Narratives are currently in beta

Key Takeaways

- Successful regulatory settlements and strategic financial measures are enhancing revenue stability and growth, with a focus on predictable financial outcomes.

- Significant capital investment in infrastructure and energy efficiency, alongside growth in nuclear power, underpins long-term growth and improved margins.

- Delays in auctions and regulatory pressures create uncertainty in revenue stability, while high expenditures and depreciation impact cash flow and net margins.

Catalysts

About Public Service Enterprise Group- Through its subsidiaries, operates in electric and gas utility business in the United States.

- The successful settlement of two major regulatory filings, including the base rate case and the clean energy energy efficiency programs, is expected to provide increased annual revenues and improve financial predictability, positively impacting PSEG's revenue and earnings growth.

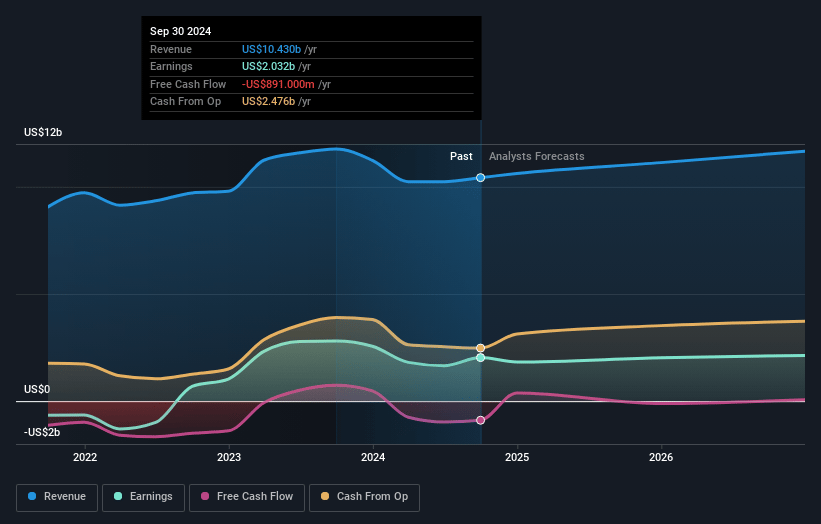

- The ongoing capital investment plan, totaling $19 billion to $22.5 billion through 2028, particularly in infrastructure modernization and energy efficiency, is projected to drive a compound annual growth rate in rate base of 6% to 7.5%, supporting long-term revenue and earnings growth.

- PSEG is positioning itself to benefit from long-term growth opportunities in nuclear power, potentially achieving increased outputs and long-term contracts at higher prices, which would significantly contribute to gross margins and earnings.

- PSEG's strategic moves to increase predictability of financial results through new pension and storm deferral mechanisms, along with their focus on reducing variability in financial outcomes, are aimed at stabilizing net margins and supporting sustainable earnings growth.

- The company's commitment to advancing energy efficiency initiatives and supporting New Jersey's state policy, including potential data center expansion, could attract more technology-based businesses, boosting revenue and enhancing net margins through higher-margin customer mix and electrification initiatives.

Public Service Enterprise Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Public Service Enterprise Group's revenue will grow by 5.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 19.5% today to 18.9% in 3 years time.

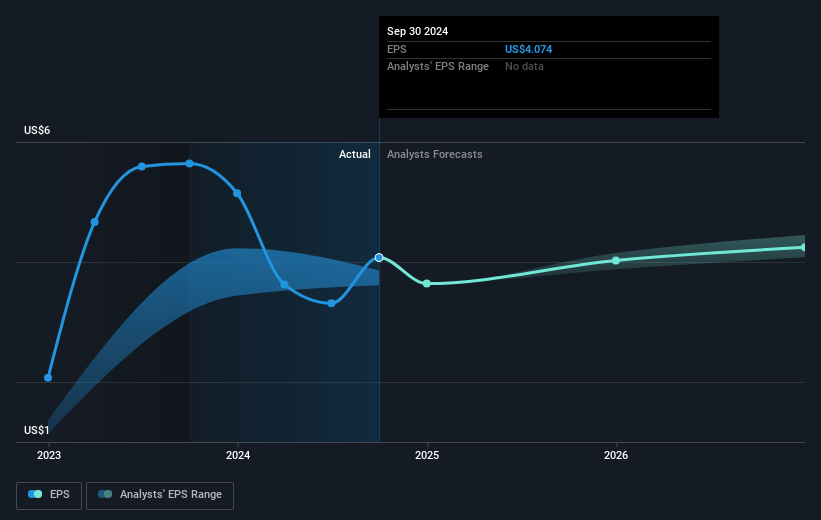

- Analysts expect earnings to reach $2.3 billion (and earnings per share of $4.46) by about November 2027, up from $2.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $2.6 billion in earnings, and the most bearish expecting $2.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.4x on those 2027 earnings, up from 20.5x today. This future PE is greater than the current PE for the US Integrated Utilities industry at 19.7x.

- Analysts expect the number of shares outstanding to grow by 1.64% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 5.8%, as per the Simply Wall St company report.

Public Service Enterprise Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Non-GAAP operating earnings showed minimal growth from $0.85 in Q3 2023 to $0.90 in Q3 2024, reflecting slower earnings growth potential. [Earnings]

- High investment-related depreciation and interest expenses offset rate base growth, affecting net income performance. [Net margins]

- Delays in capacity auctions create uncertainty in future revenue streams, potentially impacting financial stability. [Revenue]

- New capital and operational expenditures, such as nuclear upgrades and data center developments, may not immediately translate into profit, affecting cash flow and leverage. [Net margins]

- Pressure from regulatory and tax changes, such as new pension and storm deferral mechanisms, may influence future rate and revenue structures. [Revenue]

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $88.28 for Public Service Enterprise Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $102.0, and the most bearish reporting a price target of just $68.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $12.3 billion, earnings will come to $2.3 billion, and it would be trading on a PE ratio of 23.4x, assuming you use a discount rate of 5.8%.

- Given the current share price of $83.78, the analyst's price target of $88.28 is 5.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives