Key Takeaways

- Strategic localization in China aims to reduce costs and improve margins, though transitional period may temporarily impact fiscal margins.

- Record new product introductions in high-growth sectors target revenue growth, but gains may be slower than expected due to transitional challenges.

- Declines in automotive sales and industrial demand, combined with margin pressures, may challenge Allegro MicroSystems' revenue and profitability recovery.

Catalysts

About Allegro MicroSystems- Designs, develops, manufactures, and markets sensor integrated circuits (ICs) and application-specific analog power ICs for motion control and energy-efficient systems.

- Allegro MicroSystems is investing in localizing their supply chain in China, which is expected to lead to cost reductions and improve margins over time, although fiscal year 2025 margins might be temporarily impacted due to transitional costs.

- The company is introducing a record number of new products, particularly in their magnetic sensing and power IC portfolios. These innovations, which cater to high-growth areas like hybrid vehicles and electric vehicles, could drive revenue growth in the coming years, albeit potentially slower than consensus forecasts.

- Allegro is focusing on a strategic shift to increase design wins with top OEMs, which is expected to generate long-term revenue growth. However, the full impact may take time to materialize due to the typical multi-year automotive product lifecycle.

- The company is experiencing an increase in within-quarter orders and a decrease in cancellations, suggesting potential future revenue stabilization. However, inventory digestion issues in certain markets might dampen immediate earnings and net margin expectations.

- Allegro's initiatives to reduce operating expenses and optimize their cost structure, including repricing their term loan and making voluntary debt payments, are projected to enhance cash flow and profitability moving forward, though immediate financial benefits might not reflect in current fiscal projections.

