Key Takeaways

- Potential financial strain from high capital spending on RNG projects and propane operations may impact cash flows and net margins before returns materialize.

- Profitability and revenue depend on successful RNG production, tax credits, and navigating volatile market and regulatory conditions.

- Strategic growth through acquisitions, effective pricing, renewable investments, and monetizing tax credits supports revenue, profitability, and stability amid market volatility and low-carbon transitions.

Catalysts

About Suburban Propane Partners- Through its subsidiaries, engages in the retail marketing and distribution of propane, renewable propane, fuel oil, and refined fuels in the United States.

- The expectation of significant capital spending on RNG projects and propane operations, which could strain cash flows and leverage further before realizing anticipated benefits. This impacts net margins and potentially earnings due to higher upfront expenditures before future returns are actualized.

- Supply-demand dynamics where propane revenues remain sensitive to unpredictable weather patterns, particularly given recent decreases in demand from warm weather and an inconsistent agricultural sector. Future revenue is therefore exposed to volatility.

- Elevated leverage ratio of 4.99x potentially signals higher financial risk, as the company's strategy involves significant borrowings to fund acquisitions and growth projects. This is likely to put pressure on net income and interest expenses if earnings do not increase proportionately.

- The accounting charges and write-downs of $19.8 million in investments signal potential risks in the future valuation of early-stage renewable investments, casting uncertainty over asset and investment revenue returns, especially in a challenging equity funding climate.

- Dependence on future RNG production and tax credits under the IRA to improve financial metrics suggests that profitability and revenue enhancement are reliant on successfully operationalizing facilities and monetizing credits, which may shift based on regulatory or market conditions.

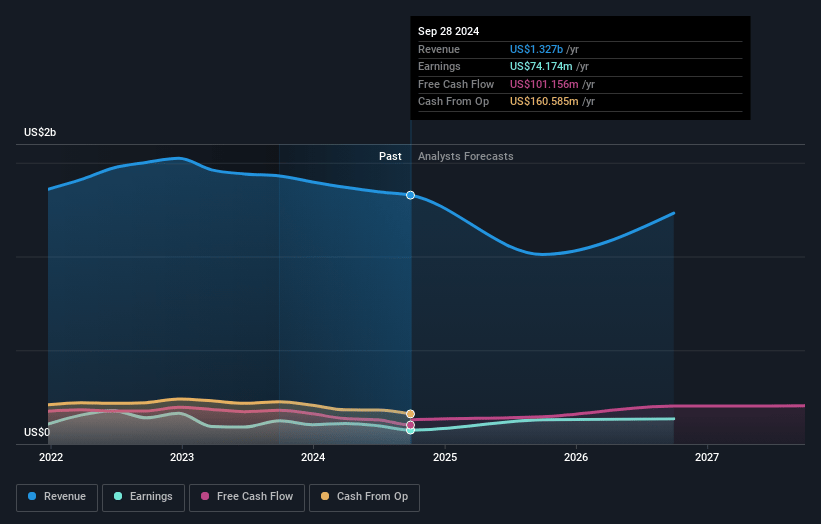

Suburban Propane Partners Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Suburban Propane Partners's revenue will grow by 4.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.2% today to 10.9% in 3 years time.

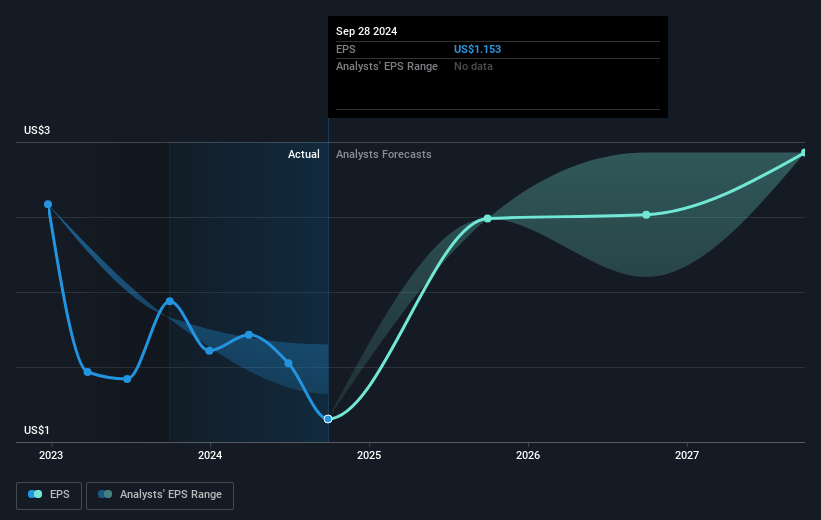

- Analysts expect earnings to reach $164.7 million (and earnings per share of $2.02) by about March 2028, up from $69.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.2x on those 2028 earnings, down from 18.7x today. This future PE is lower than the current PE for the US Gas Utilities industry at 19.1x.

- Analysts expect the number of shares outstanding to grow by 0.7% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.72%, as per the Simply Wall St company report.

Suburban Propane Partners Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The acquisition of a well-run propane business in the Southwest territory and strategic investments has helped to offset reduced demand due to warm weather, indicating potential growth in revenue through market expansion.

- Suburban Propane's field operations' ability to manage selling prices effectively in a high commodity price environment could positively impact net margins by maintaining profitability despite volatile market conditions.

- Expectation of increased RNG production following facility enhancements and capital projects may result in improved earnings from the renewable natural gas operations.

- Monetization of production tax credits (PTCs) from renewable gas facilities is anticipated to bolster cash flow, positively impacting net income and supporting ongoing financial stability.

- The company's focus on strategic growth plans, including renewable energy investments and propane business expansion, is intended to sustain revenue streams and future earnings in line with a low-carbon economy transition, potentially offsetting any downturns in traditional propane sales.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $17.0 for Suburban Propane Partners based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.5 billion, earnings will come to $164.7 million, and it would be trading on a PE ratio of 8.2x, assuming you use a discount rate of 6.7%.

- Given the current share price of $20.0, the analyst price target of $17.0 is 17.6% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives