Narratives are currently in beta

Key Takeaways

- Demand for Camtek's HPC systems and new Eagle system orders suggests potential revenue and earnings growth driven by generative AI trends and market alignment.

- Manufacturing expansion and product diversification into advanced packaging and sensors indicate prepared capacity for growth beyond the HPC market.

- Camtek faces revenue risks from reliance on HPC and Asian markets, pressure from operating expenses, overcapacity in HBM, and competitive limits on pricing power.

Catalysts

About Camtek- Develops, manufactures, and sells inspection and metrology equipment for semiconductor industry.

- The demand for Camtek's systems for HPC-related products is expected to continue into 2025 due to its role as a key equipment provider for generative AI, potentially boosting future revenues significantly.

- Camtek is introducing its fifth generation Eagle system, which offers enhanced capabilities and has already secured over $20 million in orders. This innovation is likely to impact future earnings positively as it aligns with new market demands.

- The company's expansion of manufacturing capacity in Europe, starting in 2025, indicates preparedness to meet increased demand, which could lead to sustained revenue growth in the coming years.

- Camtek's product diversification, including inspection solutions for advanced packaging and increased demand from CMOS image sensors and silicon carbide segments, suggests potential for revenue growth beyond the HPC market.

- The release of technological bottlenecks, such as the anticipated alleviation of 2.5D substrate constraints, could enhance Camtek’s margin performance by optimizing production capacity and processes in the near future.

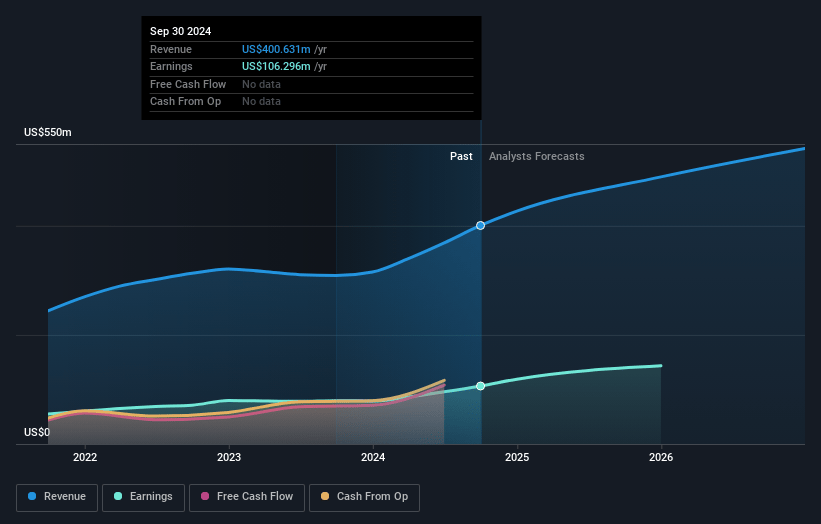

Camtek Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Camtek's revenue will grow by 15.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 26.5% today to 34.7% in 3 years time.

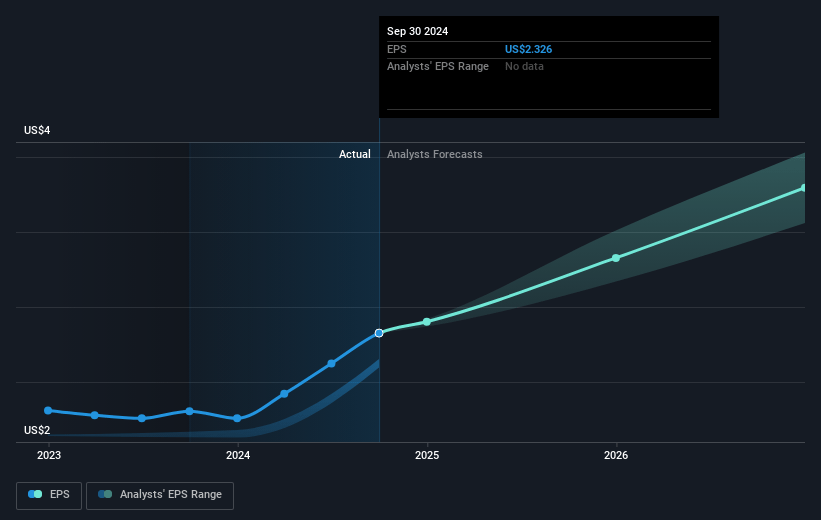

- Analysts expect earnings to reach $211.7 million (and earnings per share of $3.74) by about November 2027, up from $106.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 38.0x on those 2027 earnings, up from 32.0x today. This future PE is greater than the current PE for the US Semiconductor industry at 30.1x.

- Analysts expect the number of shares outstanding to grow by 7.68% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.64%, as per the Simply Wall St company report.

Camtek Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Camtek's reliance on the HPC (high-performance computing) market, which constitutes a large portion of its revenue, may pose a risk if demand in this segment slows due to production capacity bottlenecks, potentially impacting revenue projections for the coming years.

- The company's significant revenue dependence on the Asian market, particularly China, which accounts for a substantial portion of revenue, could be a risk due to geopolitical tensions or changes in trade policies, potentially affecting future revenue and growth.

- Increasing operating expenses, driven by planned expansions and investment in new product development, may pressure net margins if revenue growth does not meet expectations or if new product launches do not perform as anticipated.

- Potential overcapacity concerns in the HBM (high-bandwidth memory) segment, which is crucial for Camtek's growth, could lead to fluctuations in customer orders and affect the company's revenue stability and growth projections.

- While new product offerings like the Eagle G5 aim to capture additional market share, the competitive landscape in semiconductor inspection and metrology could limit pricing power and profitability, thereby impacting earnings and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $109.0 for Camtek based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $140.0, and the most bearish reporting a price target of just $95.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $610.5 million, earnings will come to $211.7 million, and it would be trading on a PE ratio of 38.0x, assuming you use a discount rate of 9.6%.

- Given the current share price of $74.84, the analyst's price target of $109.0 is 31.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives