Key Takeaways

- Strategic investments in the TimberStrand facility and natural climate solutions are set to enhance operational efficiencies and boost earnings.

- Growth in housing demand and strategic acquisitions aim to bolster long-term revenue and sustainable cash flow.

- Weyerhaeuser faces risks from elevated inventories and market headwinds, impacting revenue, margins, and profitability amidst challenging market conditions and potential tariffs.

Catalysts

About Weyerhaeuser- Weyerhaeuser Company, one of the world's largest private owners of timberlands, began operations in 1900.

- The planned investment of approximately $500 million in a new TimberStrand facility in Arkansas is expected to double Weyerhaeuser's TimberStrand offering and increase total company EWP capacity by 24%. This expansion is anticipated to generate over $100 million of annual adjusted EBITDA, positively impacting revenue and earnings.

- The development of the Natural Climate Solutions business, with significant contributions expected from Forest Carbon credits and renewables such as large-scale solar and wind projects, is projected to reach $100 million of adjusted EBITDA by the end of 2025. This growth is likely to enhance net margins and overall earnings.

- The integration benefits from the new TimberStrand facility, leveraging Weyerhaeuser's existing Timberlands, are anticipated to create operational efficiencies and cost synergies, further improving net margins and earnings.

- The company’s strategic acquisitions, such as increasing its Timberlands in Alabama, aim to enhance its sustainable cash flow generation and long-term revenue growth.

- There is expected growth in housing demand and potential improvement in repair and remodel activities in 2025, driven by demographic trends and an underbuilt housing stock. This is likely to increase demand for Weyerhaeuser’s products, boosting revenue.

