Key Takeaways

- Strategic acquisitions and property transformations are anticipated to enhance revenue and earnings through increased group business and improved brand alignment.

- Capital recycling and share repurchases should boost EPS and returns on invested capital, supporting future revenue and margin growth.

- Rising labor costs and delayed projects, coupled with interest cost increases, threaten revenue growth and profitability for Sunstone Hotel Investors.

Catalysts

About Sunstone Hotel Investors- A lodging real estate investment trust ("REIT") that as of the date of this release owns 15 hotels comprised of 7,255 rooms, the majority of which are operated under nationally recognized brands.

- The recent acquisition of the Hyatt Regency San Antonio Riverwalk, with its strategic location and planned meeting space upgrades, is expected to capitalize on increased group business and retail lease revenue opportunities, enhancing future revenue and earnings growth.

- The transformation and ramp-up of properties such as the Andaz Miami Beach and Marriott Long Beach Downtown are set to contribute significantly to future earnings, as they complete their refurbishments and benefit from improved brand alignment, leading to higher RevPAR and margins.

- Successful capital recycling, like the sale of the Boston Park Plaza and strategic repositioning of proceeds, should lead to enhanced returns on invested capital, supporting net margins and revenue growth in the future.

- The potential for continued share repurchases at discounts to NAV and a sustained dividend strategy are expected to drive EPS growth by reducing the share count and returning capital to shareholders.

- Strength in group bookings and corporate travel across key urban markets, along with initiatives to improve cost management and operational efficiencies, provides a compelling setup for revenue and margin expansion in 2025, especially with reduced disruption from capital projects compared to prior years.

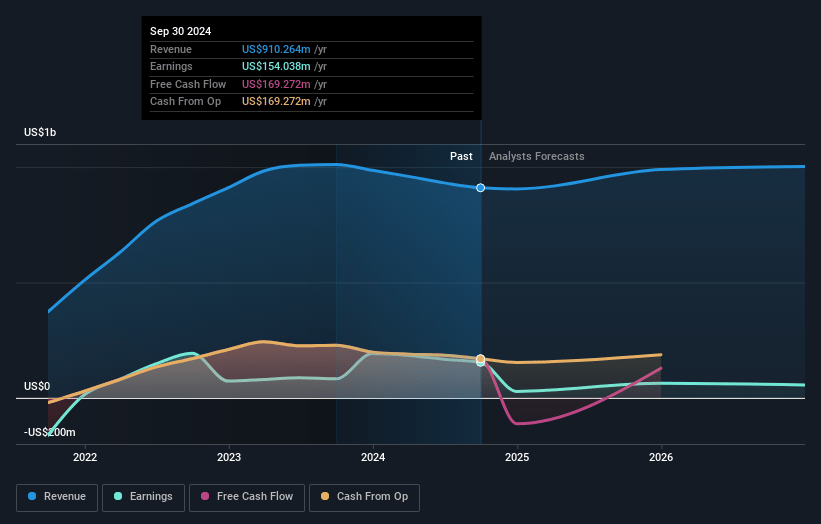

Sunstone Hotel Investors Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Sunstone Hotel Investors's revenue will grow by 6.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.1% today to 8.0% in 3 years time.

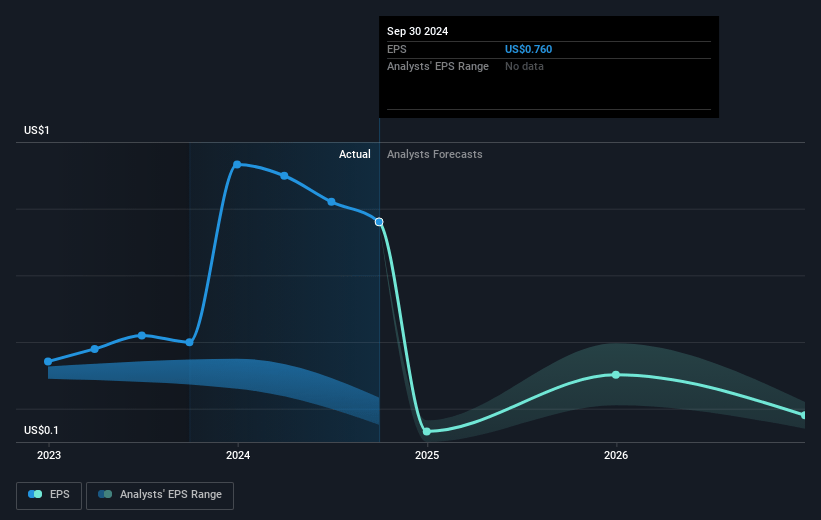

- Analysts expect earnings to reach $87.9 million (and earnings per share of $0.34) by about March 2028, up from $27.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 31.3x on those 2028 earnings, down from 69.9x today. This future PE is greater than the current PE for the US Hotel and Resort REITs industry at 24.5x.

- Analysts expect the number of shares outstanding to decline by 1.3% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.76%, as per the Simply Wall St company report.

Sunstone Hotel Investors Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The lingering effects of labor strikes in San Diego could continue to disrupt group and transient business, potentially impacting revenue and profit margins.

- Rising wage and benefit costs, particularly due to collective bargaining agreements, could inflate operating expenses and compress net margins.

- The challenges in the permitting and approval process in Miami have delayed the opening of the Andaz Miami Beach, affecting projected earnings growth from this investment.

- The potential for slower-than-expected recovery in leisure travel, particularly in Maui, could dampen anticipated revenue growth.

- Increased interest costs due to refinancing activities and the reduction of interest income from cash balances could negatively affect net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $11.375 for Sunstone Hotel Investors based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $12.0, and the most bearish reporting a price target of just $10.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.1 billion, earnings will come to $87.9 million, and it would be trading on a PE ratio of 31.3x, assuming you use a discount rate of 7.8%.

- Given the current share price of $9.66, the analyst price target of $11.38 is 15.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.