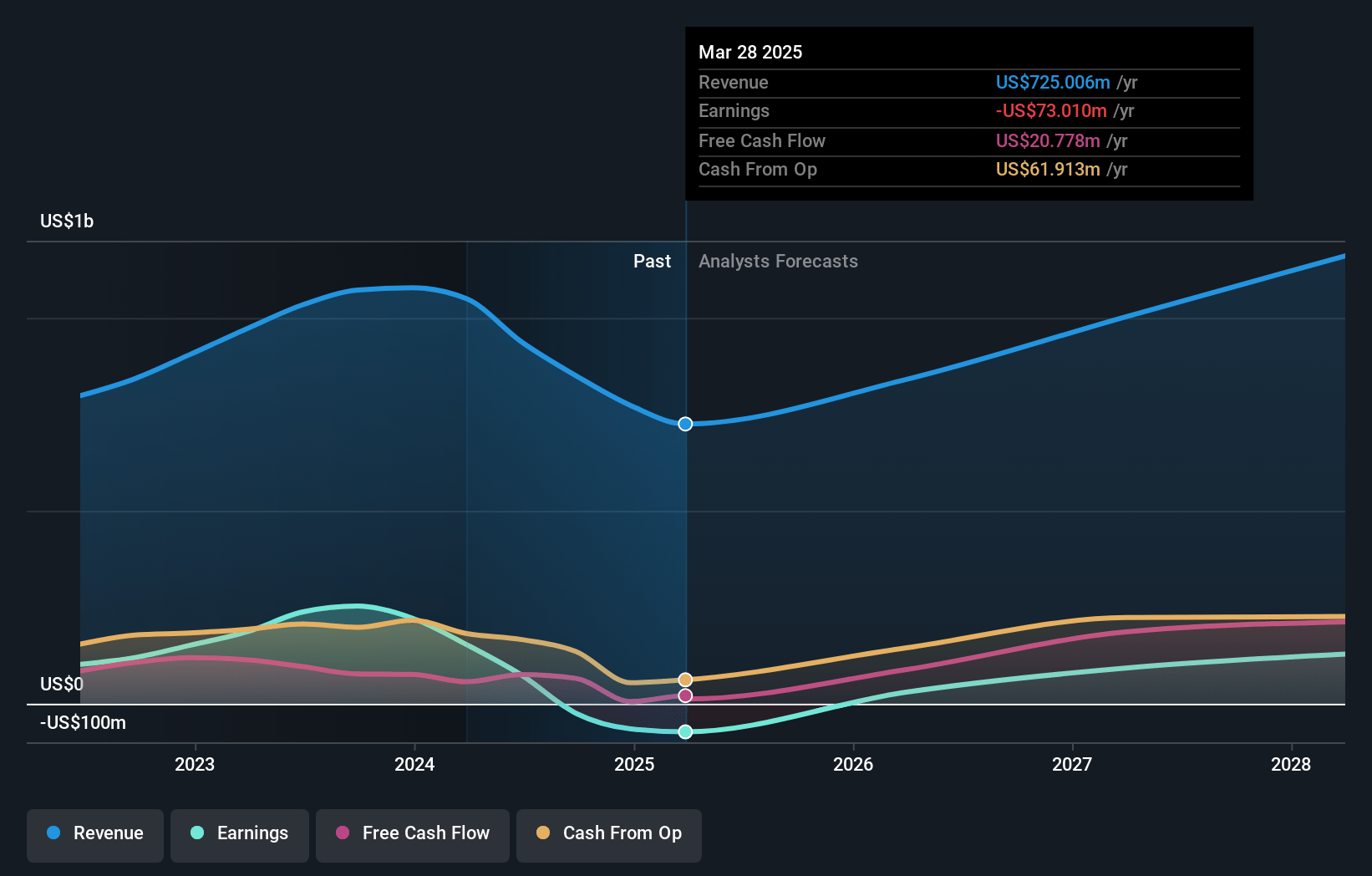

Allegro MicroSystems Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Allegro MicroSystems compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Allegro MicroSystems's revenue will grow by 11.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -8.5% today to 12.7% in 3 years time.

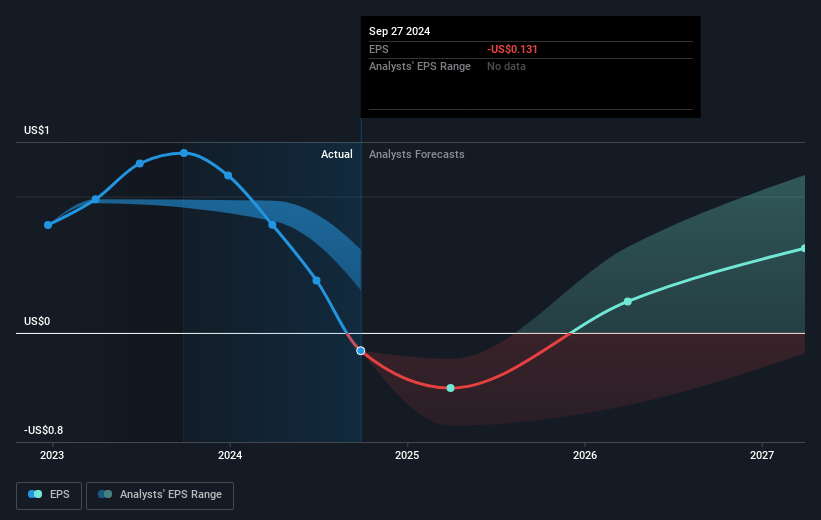

- The bearish analysts expect earnings to reach $133.6 million (and earnings per share of $0.7) by about April 2028, up from $-65.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 37.7x on those 2028 earnings, up from -54.2x today. This future PE is greater than the current PE for the US Semiconductor industry at 24.2x.

- Analysts expect the number of shares outstanding to decline by 4.97% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.23%, as per the Simply Wall St company report.

Allegro MicroSystems Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company experienced a 30% year-over-year decline in sales for Q3, which could signal underlying issues with demand that might continue to impact revenue.

- Despite growth in specific industrial sectors like data centers and medical, general industrial demand remains soft, and any lingering challenges, such as macroeconomic conditions, could further impact revenue.

- Allegro's automotive sales, which account for a significant portion of their revenue, declined 33% year-over-year, and any further inventory management issues could continue to suppress earnings.

- The expectation of a 4% increase in sales in the next quarter may not be enough to offset the significant declines in previous quarters, potentially impacting overall profitability.

- The company anticipates a gross margin headwind of approximately 200 basis points in the fourth quarter owing to pricing agreements and inventory adjustments, which could negatively impact net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Allegro MicroSystems is $24.49, which represents one standard deviation below the consensus price target of $28.25. This valuation is based on what can be assumed as the expectations of Allegro MicroSystems's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $35.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $1.1 billion, earnings will come to $133.6 million, and it would be trading on a PE ratio of 37.7x, assuming you use a discount rate of 9.2%.

- Given the current share price of $19.23, the bearish analyst price target of $24.49 is 21.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:ALGM. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.