Catalysts

About HORNBACH Holding KGaA

HORNBACH Holding KGaA operates large project focused DIY and home improvement stores, supported by integrated online channels, across Germany and multiple European markets.

What are the underlying business or industry changes driving this perspective?

- Continued roll out of large format DIY stores across Europe, including new flagship sites and concept formats such as BODENHAUS, increases selling space and catchment coverage. This can support higher group revenue and operating earnings over time.

- Entry into Serbia, where management sees room for 6 to 8 large stores and has already secured several locations, adds a fresh growth region. This can broaden the earnings base and support long term EBIT contribution once stores mature.

- Consistent market share gains in key countries such as Germany, the Netherlands, Czechia, Austria and Switzerland, supported by assortment depth, pricing and service, can help sustain like for like growth. This can support gross profit and net margins if scale benefits continue.

- Growing e commerce, now 12.9% of sales with 8.1% sales growth and solid contributions from both Direct delivery and Click & Collect, deepens customer engagement and can lift total revenue. This can also support more efficient inventory and working capital usage.

- Rising sales to professional customers, particularly in building materials and renovation related services, together with double digit growth in installation services, can support higher basket sizes and potentially more resilient revenue and EBIT through the cycle.

- Ongoing investment in IT infrastructure, software and AI to improve efficiency and working capital management, alongside a strong equity ratio of 47.1% and lower net financial debt to EBITDA of 2.5x, can support cost discipline and underpin future net margin and earnings quality.

Assumptions

This narrative explores a more optimistic perspective on HORNBACH Holding KGaA compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

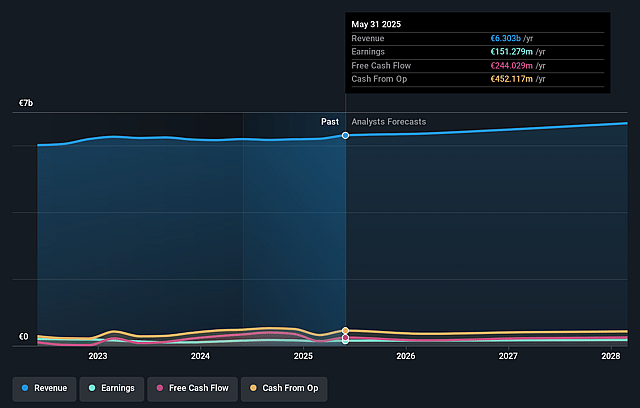

- The bullish analysts are assuming HORNBACH Holding KGaA's revenue will grow by 2.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 2.1% today to 2.7% in 3 years time.

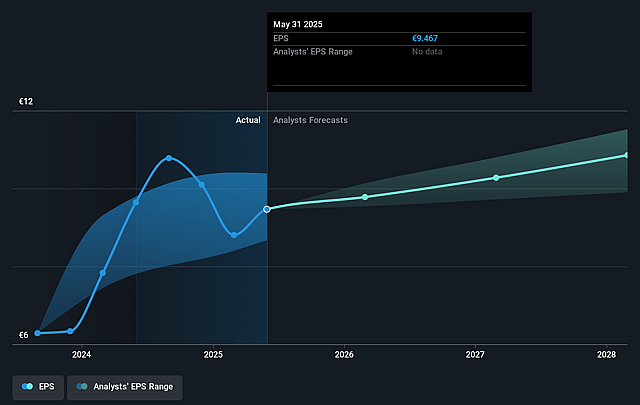

- The bullish analysts expect earnings to reach €189.5 million (and earnings per share of €11.84) by about February 2029, up from €133.5 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €143.9 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 12.6x on those 2029 earnings, up from 9.6x today. This future PE is lower than the current PE for the GB Specialty Retail industry at 17.2x.

- The bullish analysts expect the number of shares outstanding to decline by 0.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.98%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Consumer sentiment has been weak in Germany and other regions and management only expects net sales and adjusted EBIT to be at or slightly above the prior year, so if this subdued demand becomes a longer term pattern, store productivity and like for like growth could stall and put pressure on revenue and earnings.

- The business is committing to higher and sustained CapEx, including €25 million to €40 million per new Serbian store and a run rate of elevated investment across Europe. If new locations fail to reach the hurdle rate set by the weighted average cost of capital, returns on invested capital and free cash flow could fall even if headline sales grow.

- Personnel expenses are a large part of the cost base, about 60% of total costs, and grew 4.9% to €871 million in the first 9 months due to wage increases and new headcount. If wage inflation and staffing needs continue to run ahead of sales growth, operating leverage could work in reverse and weigh on net margins and EBIT.

- The project to improve IT infrastructure and introduce software and AI is expected to deliver efficiency benefits only over time. If the benefits are delayed or smaller than planned, the company could carry structurally higher general and administrative and selling costs that constrain earnings and cash generation.

- The expansion model depends on growing markets such as Serbia and on stable or improving conditions in existing countries. Recent examples like Romania's budget adjustments and weather related disruption in Czechia show that external shocks can hit purchasing power and store traffic, which could lead to volatile revenue and profit contribution from newer regions.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for HORNBACH Holding KGaA is €117.0, which represents up to two standard deviations above the consensus price target of €100.57. This valuation is based on what can be assumed as the expectations of HORNBACH Holding KGaA's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €117.0, and the most bearish reporting a price target of just €80.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be €6.9 billion, earnings will come to €189.5 million, and it would be trading on a PE ratio of 12.6x, assuming you use a discount rate of 9.0%.

- Given the current share price of €80.7, the analyst price target of €117.0 is 31.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on HORNBACH Holding KGaA?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.