expect the number of shares outstanding to grow by 0.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.98%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Accelerating distributed energy adoption, such as solar and batteries by customers and businesses, could reduce long-term demand for Duke Energy's centralized grid services and utility-provided electricity, leading to potential stagnation or decline in sales and ultimately pressuring long-term revenue growth.

- Heavy reliance on natural gas and legacy coal infrastructure complicates Duke's transition to renewables, which could result in higher capital expenditures, increased compliance costs, and exposure to stranded asset risk as decarbonization policies accelerate-negatively impacting net margins and future earnings.

- Significant increases in capital needs for grid modernization, generation investments, and new project developments-especially to serve large customers like data centers-raise Duke Energy's dependence on external financing, amplifying vulnerability to persistent inflation and higher interest rates that can compress returns and elevate interest expense, thereby reducing net income.

- While recent legislative and regulatory outcomes have been supportive, any future unfavourable regulatory changes (such as potential shifts to performance-based ratemaking or customer rate resistance) could introduce earnings variability, limit guaranteed returns, or constrain rate base growth, all of which may adversely affect regulated revenue and EPS trajectory.

- Elevated balance sheet leverage and large deferred equity issuance plans heighten refinancing and credit downgrade risks, particularly if capital markets tighten or operational execution falters, which could increase borrowing costs, reduce financial flexibility, and ultimately negatively impact net income and shareholder returns.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $139.82 for Duke Energy based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $36.7 billion, earnings will come to $6.2 billion, and it would be trading on a PE ratio of 21.5x, assuming you use a discount rate of 7.0%.

- Given the current share price of $128.03, the analyst price target of $139.82 is 8.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Duke Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.