Narratives are currently in beta

Key Takeaways

- Strategic investments in grid reliability and data centers at AES Indiana and AES Ohio are expected to drive significant revenue and earnings growth.

- Selling a stake in AES Ohio is anticipated to enhance growth and stabilize earnings through improved cash flow and credit metrics.

- Weather-related impacts, execution risks, market volatility, and capital expenditure dependence pose significant challenges to AES's revenue stability and future profitability.

Catalysts

About AES- Operates as a diversified power generation and utility company in the United States and internationally.

- AES has signed or been awarded 2.2 gigawatts of new contracts since the last call, including long-term renewable PPAs and increased data center load growth, which are expected to drive future revenue growth.

- The company has added 1.3 gigawatts of new PPAs to its backlog since the previous financial review call, driving a focus on prioritizing the most profitable PPAs, which should contribute to increased net margins.

- A robust supply chain strategy ensures AES can meet future project return targets and protect against tariff changes, potentially improving project execution, and leading to higher net margins.

- AES Indiana and AES Ohio are undergoing significant investment programs for grid reliability and data center growth, expected to lead to double-digit rate base growth through 2027, which should positively impact revenue and earnings.

- AES's plan to sell a 30% stake in AES Ohio to CDPQ should support further growth and enhance parent free cash flow for rent investments, thereby benefiting earnings stability and credit metrics.

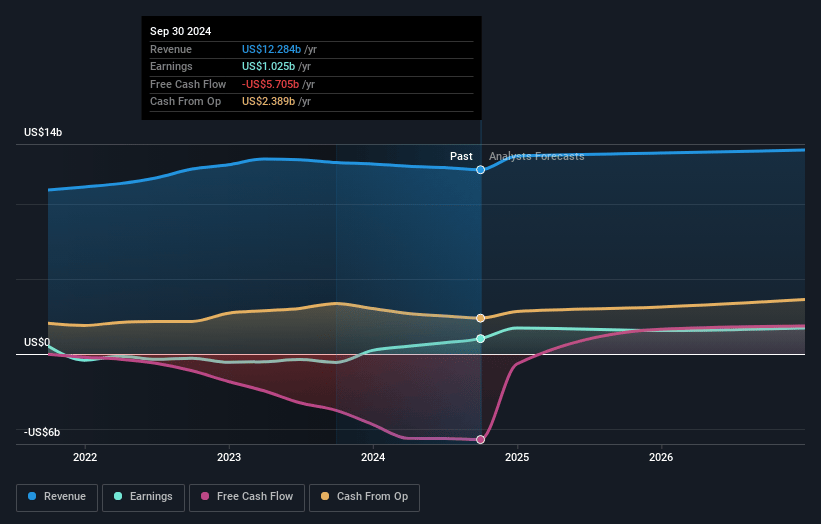

AES Future Earnings and Revenue Growth

Assumptions

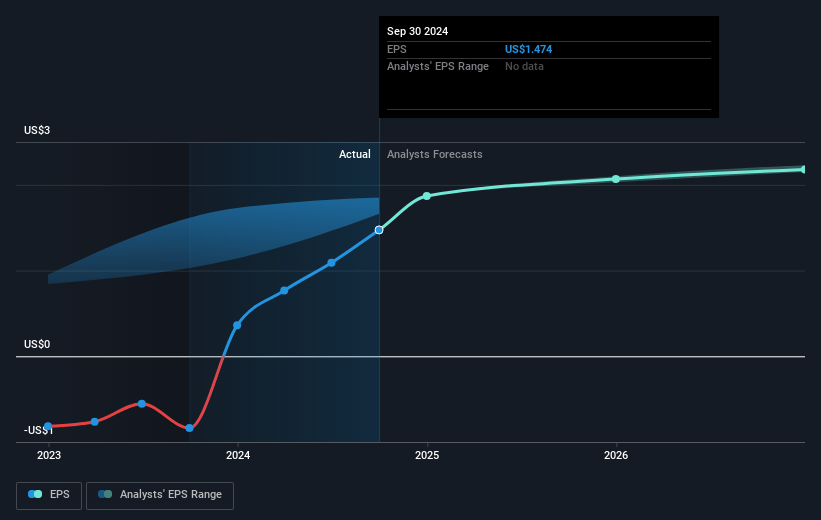

How have these above catalysts been quantified?- Analysts are assuming AES's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.3% today to 13.1% in 3 years time.

- Analysts expect earnings to reach $1.9 billion (and earnings per share of $2.31) by about November 2027, up from $1.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $2.2 billion in earnings, and the most bearish expecting $1.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.9x on those 2027 earnings, up from 10.8x today. This future PE is lower than the current PE for the US Renewable Energy industry at 25.6x.

- Analysts expect the number of shares outstanding to grow by 5.15% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 8.7%, as per the Simply Wall St company report.

AES Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Weather-related events, such as extreme weather in Colombia and drought conditions in South America, have negatively impacted AES's current year financial results, specifically affecting EBITDA and net margins.

- Execution risks in achieving their ambitious investment and growth targets can potentially lead to increased costs or delays, impacting future revenues and overall earnings.

- The closure of AES Brazil and the volatility seen in South American markets could lead to a reduction in diversification and exposure to growth markets, possibly affecting overall revenue stability.

- AES's reliance on significant capital expenditures and the need for substantial investments in renewable projects could strain financial resources if not managed properly, potentially impacting net margins.

- Potential regulatory and policy changes, such as tariff policies in the U.S. and the federal elections' outcome, may influence the financial viability of renewable energy projects, affecting future revenue streams and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $21.48 for AES based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $14.6 billion, earnings will come to $1.9 billion, and it would be trading on a PE ratio of 11.9x, assuming you use a discount rate of 8.7%.

- Given the current share price of $15.51, the analyst's price target of $21.48 is 27.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives