Key Takeaways

- CEVA's strength in wireless communication IP, especially in newer WiFi standards, and strategic partnerships drive anticipated revenue and market leadership.

- Expansion into automotive markets and diversified royalty streams promise long-term revenue stability and improved net margins.

- Revenue and growth concerns arise from sluggish smartphone shipments, economic challenges, competitive AI pressures, geopolitical risks, and slow Wi-Fi 7 adoption.

Catalysts

About CEVA- Provides silicon and software intellectual property (IP) solutions to semiconductor and original equipment manufacturer companies in the United States, Europe, the Middle East, the Asia Pacific, and internationally.

- CEVA's strategic partnerships and design wins in Bluetooth, WiFi 6, and especially the newer WiFi 7 demonstrate strong market leadership in wireless communication IP, which is poised to drive future revenue growth as customers upgrade to higher ASP products.

- The expansion into the automotive market, particularly with the ADAS win involving high-performance AI and edge AI technologies like NeuPro-M NPU, indicates a strong potential for increased earnings from new verticals, as these advanced systems become more prevalent.

- The diversification and deepening of the royalty customer base, particularly with the first royalty report from a U.S. OEM using CEVA's technology in their 5G models, suggest a promising long-term royalty stream and increased market share in wireless communication IP, positively impacting net margins and revenue stability.

- Strong growth in WiFi royalties, driven by a shift to higher-margin WiFi 6 shipments, signals a favorable product mix transition, which will enhance net margins as the market continues to adopt newer technology standards.

- CEVA's prudent cost control measures and strategic focus on licensing, alongside anticipated growth from existing design engagements and new customer segments, are expected to improve operating income and non-GAAP EPS, even in a cautious revenue growth environment.

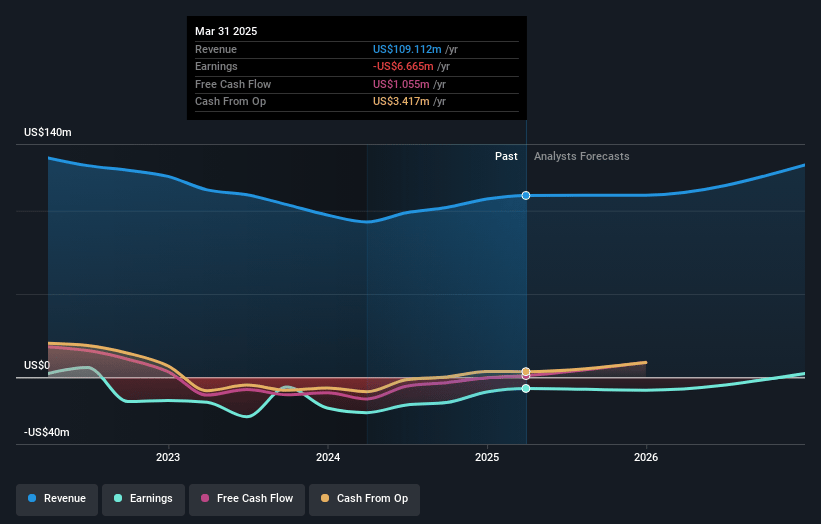

CEVA Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CEVA's revenue will grow by 7.7% annually over the next 3 years.

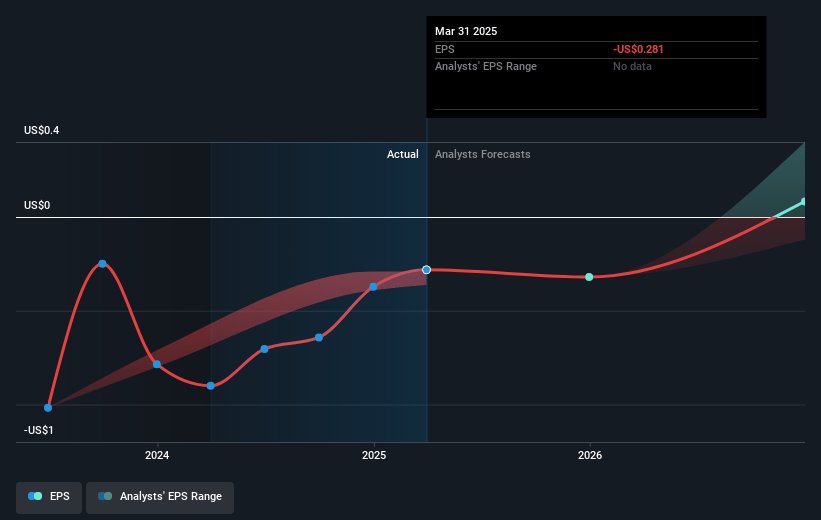

- Analysts are not forecasting that CEVA will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate CEVA's profit margin will increase from -6.1% to the average US Semiconductor industry of 12.9% in 3 years.

- If CEVA's profit margin were to converge on the industry average, you could expect earnings to reach $17.5 million (and earnings per share of $0.73) by about May 2028, up from $-6.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 56.6x on those 2028 earnings, up from -79.6x today. This future PE is greater than the current PE for the US Semiconductor industry at 25.0x.

- Analysts expect the number of shares outstanding to grow by 1.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.1%, as per the Simply Wall St company report.

CEVA Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Soft low-cost smartphone shipments and a slower-than-expected product ramp-up from an industrial customer negatively impacted CEVA's royalty revenue, indicating potential issues in revenue stability and growth.

- The company's decision to lower 2025 revenue guidance from high single-digit to low single-digit growth reflects concerns about the global macroeconomic environment and consumer demand, posing a risk to future revenue projections.

- There is a potential risk from the competitive landscape in AI NPUs, with the need for CEVA to continuously innovate and maintain its technology leadership to secure and expand its royalty base, which could affect future earnings.

- Tariff and geopolitical uncertainties could indirectly impact CEVA's customer demand and overall market conditions, potentially affecting revenue generation.

- The transition to Wi-Fi 7, although promising, may take time to reach higher volume shipments, potentially delaying anticipated revenue from royalties associated with this technology upgrade.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $31.833 for CEVA based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $21.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $136.2 million, earnings will come to $17.5 million, and it would be trading on a PE ratio of 56.6x, assuming you use a discount rate of 9.1%.

- Given the current share price of $22.17, the analyst price target of $31.83 is 30.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.