Key Takeaways

- Strategic AI-driven growth in Semiconductor Test and market share in custom VIP ASICs to enhance revenue, margins, and earnings.

- Partnerships and technology expansions aim to diversify revenue streams, drive complexity, and improve operating leverage and profitability.

- Teradyne faces challenges in Robotics and System Level Test units, with uncertainties in market recovery and risks in Industrial Automation affecting margins and growth projections.

Catalysts

About Teradyne- Designs, develops, manufactures, and sells automated test systems and robotics products in the United States, Asia Pacific, Europe, the Middle East, and Africa.

- Teradyne's focus on AI-driven growth in Semiconductor Test, particularly in SOC and memory markets, is expected to drive top-line growth as AI accelerators and AI Compute demand continue to rise, significantly impacting revenue.

- The company's strategic shift to capture market share in custom VIP (Vertically Integrated Producers) ASICs for Compute, with expectations of maintaining around a 50% share in a burgeoning market, is projected to enhance operating margins and earnings.

- Teradyne's partnership with Infineon to bolster its presence in power semiconductor testing, particularly in silicon carbide and gallium nitride devices for EV and renewable markets, is anticipated to diversify its revenue streams and strengthen net margins.

- Growth in System Level Test applications for AI and the expansion of 2-nanometer and gate-all-around process technology in mobile and automotive sectors are expected to drive complexity and unit demand, increasing Teradyne's market share and boosting EPS.

- The restructuring of the Robotics business to integrate UR and MiR operations aims to improve efficiency, reduce breakeven revenue, and set a foundation for long-term growth, positively impacting overall business operating leverage and profitability.

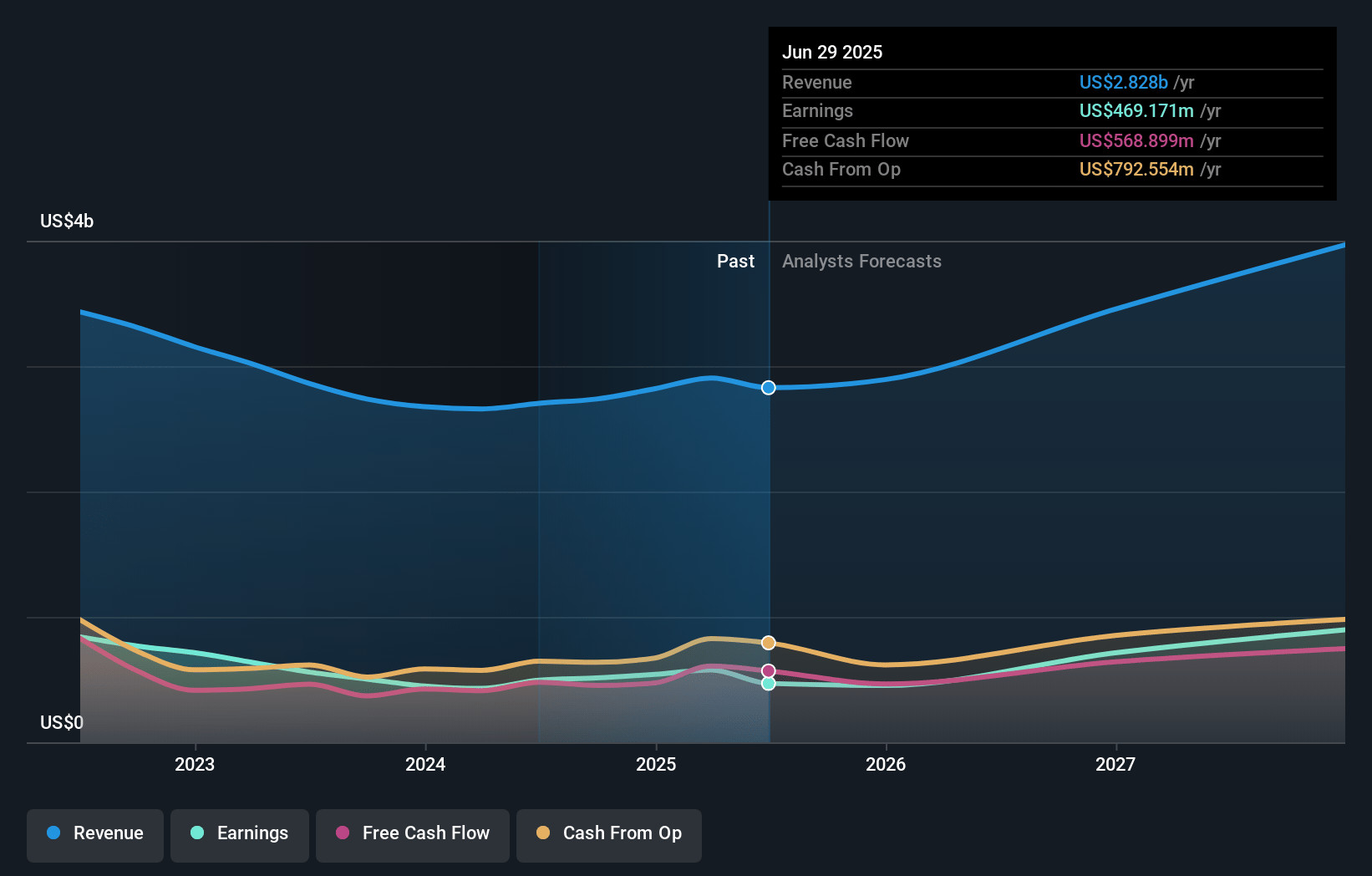

Teradyne Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Teradyne compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Teradyne's revenue will grow by 17.3% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 19.2% today to 24.4% in 3 years time.

