Key Takeaways

- Upbranding and renovations at key properties are expected to enhance revenue, occupancy, and competitive positioning, driving EBITDA growth.

- Improved group bookings and corporate travel demand hint at rising revenues and net income, supported by efficient expense management and favorable market conditions.

- Pressure on margins and moderated leisure demand, coupled with competition and investment uncertainties, pose risks to revenue growth and financial performance.

Catalysts

About Xenia Hotels & Resorts- A self-advised and self-administered REIT that invests in uniquely positioned luxury and upper upscale hotels and resorts with a focus on the top 25 lodging markets as well as key leisure destinations in the United States.

- The completion of the transformational renovation and upbranding of Grand Hyatt Scottsdale is expected to drive significantly higher cash flow and contribute positively to RevPAR and occupancy, enhancing revenue and earnings growth.

- The strengthened group booking pace, with group room revenues and occupancy on the rise, indicates potential for increased revenue and net income as group demand is expected to boost hotel stays and rates.

- The continuous improvement in corporate transient demand, particularly midweek, suggests room for growth in revenues as business travel, which currently lags 2019 levels, picks up, indicating future earnings potential.

- CapEx projects completed in 2024, such as renovations in Orlando, Salt Lake City, and Santa Barbara, along with new developments like the ballroom at Hyatt Regency Grand Cypress, are projected to enhance competitive positioning and drive future revenue and EBITDA growth.

- The favorable supply backdrop and ongoing efforts to manage expenses, as well as the completion of past years' investments, suggest potential for superior earnings growth beyond 2025, impacting future margins and FFO positively.

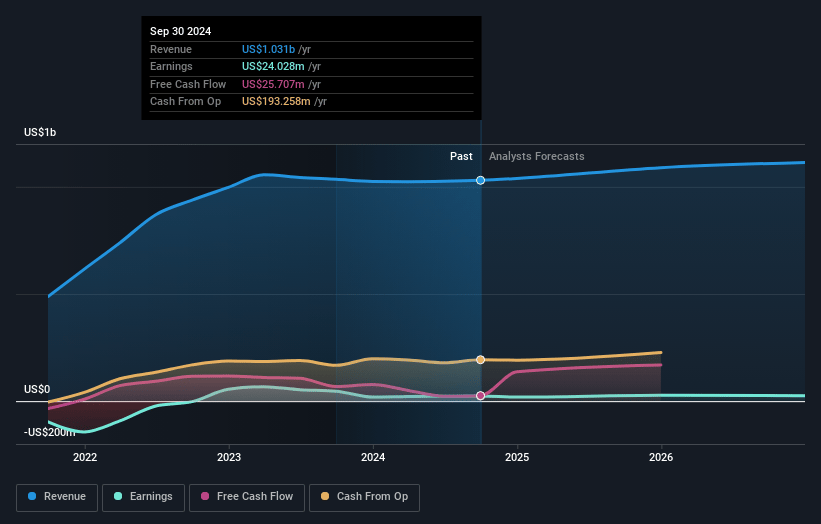

Xenia Hotels & Resorts Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Xenia Hotels & Resorts's revenue will grow by 3.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.5% today to 3.1% in 3 years time.

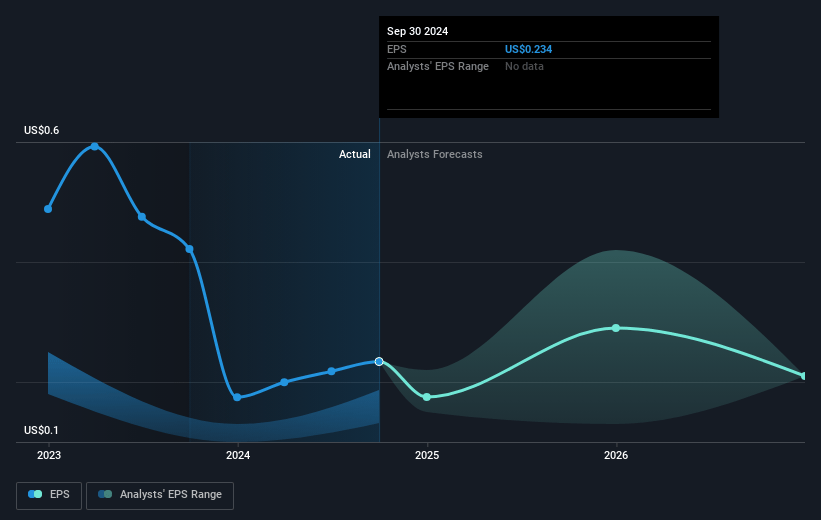

- Analysts expect earnings to reach $35.5 million (and earnings per share of $0.35) by about May 2028, up from $15.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 46.4x on those 2028 earnings, down from 68.3x today. This future PE is greater than the current PE for the US Hotel and Resort REITs industry at 19.1x.

- Analysts expect the number of shares outstanding to decline by 0.6% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.69%, as per the Simply Wall St company report.

Xenia Hotels & Resorts Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Margins faced pressure due to labor costs and increased sales and marketing expenses, which could impact net margins.

- Leisure demand has moderated and continues to soft, particularly affecting RevPAR in key markets like Savannah, Phoenix, and Napa, which could hurt revenues.

- The ongoing transition and intense competition in the leisure-focused markets could hinder revenue growth and stabilization, impacting earnings.

- Dependency on group and transient corporate demand recovery might pose risks if macroeconomic conditions worsen, potentially affecting future revenues.

- Uncertainty in executing investments and capital projects, with higher near-term capital expenditures, could impact earnings and overall financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $12.333 for Xenia Hotels & Resorts based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $16.0, and the most bearish reporting a price target of just $9.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.1 billion, earnings will come to $35.5 million, and it would be trading on a PE ratio of 46.4x, assuming you use a discount rate of 8.7%.

- Given the current share price of $10.62, the analyst price target of $12.33 is 13.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.