Key Takeaways

- Strategic pivot to high-growth sectors and premium products is aimed at improving revenue, net margins, and reducing variability.

- Operational efficiency and cost-reduction actions are targeting enhanced gross margins and earnings potential.

- Qorvo faces revenue declines in the Android 5G market, risks from customer dependence, rising competition, restructuring costs, and potential tax rate increases.

Catalysts

About Qorvo- Engages in development and commercialization of technologies and products for wireless, wired, and power markets worldwide.

- Qorvo is focusing on diversifying its business by investing in high growth areas like defense and aerospace, industrial and enterprise infrastructure, which are expected to drive double-digit revenue growth in these segments. This should lead to increased revenue and improve overall earnings.

- The company is emphasizing premium and flagship tier Android and 5G products, shifting focus from lower-margin mass tier products. This strategic focus is expected to improve net margins and reduce revenue variability in the long term.

- Ongoing investments in ultra-wideband, WiFi 7, power management, and automotive solutions, including design wins in new vehicle launches, are expected to drive future revenue growth across various market segments.

- Qorvo is optimizing its operational efficiency with measures like workforce reduction and relocating production to maximize its cost structure, potentially boosting gross margins by approximately 150 basis points in fiscal 2026.

- Actions taken to reduce capital intensity and product costs, such as process technology advancements and leveraging outsourced manufacturing partnerships, are expected to support high-40% gross margins in strong quarters, further bolstering earnings potential.

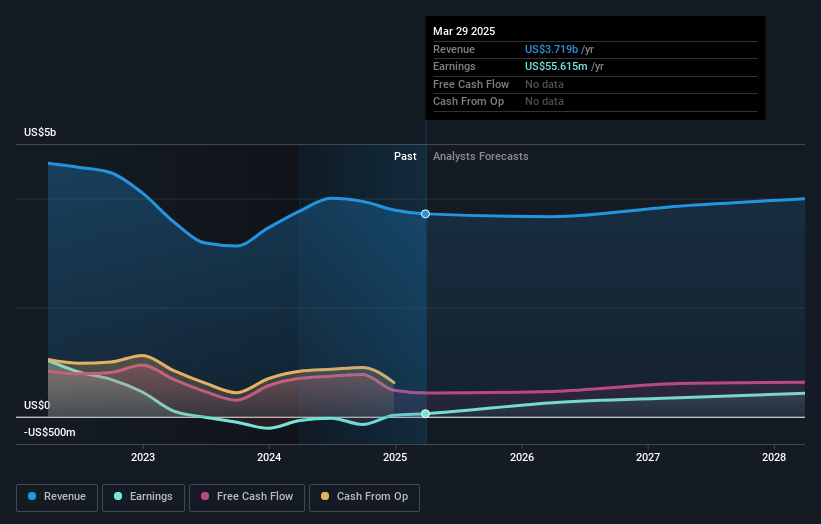

Qorvo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Qorvo's revenue will grow by 2.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.7% today to 12.3% in 3 years time.

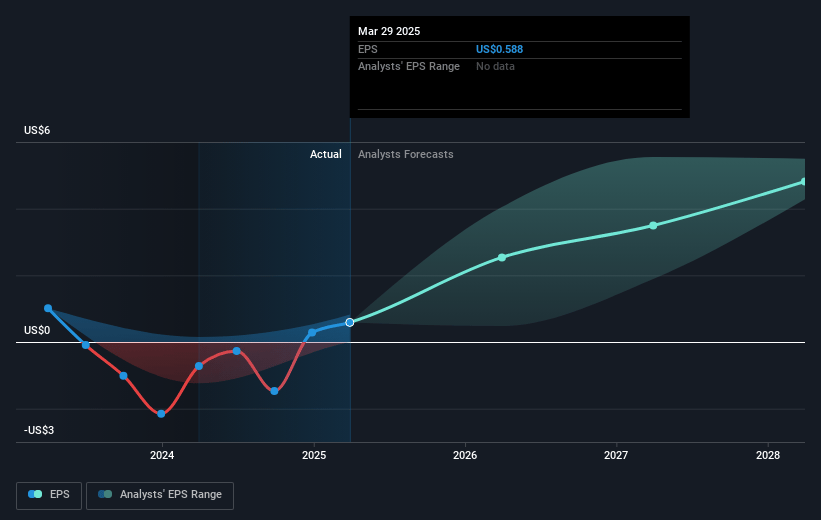

- Analysts expect earnings to reach $501.3 million (and earnings per share of $5.25) by about April 2028, up from $27.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $559.1 million in earnings, and the most bearish expecting $268.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.9x on those 2028 earnings, down from 220.7x today. This future PE is lower than the current PE for the US Semiconductor industry at 24.2x.

- Analysts expect the number of shares outstanding to decline by 2.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.75%, as per the Simply Wall St company report.

Qorvo Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Qorvo is experiencing a significant decline in its mass tier Android 5G market, expecting a revenue drop of approximately $150 million to $200 million annually, impacting overall revenue and profitability.

- The company's dependence on their largest customer, which represented over 50% of revenue in the December quarter, poses a risk if any changes in the customer's product cycles or order volumes occur, potentially impacting revenue consistency.

- The Android 5G segment is expected to be down with aggressive competition and market shifts towards entry-tier devices, leading to uncertainty in revenue forecasting and pressure on net margins.

- Qorvo's restructuring efforts, including workforce reductions, may incur initial costs and impact operational efficiency, affecting net margins and earnings in the near term.

- Changes in tax regulations could raise Qorvo's tax rate from approximately 11% to between 18% and 19% in fiscal 2026, adversely affecting net income and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $86.678 for Qorvo based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $128.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.1 billion, earnings will come to $501.3 million, and it would be trading on a PE ratio of 19.9x, assuming you use a discount rate of 9.7%.

- Given the current share price of $63.78, the analyst price target of $86.68 is 26.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.