Earnings Update: The Hershey Company (NYSE:HSY) Just Reported Its Full-Year Results And Analysts Are Updating Their Forecasts

The Hershey Company (NYSE:HSY) came out with its yearly results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. It was a credible result overall, with revenues of US$11b and statutory earnings per share of US$9.06 both in line with analyst estimates, showing that Hershey is executing in line with expectations. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

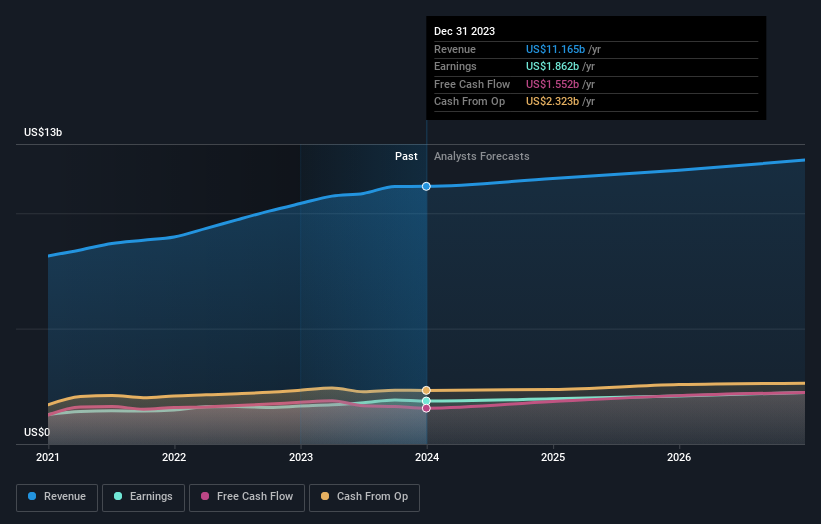

See our latest analysis for Hershey

Taking into account the latest results, the consensus forecast from Hershey's 23 analysts is for revenues of US$11.5b in 2024. This reflects a modest 3.1% improvement in revenue compared to the last 12 months. Per-share earnings are expected to increase 4.8% to US$9.57. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$11.5b and earnings per share (EPS) of US$9.62 in 2024. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

The analysts reconfirmed their price target of US$212, showing that the business is executing well and in line with expectations. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Hershey, with the most bullish analyst valuing it at US$238 and the most bearish at US$183 per share. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's pretty clear that there is an expectation that Hershey's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 3.1% growth on an annualised basis. This is compared to a historical growth rate of 8.4% over the past five years. Compare this to the 145 other companies in this industry with analyst coverage, which are forecast to grow their revenue at 2.5% per year. So it's pretty clear that, while Hershey's revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Hershey going out to 2026, and you can see them free on our platform here..

And what about risks? Every company has them, and we've spotted 1 warning sign for Hershey you should know about.

가치 평가는 복잡하지만, 저희는 이를 단순화하고자 합니다.

공정가치 추정치, 잠재적 위험, 배당금, 내부자 거래 및 재무 상태를 포함한 자세한 분석을 통해 Hershey 의 저평가 또는 고평가 여부를 알아보세요.

무료 분석에 액세스Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

This article has been translated from its original English version, which you can find here.