Narratives are currently in beta

Key Takeaways

- Demand for high-speed data and RF infrastructure in AI applications is driving significant expected revenue and margin growth.

- Strategic investments in factory expansion and advanced products aim to triple revenue, enhancing operational efficiency and market reach.

- Tower Semiconductor faces potential revenue and margin impacts from market uncertainties, technological dependencies, and concentration risks, alongside significant capital expenditure pressures.

Catalysts

About Tower Semiconductor- An independent semiconductor foundry, focus on specialty process technologies to manufacture analog intensive mixed-signal semiconductor devices in Israel, the United States, Japan, Europe, and internationally.

- Tower Semiconductor's high-speed data center offerings are seeing increased demand, driven by unique offerings that fulfill AI requirements, which is likely to boost future revenue significantly.

- The company is expanding its RF infrastructure business, benefiting from optical transceiver demand used in high-speed data communication for AI, which could improve future revenue and net margins.

- Tower's advancements in silicon photonics, now shipping 800G products and ramping 1.6-terabit products, are expected to lead to over 3x revenue growth, positively impacting earnings.

- Investments in expanding factory capacity and capabilities, such as in Agrate and Albuquerque, along with a $350 million plan for SiPho and SiGe platform qualification, are expected to support continued revenue growth and operational efficiency.

- Growth in the power business, particularly with the ramp up of 300-millimeter 65-nanometer BCD platforms, is anticipated to drive revenue growth in consumer, industrial, and automotive markets.

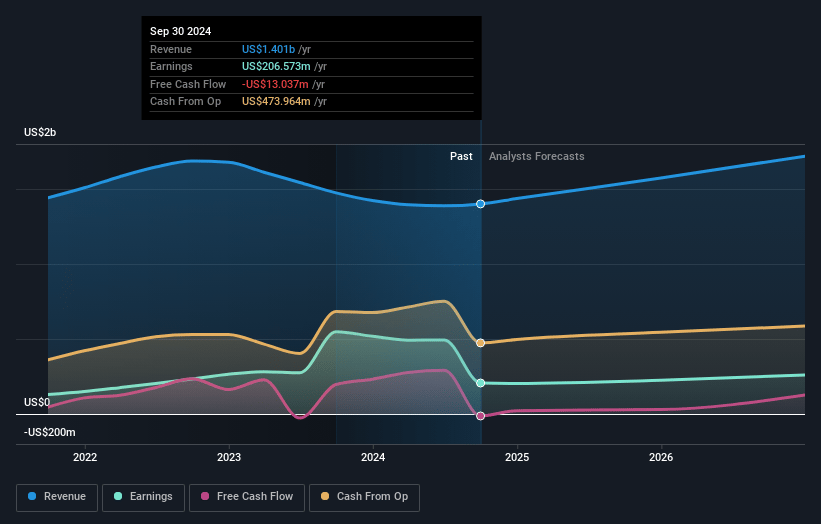

Tower Semiconductor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Tower Semiconductor's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.7% today to 15.1% in 3 years time.

