Key Takeaways

- Projected new port charges and potential U.S. trade wars could increase costs and disrupt revenue due to logistical challenges and reduced shipping volumes.

- Declining freight rates and overcapacity, coupled with uncertain geopolitical conditions, threaten to reduce earnings and strain cash flow despite fuel-efficient fleet upgrades.

- ZIM's focus on fuel-efficient fleets, cash flow, and partnerships boosts cost efficiency, shareholder value, and market competitiveness for potential growth.

Catalysts

About ZIM Integrated Shipping Services- Provides container shipping and related services in Israel and internationally.

- The projected imposition of a new port charge on Chinese-made vessels, if enacted, could increase operational costs significantly, affecting net margins as the company might have to undertake costly logistical adjustments or face higher port fees.

- The potential for a trade war and tariff increases between the U.S. and several key trading partners poses a risk of reduced shipping volumes and disrupted trade routes, potentially impacting revenue negatively as global trade patterns shift.

- An anticipated steep decline in freight rates, particularly if sustained, may lead to reduced revenues and decreased profitability, affecting earnings as the company faces a persisting overcapacity issue in the shipping market.

- Uncertain geopolitical and macroeconomic conditions, such as the unspecified timing of the Red Sea's reopening and U.S. tariff policy anxiety, could lead to volatile freight volumes and pricing, ultimately pressuring the company's earnings and profit margins.

- Despite recent fleet upgrades focusing on fuel efficiency, managing the balance between acquiring new capacity and flexibility with charter renewals under shifting market conditions could strain cash flow, impacting net margins and earnings due to potential inefficiencies in fleet utilization.

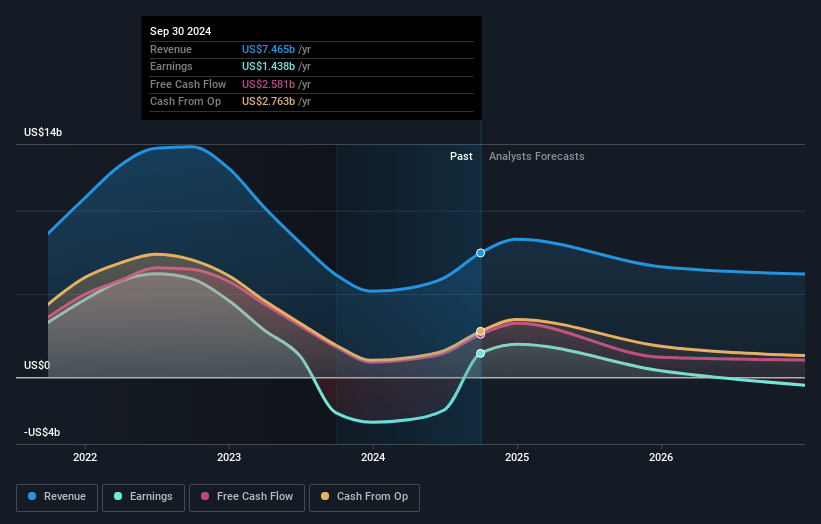

ZIM Integrated Shipping Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ZIM Integrated Shipping Services's revenue will decrease by 16.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 26.5% today to 0.8% in 3 years time.

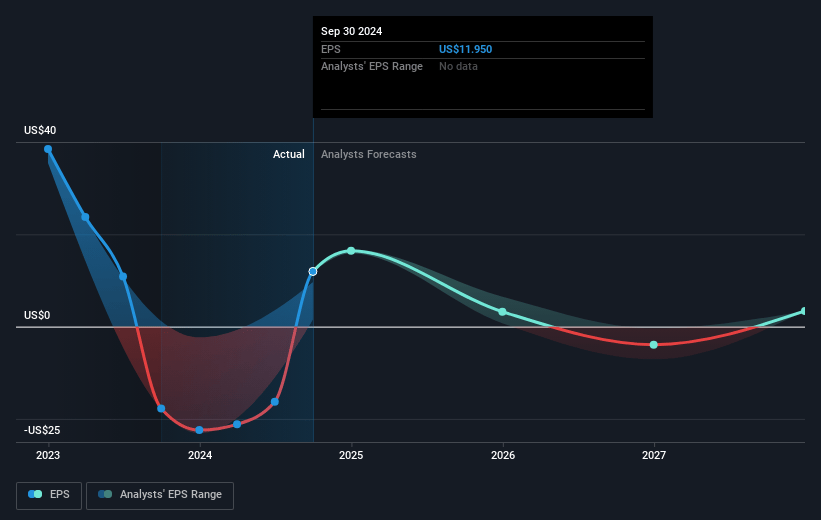

- Analysts expect earnings to reach $42.3 million (and earnings per share of $-2.72) by about July 2028, down from $2.4 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $397.0 million in earnings, and the most bearish expecting $-1.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 64.0x on those 2028 earnings, up from 0.8x today. This future PE is greater than the current PE for the US Shipping industry at 5.7x.

- Analysts expect the number of shares outstanding to grow by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.86%, as per the Simply Wall St company report.

ZIM Integrated Shipping Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- ZIM's strategic shift to investing in a modern, fuel-efficient, LNG-powered fleet positions the company to potentially improve cost efficiency and reduce operating expenses, positively impacting its profit margins.

- The company's operational success and significant volume growth, which exceeded market growth, suggest potential for continued revenue strength by leveraging its improved fleet and market presence.

- ZIM's ability to maintain a strong cash flow, coupled with a strategic commitment to dividend payouts, reflects financial stability and could support shareholder value, enhancing earnings performance.

- ZIM's strategic partnerships and agreements with major carriers like MSC may enhance its service offering and market reach, potentially boosting its revenue and market competitiveness.

- ZIM's investments in digital and technological enhancements, like smart containers, may improve operational efficiency and customer satisfaction, potentially supporting revenue growth and market differentiation.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $14.509 for ZIM Integrated Shipping Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $19.0, and the most bearish reporting a price target of just $9.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $5.1 billion, earnings will come to $42.3 million, and it would be trading on a PE ratio of 64.0x, assuming you use a discount rate of 15.9%.

- Given the current share price of $15.7, the analyst price target of $14.51 is 8.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.