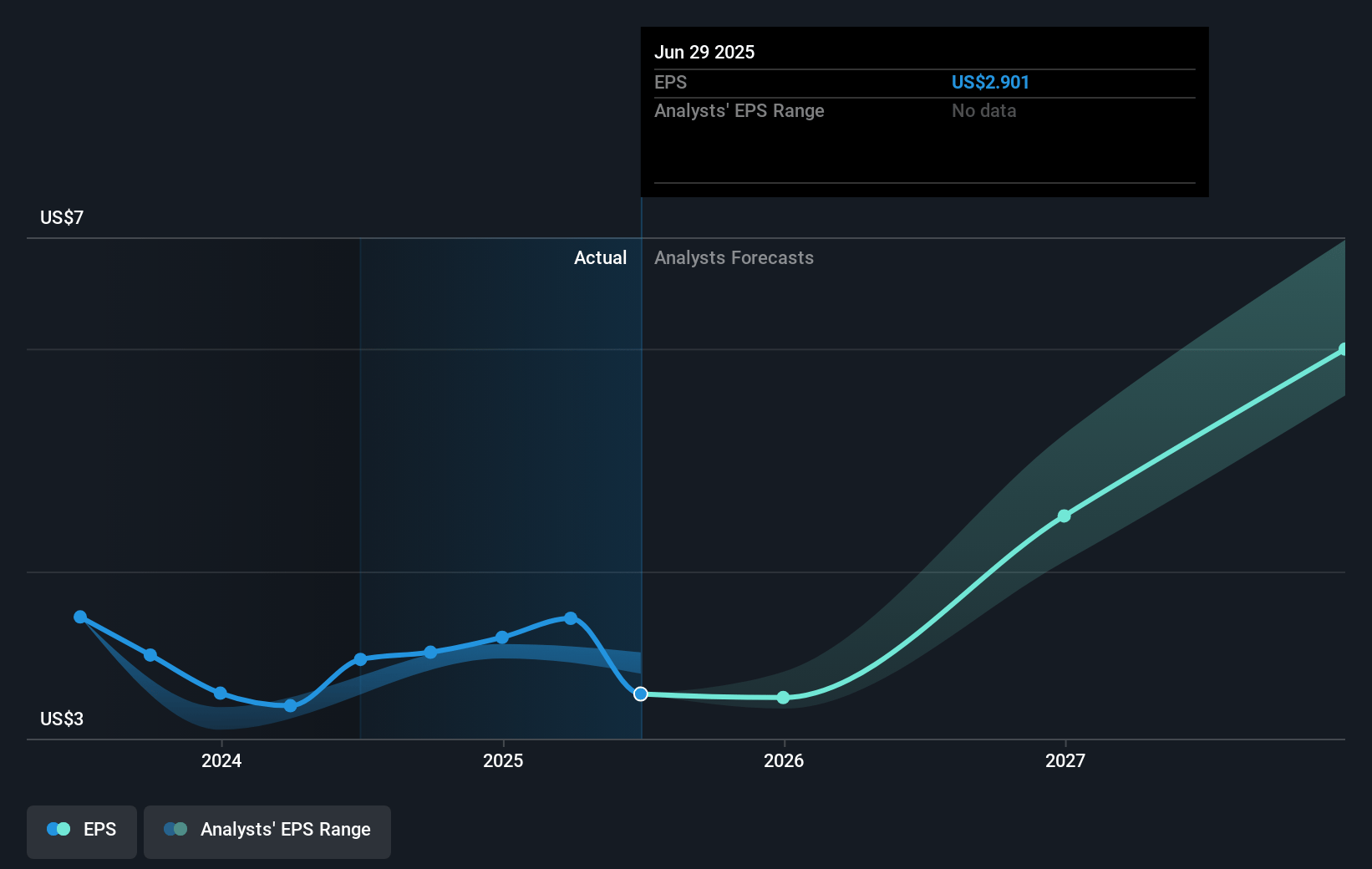

- The bullish analysts expect earnings to reach $1.1 billion (and earnings per share of $6.8) by about April 2028, up from $542.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 30.7x on those 2028 earnings, up from 21.1x today. This future PE is greater than the current PE for the US Semiconductor industry at 22.3x.

- Analysts expect the number of shares outstanding to grow by 3.59% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.82%, as per the Simply Wall St company report.

Teradyne Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Teradyne's Robotics segment has been struggling with underperformance and weak industrial spending, which has negatively impacted its margins and resulted in a 13% non-GAAP operating loss both in Q4 and the full year of 2024.

- The HBM part of the memory test market, though strong, is expected to soften in 2025 as customers absorb capacity with higher productivity tools, which could lead to stagnant market revenues.

- Weak conditions in the Industrial Automation market, which continue to affect Teradyne's Robotics business, present risks, particularly since visibility in this high-turns business is low.

- The integration of the System Level Test unit within the Semi Test business may not immediately yield the efficiency and performance expected, potentially impacting operating expenses and operating margins.

- Despite expectations of a recovery, there is uncertainty regarding the timing and scale of improvement in key markets like Mobile, Industrial, and Automotive, which could affect projected revenue growth and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Teradyne is $148.81, which represents two standard deviations above the consensus price target of $110.02. This valuation is based on what can be assumed as the expectations of Teradyne's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $155.0, and the most bearish reporting a price target of just $69.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $4.5 billion, earnings will come to $1.1 billion, and it would be trading on a PE ratio of 30.7x, assuming you use a discount rate of 8.8%.

- Given the current share price of $71.29, the bullish analyst price target of $148.81 is 52.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NasdaqGS:TER. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.