Key Takeaways

- CMS Energy's investments in renewable energy and utility customer service aim to boost revenue through improved reliability and diversified streams.

- Strategic cost management and financial mechanisms are anticipated to enhance margins and support growth, aligning with Michigan's economic development.

- Large investment plans and financing needs could strain CMS Energy's resources, impacting margins and posing risks to project execution, weather-related sales, and regulatory compliance.

Catalysts

About CMS Energy- Operates as an energy company primarily in Michigan.

- CMS Energy's 5-year $20 billion utility customer investment plan is designed to deliver improved customer service and reliability, which supports 8.5% rate base growth through 2029. This is expected to positively impact revenue growth.

- The 20-year Renewable Energy Plan involving 9 gigawatts of solar and 4 gigawatts of wind investments aligns with Michigan's clean energy transformation and energy law, which may enhance CMS Energy's net earnings through diversified revenue streams and potential cost savings from renewable energy sources.

- The financial compensation mechanism that allows earnings on power purchase agreements (PPAs) and energy efficiency incentives is projected to generate significant earnings, as noted with $20 million of incentives by the end of the decade, benefiting net margins.

- CMS Energy's expectation of 2% to 3% annual load growth due to economic development in Michigan, spurred by manufacturing and data centers, is likely to bolster future revenue.

- The company's strategic cost management initiatives, including the CE Way for process improvements and cost savings, aim at keeping rates affordable while funding growth, potentially improving net margins and overall earnings.

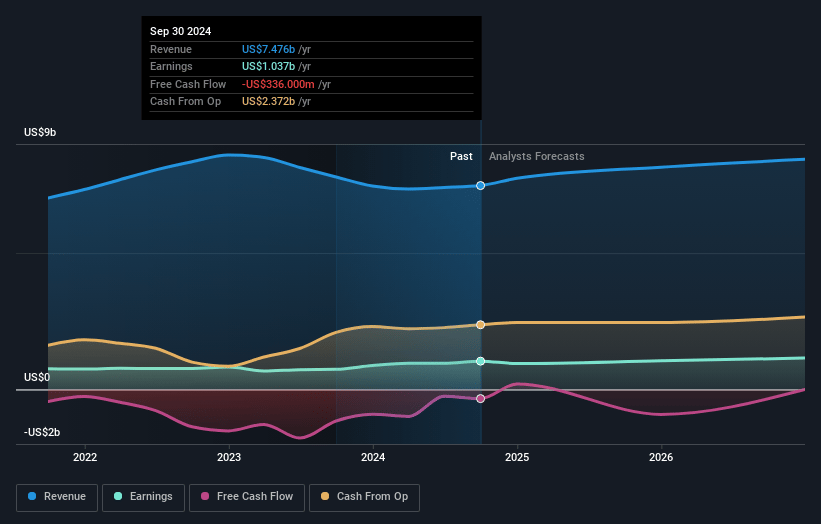

CMS Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CMS Energy's revenue will grow by 5.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.2% today to 14.6% in 3 years time.

- Analysts expect earnings to reach $1.3 billion (and earnings per share of $4.16) by about March 2028, up from $993.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.3x on those 2028 earnings, down from 22.1x today. This future PE is lower than the current PE for the US Integrated Utilities industry at 22.1x.

- Analysts expect the number of shares outstanding to grow by 0.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

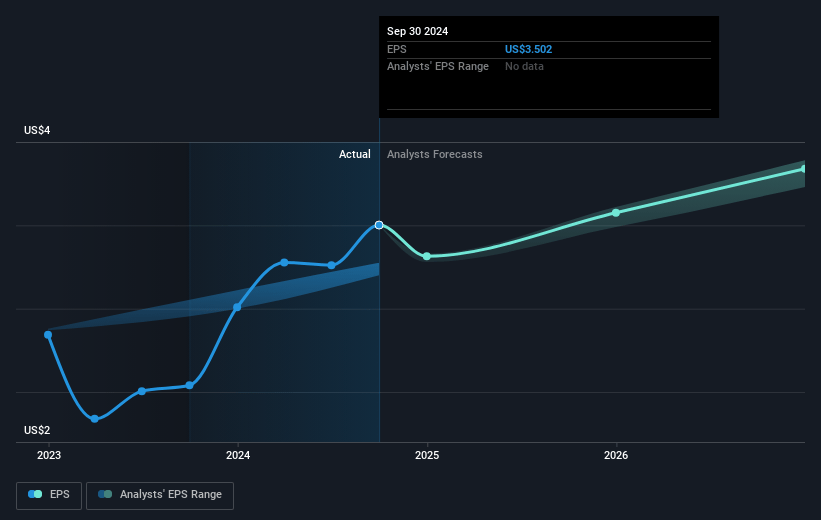

CMS Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- CMS Energy's large investment plans, including a $20 billion utility customer investment plan and additional opportunities exceeding $20 billion, could strain its financial resources and increase the risk of capital cost overruns and financing challenges, potentially impacting net margins and earnings.

- The need to manage significant weather-related financial headwinds, such as mild winters, creates uncertainty around weather-normalized sales and could impact revenue and earnings stability.

- Increased equity issuance and debt financing requirements to support the ambitious capital expenditure plan may dilute shareholder value and increase financial leverage, affecting net margins and overall returns.

- Potential difficulties with executing large renewable energy projects amid permitting challenges, changes in federal regulations, or supply chain issues could delay project completion and impact the company's ability to meet regulatory requirements and future revenue targets.

- While CMS Energy anticipates robust load growth, reliance on favorable economic conditions and continued support from regulatory environments is essential. Any changes or challenges in these areas could limit the ability to pass costs onto customers, impacting revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $72.621 for CMS Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $79.0, and the most bearish reporting a price target of just $59.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $8.8 billion, earnings will come to $1.3 billion, and it would be trading on a PE ratio of 20.3x, assuming you use a discount rate of 6.2%.

- Given the current share price of $73.5, the analyst price target of $72.62 is 1.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.