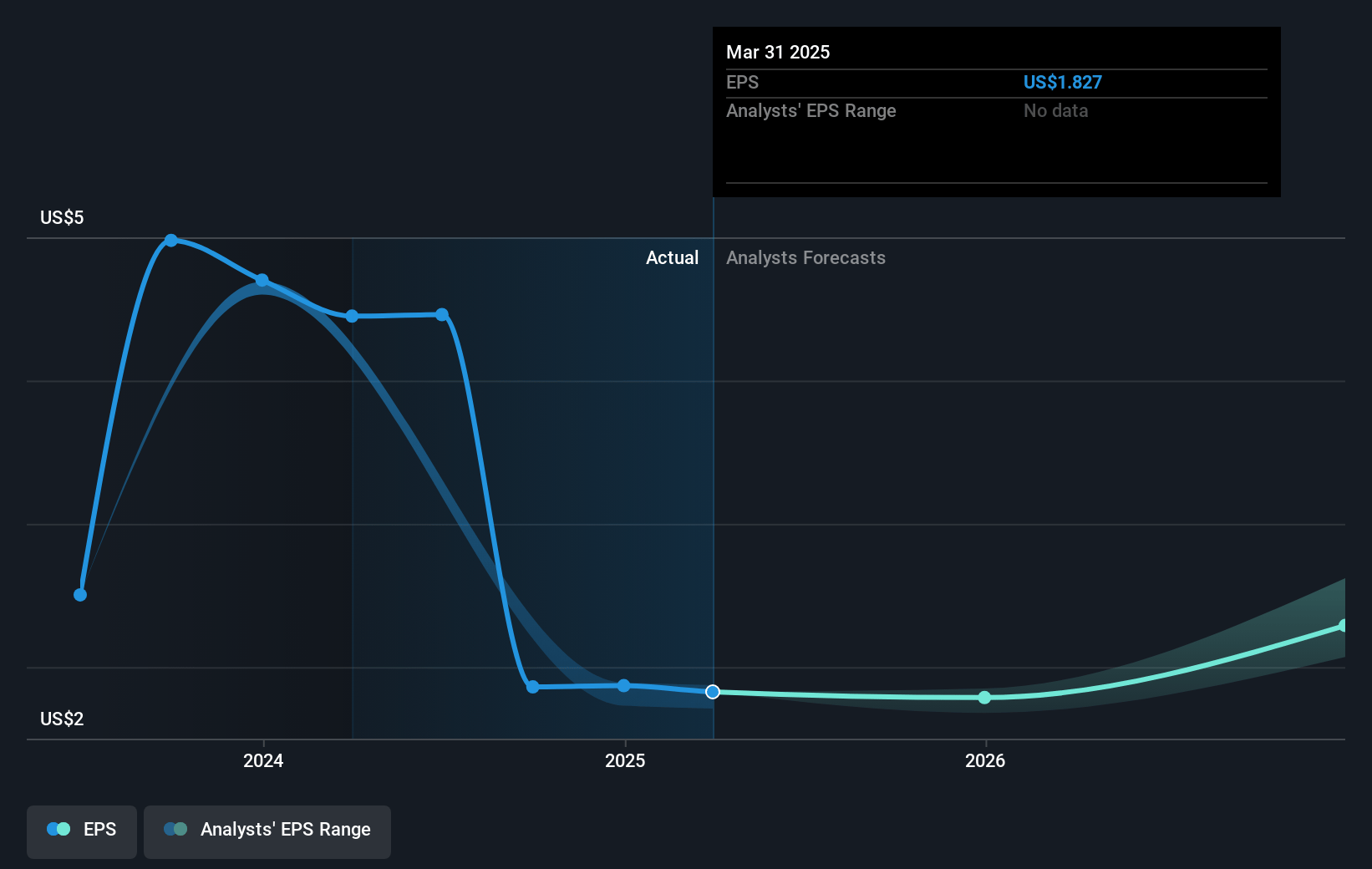

- Analysts expect earnings to reach $277.1 million (and earnings per share of $2.42) by about November 2027, up from $206.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 31.1x on those 2027 earnings, up from 25.2x today. This future PE is greater than the current PE for the US Semiconductor industry at 30.1x.

- Analysts expect the number of shares outstanding to grow by 0.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.56%, as per the Simply Wall St company report.

Tower Semiconductor Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Uncertainties and risk factors disclosed could impact future financial results, potentially affecting revenue and net margins.

- The silicon photonics and silicon germanium markets are subject to rapid technological changes, requiring ongoing innovation and investment; failure to keep up could impact future earnings.

- Utilization rates in key fabs are currently below capacity, indicating potential inefficiencies that could impact net margins and earnings if not addressed promptly.

- Dependence on a few key applications and customers for the silicon germanium and active copper cables business poses concentration risks, which could impact revenue stability if demand shifts.

- Capital expenditure plans, including substantial investments in capacity and technology, will require significant cash outlays that could pressure net margins and overall profitability if returns do not meet expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $57.5 for Tower Semiconductor based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $60.0, and the most bearish reporting a price target of just $50.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.8 billion, earnings will come to $277.1 million, and it would be trading on a PE ratio of 31.1x, assuming you use a discount rate of 9.6%.

- Given the current share price of $46.76, the analyst's price target of $57.5 is 18.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives