Last Update 12 Nov 25

Fair value Increased 1.57%PPH: Lower Discount Rate Will Likely Support Upside Momentum Ahead

The analyst price target for Pepkor Holdings has risen modestly from R32.25 to R32.76, as analysts cite improved revenue growth estimates and a lower discount rate, which supports a more favorable outlook.

Analyst Commentary

Bullish Takeaways

- Bullish analysts note that improved revenue growth estimates have contributed to upward adjustments in the target price.

- An enhanced outlook is supported by a lower discount rate, which increases Pepkor Holdings' valuation potential.

- Upgrades in analyst ratings from Hold to Buy reflect growing confidence in the company’s execution and market position.

- The price target being set above current trading levels suggests potential for further share price appreciation.

Bearish Takeaways

- Some analysts remain cautious about achieving ambitious revenue growth projections in a competitive retail environment.

- There are concerns that future performance may be tempered if macroeconomic conditions weaken.

- Risk remains around the sustainability of margin improvements, which could impact long-term valuation assumptions.

What's in the News

- Pepkor Holdings issued new earnings guidance for the year ending 30 September 2025, projecting Continuing operations EPS in the range of 149.6 to 156.0 cents and Continuing operations HEPS between 153.6 and 167.6 cents (Key Developments).

- For total operations, including discontinued activities, the company expects EPS to be between 150.0 and 155.7 cents, and HEPS to range from 153.1 to 168.0 cents (Key Developments).

Valuation Changes

- Consensus Analyst Price Target has risen slightly from ZAR32.25 to ZAR32.76, reflecting improved sentiment.

- Discount Rate has decreased modestly from 20.63% to 20.33%, indicating lower perceived risk in Pepkor Holdings' valuation model.

- Revenue Growth projections have increased marginally, moving from 10.28% to 10.38%.

- Net Profit Margin estimate has fallen significantly from 11.40% to 8.96%.

- Future P/E ratio has increased from 15.03x to 19.25x, suggesting that higher valuation multiples are being applied.

Key Takeaways

- Acquisitions and aggressive expansion plans could drive revenue growth through improved market presence and increased penetration across new territories and cellular formats.

- Enhanced financial services and improved logistics are likely to boost net margins and operating income through increased earnings and reduced operational costs.

- Supply chain disruptions, underperformance in segments, reliance on financial services, and currency risks could impact revenue, margins, cash flow, and earnings stability.

Catalysts

About Pepkor Holdings- Operates as a retailer focusing on discount, value, and specialized goods in Angola, Botswana, Brazil, Eewatini, Lesotho, Mozambique, Malawi, Namibia, South Africa, and Zambia.

- The introduction of new acquisitions such as Choice Clothing and OK Furniture is expected to drive revenue growth and improve market presence in new territories. This could result in higher revenues and improved operating margins due to synergies and cross-selling opportunities.

- Expansion in Brazil and an aggressive store opening plan across different brands, including a focus on cellular formats, suggests potential revenue growth from increased market penetration and footprint expansion.

- Enhanced FinTech and financial services contributions, particularly through innovations like the FoneYam handset rental product, are expected to substantially increase earnings and operating profits, improving net margins due to higher product and service uptake.

- The strategic focus on increasing insurance capabilities, backed by an existing extensive distribution and collection network, is anticipated to create a sizable insurance business, boosting net margins and operating income through embedded financial service products.

- Continued cost control measures, along with operational efficiencies achieved from integrating and upgrading logistics and distribution networks (such as the opening of a second distribution center in Brazil), may improve net margins by reducing operational costs over time.

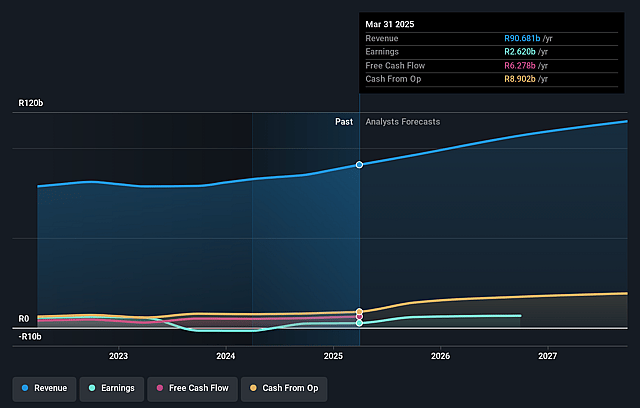

Pepkor Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Pepkor Holdings's revenue will grow by 10.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.9% today to 11.4% in 3 years time.

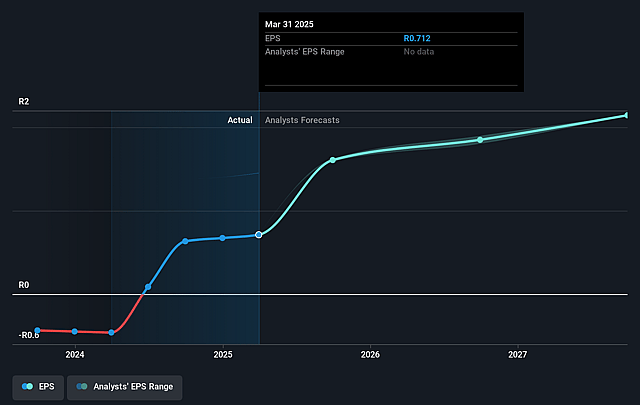

- Analysts expect earnings to reach ZAR 13.9 billion (and earnings per share of ZAR 2.14) by about September 2028, up from ZAR 2.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.0x on those 2028 earnings, down from 34.7x today. This future PE is greater than the current PE for the ZA Specialty Retail industry at 8.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 20.63%, as per the Simply Wall St company report.

Pepkor Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There are supply chain challenges, notably port disruptions and lack of container availability, impacting store openings and product availability. This could affect revenue growth if it continues.

- There were instances of underperformance in certain business segments, such as Tekkie Town due to high market competition and discounts, and issues with the new store maturity curve in Brazil. These could suppress net margins and profits if not resolved.

- The reliance on financial service growth through products like FoneYam and A+ card may mean the core retail business isn't growing as robustly, potentially affecting long-term earnings stability.

- Increased investment in inventory might strain cash flow if sales don't meet expectations, evidenced by the increased inventory levels in response to supply chain issues, which can impact cash conversion rates.

- Currency fluctuations, particularly affecting PEP Africa operations, could impact revenue when converted to rand, adding a foreign exchange risk to financial results.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ZAR32.25 for Pepkor Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ZAR34.7, and the most bearish reporting a price target of just ZAR27.7.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ZAR121.6 billion, earnings will come to ZAR13.9 billion, and it would be trading on a PE ratio of 15.0x, assuming you use a discount rate of 20.6%.

- Given the current share price of ZAR24.74, the analyst price target of ZAR32.25 is 23.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.