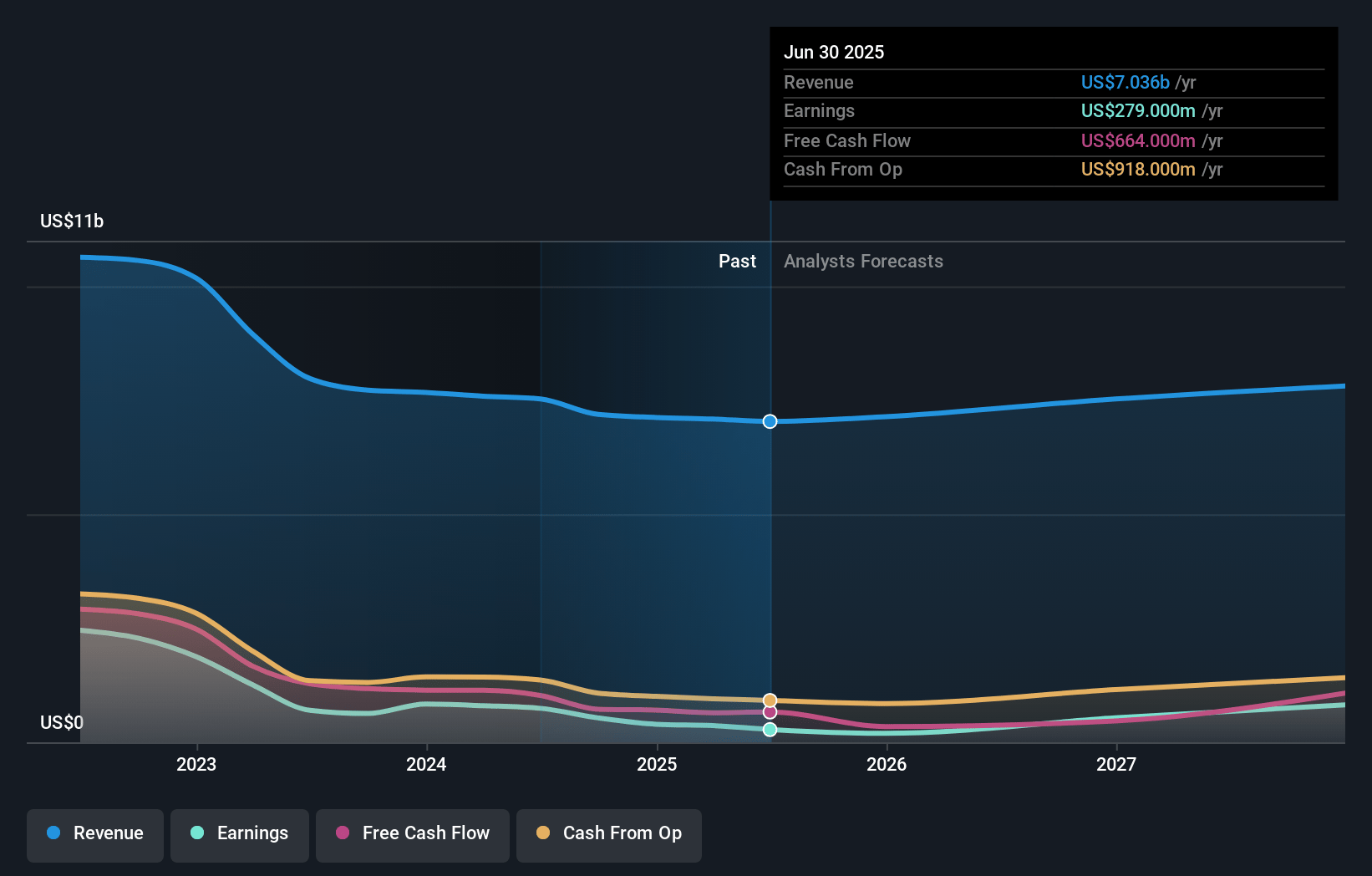

Weyerhaeuser Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Weyerhaeuser's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.6% today to 12.0% in 3 years time.

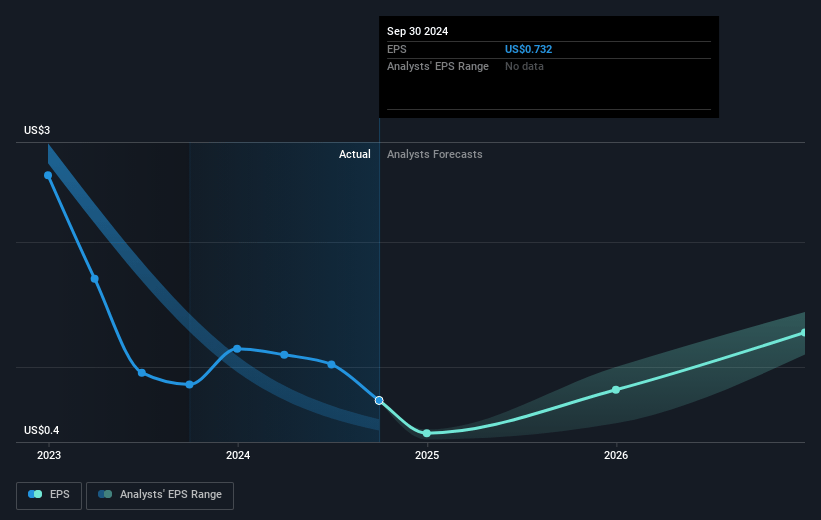

- Analysts expect earnings to reach $965.3 million (and earnings per share of $1.34) by about March 2028, up from $396.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $825.2 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.2x on those 2028 earnings, down from 56.2x today. This future PE is greater than the current PE for the US Specialized REITs industry at 29.4x.

- Analysts expect the number of shares outstanding to decline by 0.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.54%, as per the Simply Wall St company report.

Weyerhaeuser Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Weyerhaeuser faces ongoing consumption headwinds in the Japanese log market and elevated inventories, which could impact export sales volumes and average realizations, adversely affecting revenue.

- In the North American OSB market, despite demand resilience, elevated channel inventories and seasonal slowdowns present risks that could pressure pricing and margins.

- Variable compensation expenses and higher intersegment charges impacted unallocated segment results, potentially straining net margins if such costs persist.

- Lumber and OSB benchmark pricing faced moderation and potential instability due to inventory swings, supply constraints, and potential tariffs, which could negatively affect profitability.

- The financial flexibility to continue share repurchases while maintaining debt levels amidst challenging market conditions may limit net margins and overall cash flow adaptability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $36.0 for Weyerhaeuser based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $33.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $8.1 billion, earnings will come to $965.3 million, and it would be trading on a PE ratio of 32.2x, assuming you use a discount rate of 6.5%.

- Given the current share price of $30.65, the analyst price target of $36.0 is 14.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives